The Fuse

Finally election day is here and after today the stock market can forget about a Presidential election for four more years. Futures are rallying a bit following Monday’s volatile trading session. If there is no chaos following the election look for volatility to shed some of this premium over the coming days. The VIX is overwhelmingly elevated here.

Interest Rates are slightly higher today as bond sellers continue to shed their holdings in front of the next Fed meeting, which starts tomorrow morning. The 2 yr yield may have hit a ceiling at 4.25%, it has suddenly backed off. Fed funds futures are seeing a 100% chance of a cut this week, even a small chance of a double cut while December continues to be priced in for a cut. The committee may have other ideas.

US futures up modestly as the Stoxx in Europe pulled back .2% after a strong Monday. The dollar fell slightly, crude oil continues its steady climb while gold settles in just under all-time highs. The German 10 yr bund yield was up 3 bps, the 10 yr US treasury rose the same amount. In Asia, stocks in Japan were higher by 1.1% after a day off, Hong Kong and Shanhai up more than 2% each on robust turnover.

Earnings last night from Palantir were fantastic, they beat and raised guidance, the stock up more than 10%. Wynn missed and guided lower, NXPI also with a guide down. today we’ll hear from controversial SMCI, then Devon, Exact Sciences, and Microchip.

Perhaps the election today will be on the minds of investors/traders, but maybe not. Certainly market volatility is elevated just in case some chaos leads to selling. Remember, high volatility such as now for a specific event is often sold down (never a guarantee). Given the likelihood no winner will be declared for days it stands to reason more uncertainty will be seen down the road.

Breadth was good on Monday, but much better earlier in the session. Yields were down all day across the curve and that brought out the small cap stock buyers. The IWM was up nicely but the other indices were down sharply, especially the Industrials which are now in correction territory. Relative strength is quite poor.

The oscillators are still moderately oversold but could get even more oversold, new lows are starting to bounce vs new highs, something to watch.

Volume trends have turned bearish. While yesterday’s turnover was less than Friday there has been giant shift in patterns. We no longer see strong volume days on the up sessions. That tells us accumulation days are not happening, while have had a series of distribution days plague the markets. That could be trouble brewing if seller continue to hit the markets.

The SPX 500 nailed the 50 day moving average again and bounced nicely to the highs of the session but that bounced was sold vigorously. There is some good support though at the 5,700 level and below there at 5,670, but if that fails to hold there is significant downside. The uptrend remains in tact for now. The industrials are the worst index at this point, 40K is next up (another 5% lower).

The Internals

What’s it mean?

