The Fuse

Equity futures are soft this morning after a very strong rally ensued just before the close on Monday to put the SPX 500 index on the precipice of 5K. Big earnings are out after the close tonight and may offer some direction. Only two days left in the month of January at it appears this might be another up month, but plenty of time to let things play out. The VIX is starting to rise up slightly and that may control the action. Risk off day to start.

Interest Rates are sliding today as the market grapples with new interest rate policy announced on Wednesday. In a risk off mode we often see bonds catching a bid. The 10 year is trying to make a run down towards 4% but it would take a sharp move lower in yield to get there. It’s possible however if stock investors are more risk averse in the coming days.

Today starts a two day meeting for the Federal Reserve as they weigh in on current monetary policy. The market is looking towards rate cuts later in the year and perhaps as early as March. If that is not the case the markets are likely to be disappointed but will soon realize the Fed’s goals are real and not fantasy. The IMF boosted global economic growth for 2024 and sees inflation retreating. The IMF sees a soft landing for the US economy but growth slowing to 2.1% from a hot 2.5% in 2023.

Earnings are starting to come in hot n’ heavy and tonight we’ll hear from some big names like MSFT, AMD, SBUX and GOOGL. This morning strong numbers from GM and Pfizer along with HCA, very poor guidance from UPS as they missed on their earnings quarter as well.

Futures sold off soon after opening up Sunday evening and that spread to some losses overseas, but the buyers came back in a hurry and waited patiently for the selling to dry up. When that happened, the bulls stepped in and whacked the bears upside the head, pushing the indices to new highs (save for the Russell 2K). It’s been an impressive charge especially in January after getting off to such a difficult start. Nobody seems to remember the Santa Claus Rally failure any longer.

