The Fuse

Equity futures are down modestly as we begin the last trading week of April. After a very strong month of March the indices have slowed their pace, so far the S&P 500 is only up .5% for the month but with so much being released this week that could change quickly.

Interest Rates are down on the long end of the curve today as the TLT is rising. The market is still seeing a rate hike coming next week, but the bond market is trying to tell the markets economic trouble lies ahead.

Overnight, Bed Bath and Beyond filed for bankruptcy protection. Morgan Stanley sees risks to stocks due to poor earnings and the Fed, while hedge funds have the biggest bet every against treasuries, believing rates will rise substantially.

Coke is shooting higher this morning after reporting strong earnings and guidance, along with some pricing power.

A quiet week but we have the last trading week of April, which so far is rather flat. We’ll see how much a big earnings week will affect market sentiment, which is rather bullish.

Poor breadth again Friday but well off the worst levels of the day. This turned the oscillator down, but not definitively. We could se a modest pop early in the week to burn of the short term oversold condition, but intermediate term the breadth signals are still bullish.

Volume trends picked up on Friday’s option expiration, so Monday will be the first day of May expiration period. As we head into the start of the worst six months of the year, we often see volume trends slow down, which makes trading the markets a bit more difficult.

A weekly close above 4100 one more time for the SPX 500, that was a huge accomplishment. However, we still see the index trading in a range from 3800 to 4200. The Nasdaq 100 is clinging to 13K, and with so many earnings releases this week it’ll be a challenge to hold those levels into May.

The Internals

What’s it mean?

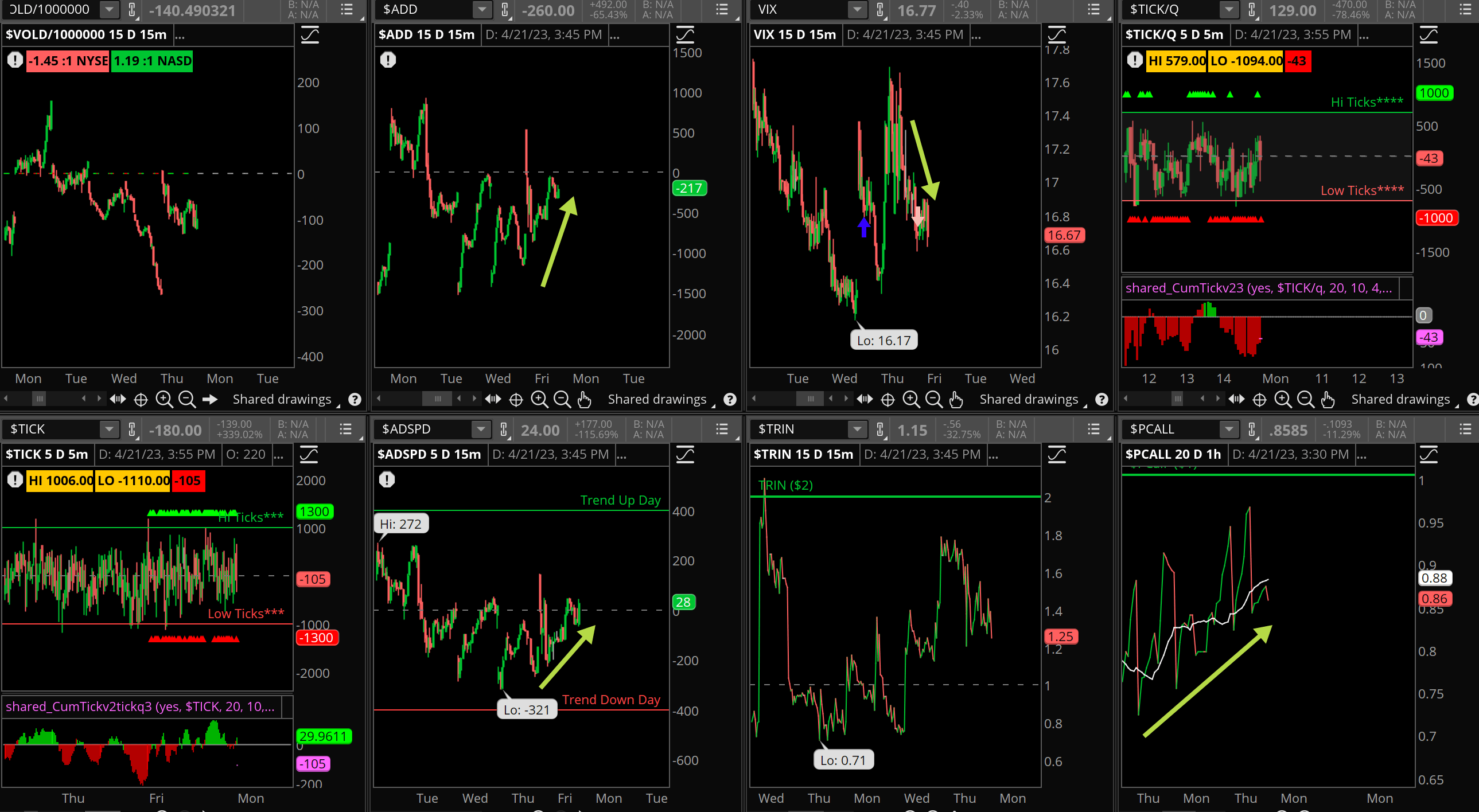

Not much to get excited about with the internals. In fact, aside from Thursday’s market demolition this was simply a repeat of earlier sessions this week. VIX down, Put/calls headed lower and the ADD back to the neutral line. Bargain hunters came in to lift markets higher throughout the day, but the internals do not give us much information about direction just yet.

The Dynamite

Economic Data:

- Monday: Dallas Fed Survey

- Tuesday: Housing Data, Consumer Confidence for April

- Wednesday: Durable Goods, Mortgage Apps

- Thursday:GDP 1st Look, Q1, jobless claims, home sales

- Friday: PMI, Employment Cost Indext, PCE, Michigan consumer sentiment

Earnings this week:

- Monday: KO, CLF, WHR, CDN, AMP, CR

- Tuesday: VZ, UPS, MCD, GM, MMM, PEP, SPOT, RTX, HAL, MSFT, V, GOOGL, CMG, TXN, JNPR, ENPH

- Wednesday: BA, HUM, HLT, TECK, ADP, TMO, GD, BSX, ROKU, META, NOW, ALGN, URI, KLAC, TDOC, WM

- Thursday: AAL, LLY, VLO, MA, CROX, MO, ABBV, MRK, AMZN, INTC, SNAP, NET, FSOR, PINS GILD, AMGN, CAT, DPZ, SAM, X, HSY, MBLY, COF, DLR

- Friday: XOM, , CVX, CHTR, CL, LAZ

Fed Watch: After a bunch of Fed speakers last week we head into the quiet period before the May 2/3 committee meeting. Fed funds futures are showing an 85% chance of a 25bps rate hike at the meeting.

Issues/Stocks to Watch this Week

Earnings – A huge amount of names report this week, more than 1000. Will they beat and raise guidance for the year?

GDP Q1 – First look at the US earnings, Atlanta Fed GDPNow has an estimate of 2.5%. We’ll be watching the inflation portion closely.

Housing Data – With a sharp drop in interest rates, there is a slew of data out this week that will give us good information on the health of this sector.