The Fuse

Equity futures are up a bit this morning after a non-eventful weekend. Dow futures are up strong though component Pfizer is down early.

Interest Rates are rising again this mornings as fixed income investors continue to shed bond holdings. It’s been a methodical drop in bond prices, yields are right near 5% on the long end of the curve. If that level is breached there could be another leg down for the stock market.

Not much news over the weekend and that was a relief. Still, there is a worry out there of something bigger or more ominous coming from the Middle East, but perhaps that is just a natural worry. Gold prices are down slightly while crude is up nearly 1%.

A huge week of earnings this week as we’ll hear from Tesla, Netflix ASML, American Express and others. We normally see a good market response to the first big week of earnings season, but the uptrend is starting to shift downward. If money flows are weak then we could see stocks move lower if guidance is disappointing.

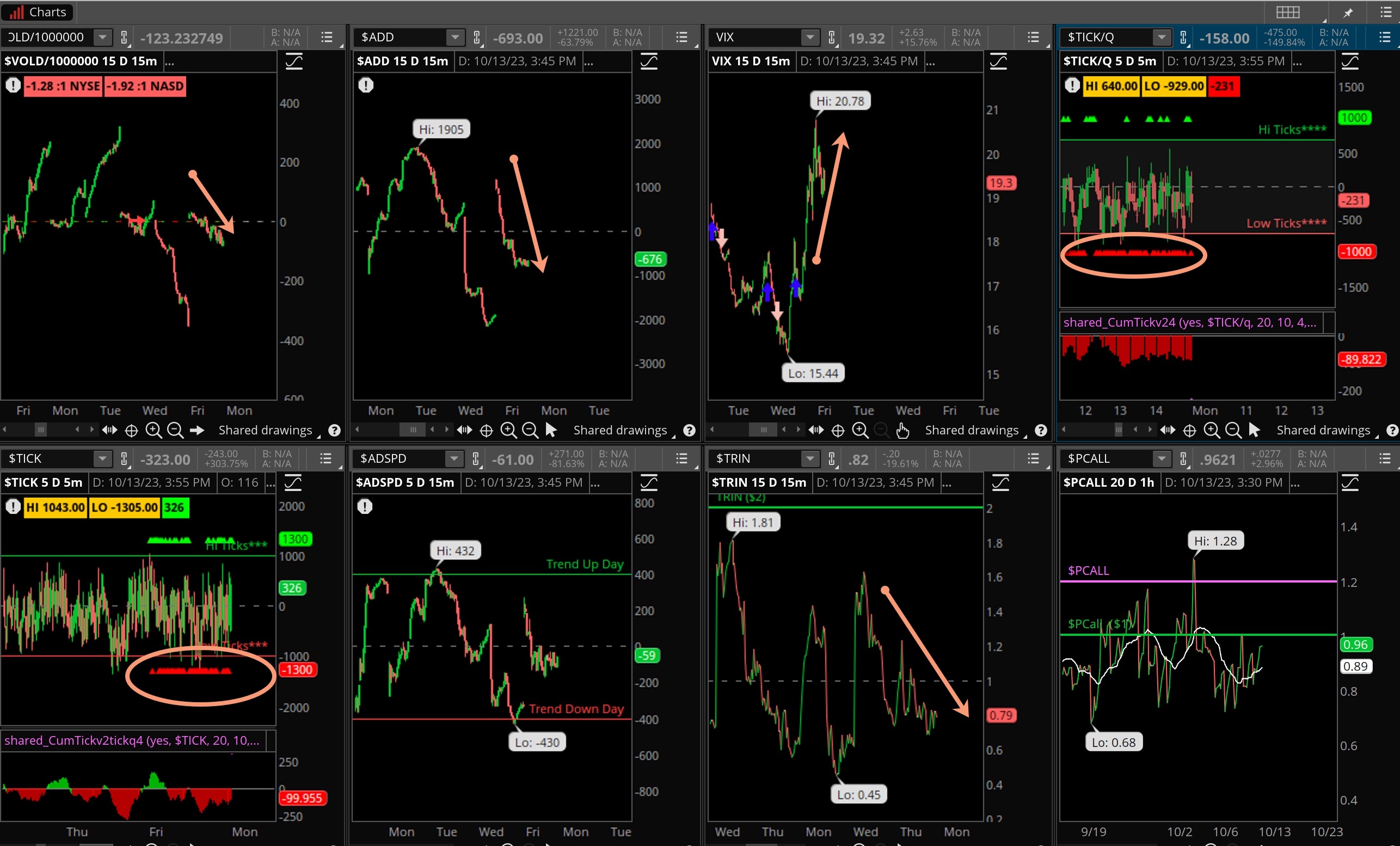

It’s a big options expiration week coming up on Friday, and all signs point to a volatile week of action. Market volatility is on the rise and has been for a few sessions. The VIX has been making a move towards 21% and could threaten to break higher this week.

Breadth was poor Friday and coupled with Thursday’s weakness this indicator is on a sell signal now. With a couple of positive sessions that can change but breadth can be weak for awhile. New lows expanded on the NYSE and Nasdaq Friday and remain buried in a bearish trend.

Volume trends were strong and bearish Friday, another day of distribution notched as markets remain under some severe pressure. The reversal on Thursday and the continuation of that move on bigger turnover Friday was not a good sign for the bulls.

The SPX 500 closed right on the 20 day moving average Friday, amazing how that works, huh? That average is important of course as a reference point. The 20 ma is still moving downward, and some closes below early in the week will set up a test of the prior week’s lows around 4200-4220 on the SPX 500.

The Internals

What’s it mean?

Weak internals all day long but not horrendous, yet the VIX rocketed higher and closed at an eight month high. Put/calls are on the rise again while ticks on both indices were deeply red. With gold up, volatility up and bonds up that meant a risk off day all around, and that’s what we got.

The Dynamite

Economic Data:

- Monday:Empire Manufacturing Index

- Tuesday:Retail Sales, Industrial Production/Capacity, biz Inventories, housing market index

- Wednesday:Housing starts, crude inventories, Fed beige book

- Thursday:Jobless claims, Philly Fed index, Home Sales, Leading Indicators

- Friday:Japan Inflation, German PPI, UK retail sales

Earnings this week:

- Monday: SCHW

- Tuesday: ACI, BACK, BK, GS, JNJ, LMT, IBKR, JBHT, UAL

- Wednesday: ELV, MS, PG, AA, CCI, LRCX, NFLX, PPG, SAP, STLD, TSLA

- Thursday: AAL, T, MAN, NOC, UNP, CSX

- Friday: AXP, SXT, VFC

Fed Watch:

More Fed speak this coming week, but we heard plenty the last two weeks and from the meeting minutes released on Oct 11th. It seems the latest data and information is slowly turning the Fed less hawkish, but only slightly. Yet, there are several on the committee who are willing to wait it out even longer. Let’s see how the market responds to the higher inflation readings from last week.

Stocks to Watch

Netflix – Always interesting to watch how this stock moves following earnings.

Tesla – This EV company reports earnings this week and while car sales have been brisk, the concern is over margins as Tesla continues to cut prices sharply.

Interest Rates – They rose sharply this week then collapsed again Friday, we’ll see if they make a run at new highs or fall down as the safety trade is back (Middle East turmoil). We’ll be watching gold as well, which put in a spectacular week.