The Fuse

Futures are strong today with a good bid leading into the opening print. The last five days have been a disaster for the bulls, in fact the Dow Industrials have been lower each day. That may change today. The February CPI number comes out today and will be a determinant of interest rate policy going forward.

We had talked about the 3900 level as being important, sure enough it fell hard yesterday, and actually the low was right near the starting point of 2023. The SPX 500 tagged a low of 3808 yesterday, the Industrials remain below the December lows and the Russell 2k is now negative on the year.

Banks are rebounding today with some upgrades and deep oversold conditions. Asian stocks were down at the open last night, but interest rates continue to be watched carefully. Bank ETF’s are at multi year lows. Some companies are trying to figure out buying pieces of SVB for fire sale prices. New lows crushed new highs yesterday.

Thin pickings on earnings this week, but Lennar reports tonight and a host of smaller names tomorrow.

The big inflation number out is the CPI data today. After completely walking back an aggressive Fed schedule, futures markets are seeing a March rate hike as the last in this cycle. I’m not sure that is the case, we’ll know more with this inflation data.

Breadth was once again weak, save for the nasdaq which was better than the rest. Still, the McClellan oscillator is deeply oversold and due for a bounce.

Heavy volume today as the bigger indices like the R2K and the SPY really took it on the chin. These indices broke to levels not seen since early January. The Dow Industrials is well below the December lows, often a bad sign for the year.

Right back down to 3806 yesterday in what might have been a washout low. That brought the SPX 500 back the flat line for 2023, but a sharp bounce off the lows had the index put in a nice doji. That is indecision. The VIX shows more big ranges coming, but when the news is released this week, it’s possible to see that recede, as has been the case since November.

The Internals

What’s it mean?

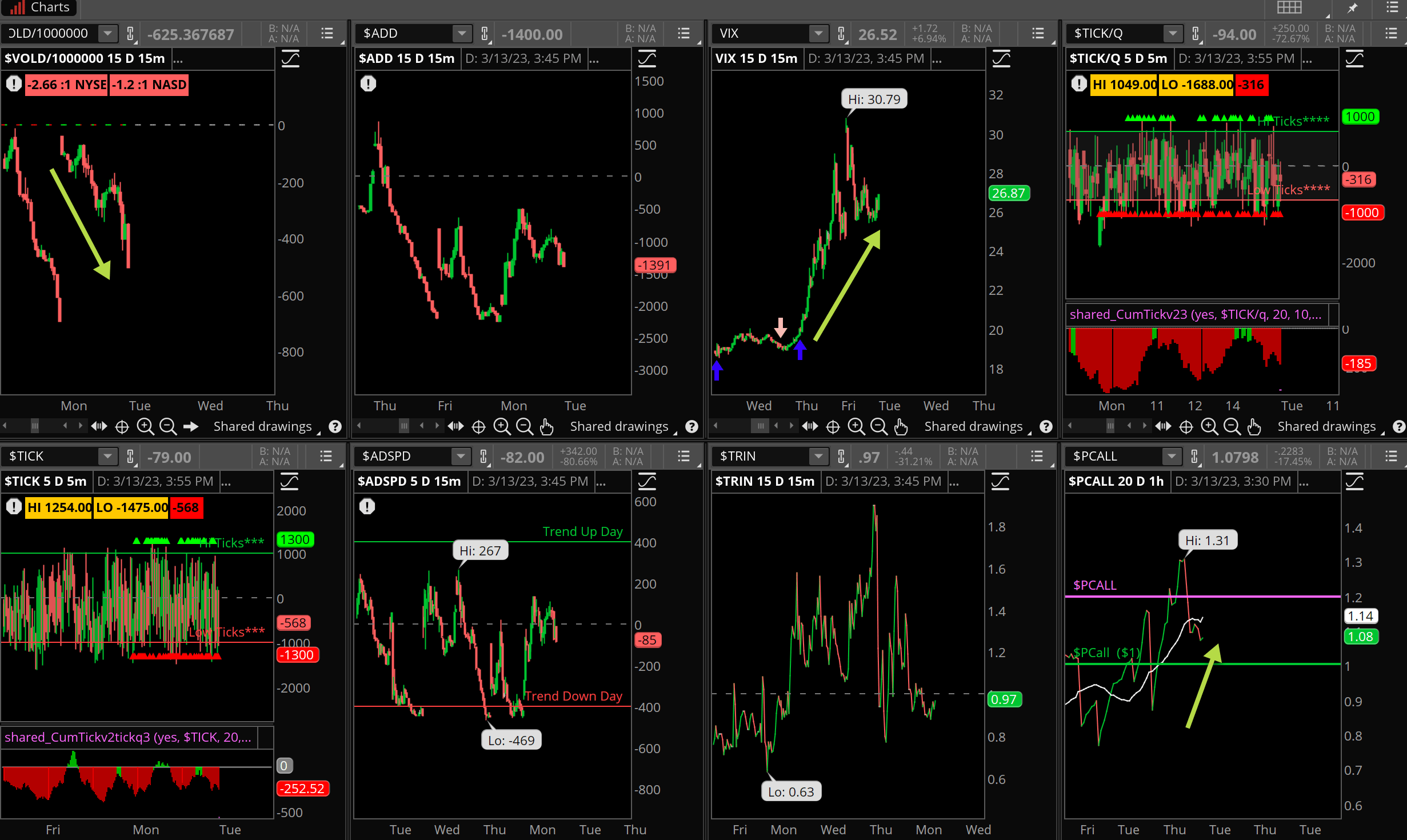

Another day of weakness for the markets, the VOLD was straight down all day long (top left), the VIX shot higher, towards 31% but backed off late in the day. That spike is notable. The ADSPD did not show a trend, put/call backed off some, we may be ready for a whopper rally in a few days.

The Dynamite

Economic Data:

- Tuesday:CPI

- Wednesday:empire state manufacturing, PPI, retail sales, biz inventories

- Thursday:jobless claims, philly fed index, housing starts/permits

- Friday:IP/cap utilization,, LEI, sentiment, Eurozone CPI, labor cost index

Earnings this week:

- Tuesday:LEN GES IHS

- Wednesday:OTLY ADBE FIVE

- Thursday:DG SIG FDX GME GRPN DBI WSM

- Friday:BLDP

Fed Watch: No Fed speakers this week as the committee is in the blackout period before their next meeting. However, the data is going to skew the fed funds futures, so we’ll be watching the movements this week.

Stocks/Issues to Watch

Name – Bank ETF, which is falling sharply with all the bank issues.

Name – Rates, which fell sharply on Monday.

Name – VIX, continues to move upward.