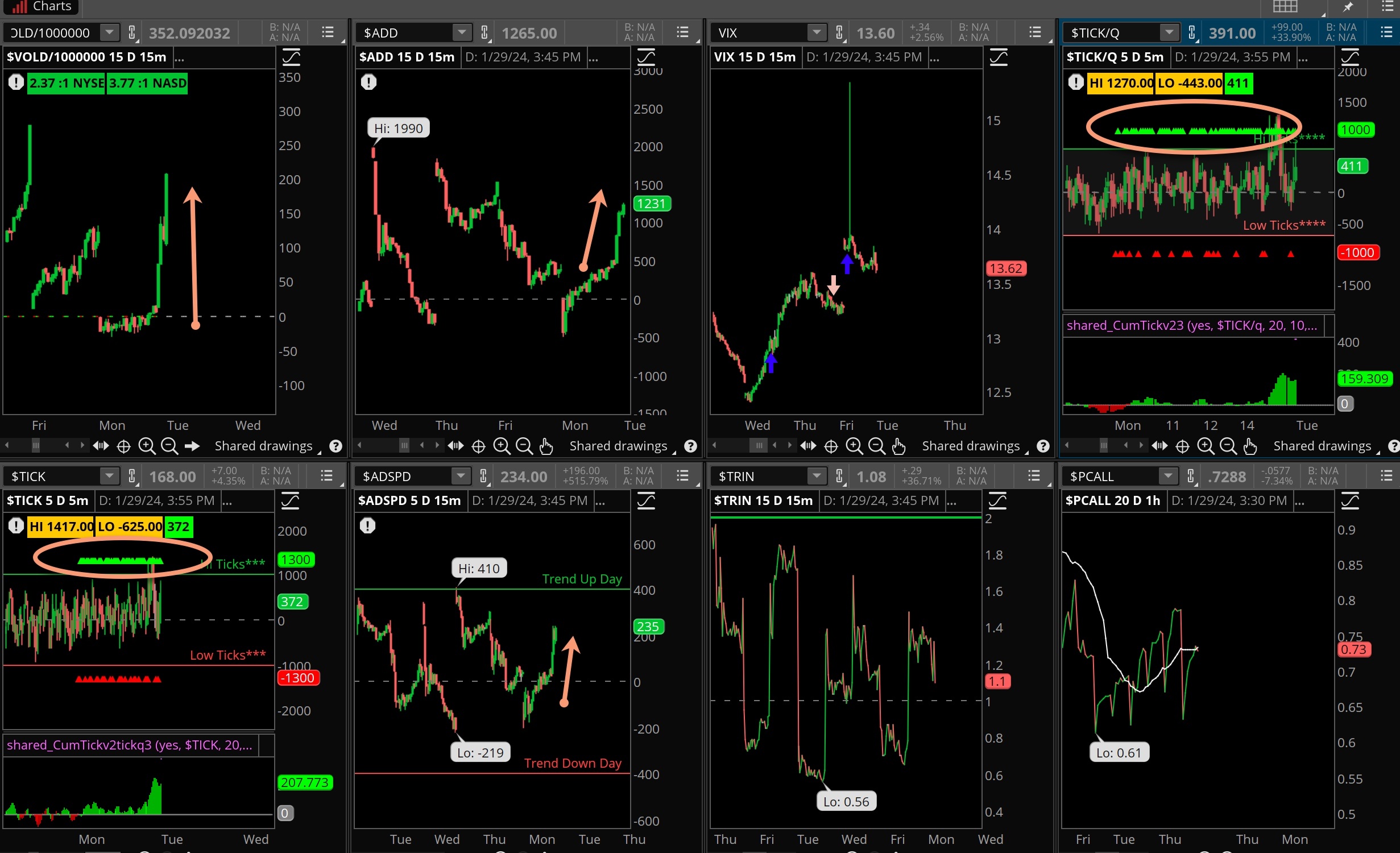

Markets were slow a’foot most of the day until some big buy programs hit in the last hour to vault markets higher. Breadth was mediocre most of the day but managed to finish with a grand flourish, nearly 3-1 positive. Much of that gain came late in the day, see the internals below. Breadth is still on a buy signal, new highs trouncing new lows.

Turnover was modestly lower all the indices save for the Nasdaq but that is often the case following a weekend. We should see more volume as we make it through the week. If yesterday’s price action is any indication there is more volume left to the upside, markets are not overbought at all.

More new highs and this time 4,900 was penetrated, the buyers went through that level like a hot knife through butter. 5K is next up on the SPX 500 and could be seen later in the week. The price action, the trend, momentum are all in the bulls’ favor at this point. Seasonal trends are also bullish this week.

The Internals

What’s it mean?

An explosive rally hit the markets towards the end of the and we can see how powerful that move was in the internals. The VOLD burst out and moved up sharply as did the ADD, while the TICKS were solid green all session long. It was an impressive close and there is perhaps more upside to come later in the week. Put/calls came back down and the VIX remains contained.

The Dynamite

Economic Data:

- Tuesday:Housing price data, JOLTS, consumer confidence, fed meeting starts

- Wednesday:Fed rate decision, ADP report, crude inventories

- Thursday: Jobless claims, productivity/labor costs, ISM, construction spending

- Friday: Employment report, factory order, Michigan consumer sentiment

Earnings this week:

- Tuesday: GLW, DHR, GM, JBLUE, PFE, UPS, AMD, GOOGL, EA, MSFT, MDLZ, SWKS, SBUX

- Wednesday: BA, EAT, MA, ROK, KLIC, QRVO, QCOM, WCN

- Thursday: ETN, RACE, HON, LAZ, MRK, SWK, AMZN, AAPL, META, BZH, HOLX

- Friday: ABBV, CVX, XON, CHD, QSR

Fed Watch:

Another huge week for markets as the Fed will sit down for their first meeting of 2024. Fed futures are predicting no change in the current rate policy but perhaps in the statement some wording that might hint of rate cuts. The projections last month pretty much did that, but there is a wide disparity between what the Fed’s reality is versus the market. Perhaps some of that differential will be narrowed this week. The futures market still sees 5-6 rate cuts this year.

Stocks to Watch

Earnings – Thursday is a big day but so is Tuesday, which has AMD, MSFT, GOOGL, SBUX to set the table. Thursday has Apple, Amazon, Meta, Atlassian and others. These earnings reports will definitely drive market volatility.

Interest Rates – With a policy meeting this week we may see big moves in the 2 year yield. Note, the spread between 2’s and 10’s has narrowed significantly as the market prepares for a pivot in monetary policy (soon).

Economic Data – with all that is happening it is also a big week for data (see above). We’ll have the January employment report, ISM data, productivity/labor along with confidence and sentiment data.

[thrive_leads id=’60674′]