The Fuse

Equity futures have a solid bid this morning after a very volatile last day of August. As we start the new month, we have plenty of data to consider surrounding the jobs report for August, which is ironic that it comes out before the Labor Day holiday.

Interest Rates are modestly higher this morning but remain steady. It seems the market is just waiting for some news to start buying treasuries again and take rates down below 4%.

August was a down month but not bad enough to keep markets in a bear. After yesterday, we officially grade the stock market in a bull market condition, as the MACD confirmed the July crossover. Time to use the bull playbook.

Blowout earnings from Dell, MongoDB and Lululemon have these stocks pushing higher this morning. The jobs report will move volatility around of course, but solid earnings cannot hold back the buyers.

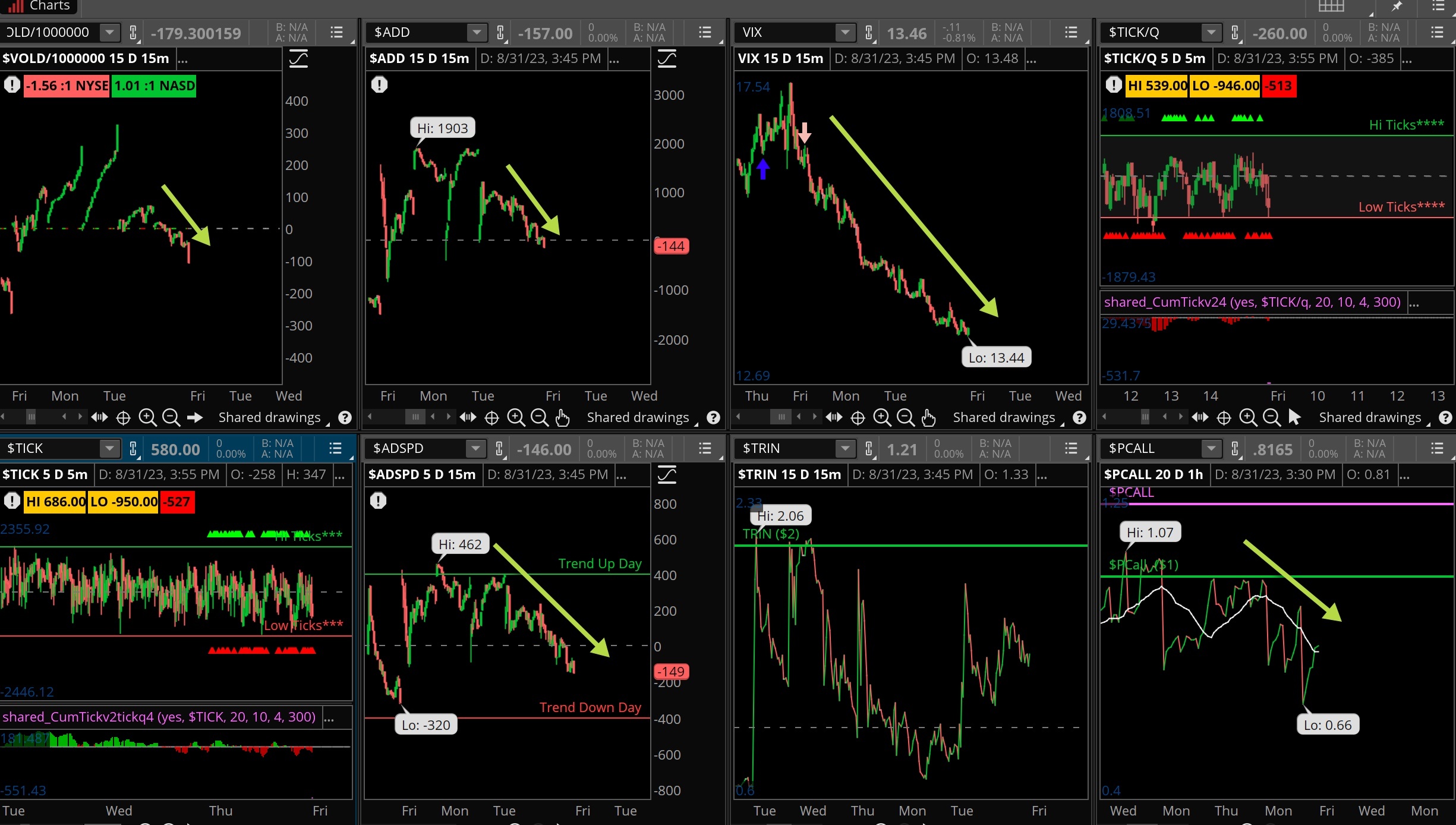

Breadth started strong and then stalled out significantly finishing negative. No worries here though, this indicator remains on a buy signal after having rolled over early in the week.

Not much on the events front other than the non-farm payroll report. Expectations are for 170K new jobs created in August, 3.5% unemployment rate and average hourly earnings up slightly. We’ll have ISM and construction spending a bit after this report. Cleveland Fed’s Mester speaks later today.

Good not great volume on the last trading day in August. Overall it was a muted month of turnover, not surprising as many disinterested players were not even around to trade stocks. That may pick up after the holiday however. September is often a rough month for markets.

4,600 on the SPX 500 remains the next target level, but at that point the market might be overbought. It certainly depends on how much time is spent above the current 4500 level. Nasdaq was looking as if it would roll over last week but the buyers stepped in a supported at 15K, next stop 16,200.

What’s it mean?

Consolidation day for the indices and the internals. Notice on the VOLD there was spillover buying at the start but breadth and volume retreated, that’s normal following a few strong days in a row. Volatility (VIX) remains under pressure though and put/calls are finally coming down. Ticks were moderate but that will change later today.

The Dynamite

Economic Data:

- Friday: August job report, ISM manufacturing, S&P Global PMI for August

Earnings this week:

- Friday:

Fed Watch:

Well, if anyone was expecting something different from Chair Powell following last month’s Fed hike they were disappointed. The Chairman was quite hawkish again and said under no uncertain terms the committee is ready to hike rates further. The Cleveland Fed Nowcasting sees August CPI rising by 9.6% annualized on the headline number, but core about unchanged (higher than preferred). If that number comes in hot we’ll see talk of 6% rates coming very soon (fed funds). As of now, any rate cuts probabilities are dwindling.

Stocks/issues to Watch This Week

Salesforce – This company reports earnings this week and many are concerned about the valuation, which has become quite rich in a tough market.

VIX – We’ll be watching volatility again as we approach the month end, which could ignite some fireworks. A three day weekend is upon us though and that could lead to a drop in volatility.

SPX 500 – Thursday is the day, the last trading session in August. If the MACD manages to hold the crossover from July then we can designate a bull market has been established. It’s been awhile! Doesn’t mean the market goes up every single day, however.