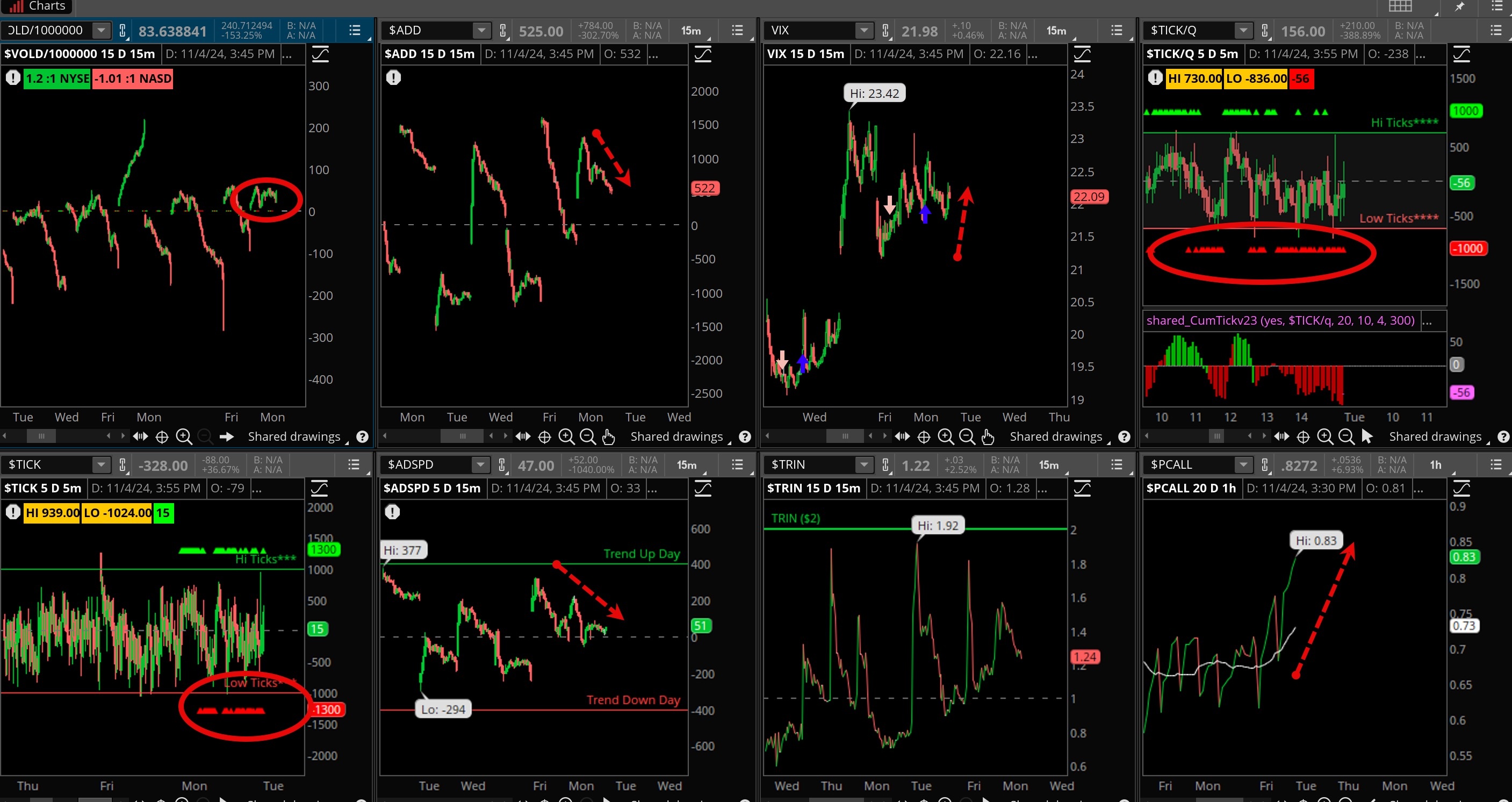

Another poor showing for the internals, it still seems the market is trying to get past the election and the Fed this week. The VOLD is symptomatic here, there was little movement even as breadth was positive. ADD fell from the start, and check out put/call ratio (bottom right), soaring as put buying was heavy in front of the election. Ticks were moderate but leaning towards bearish (more sell programs).

The Dynamite

Economic Data:

- Tuesday:ISM Services, trade deficit

- Wednesday:SPX final US services PMI

- Thursday:Jobless claims, productivity, FOMC rate decision, consumer credit, inventories

- Friday:Consumer sentiment

Earnings this week:

- Tuesday:MLCO, ADM, APO, RACE, BLDR, DVN, SMCI, MCHP, EXAS

- Wednesday:CELH, CVX, TEVA, TM, JCI, ARM, AMC, QCOM, ELF, APP, IONQ, CLOV

- Thursday:VSTR, GOLD, DDOG, HAL, HSY, MRNA, DKNG, ANET, SQ, RIVN, U, TTD, AFRM, FNET, PINS, ABNB

- Friday:SONY, IEP, FLR, NRG

Fed Watch:

Another Fed meeting is upon us and the Fed futures market predicts a cut after Thursday’s meeting. That is likely the case as the committee has no reason to disappoint the crowd, but debate about a December cut will certainly be heard. The job report Friday (poor) may be an anomaly, but if it is slowing that quickly a faster rate cut policy may be appropriate.

Stocks to Watch

Election – We have finally come to the day that can change the US. We should know how things turn out later in the week, the effects on the market and economy will be analyzed.

Federal Reserve – The seventh meeting of 2024 will take place this week, the committee is largely expected to cut rates once more, this time by .25%. That may not sound like much but with lower inflation it makes sense for the committee to bring down borrowing costs.

Earnings – It is another big week of earnings as the season comes into the halfway point. 1/3 of the SPX 500 reported last week and very little damage was felt. Many stocks reporting this week have strong chart patterns and formations, we’ll see if that continues to be the case.

[thrive_leads id=’60674′]