The Fuse

Equity futures are a bit soft and carrying through from yesterday’s modest drop. Today we’ll have the November employment report which will be watched carefully for any signs of a slowdown or increased inflation.

Interest Rates are down a fraction as long term bond holders begin to look for bargains. Naturally, the jobs report today is going to have an impact on the bond market if there is some inflation, where yields could move sharply higher. Fed funds futures still see a better than 72% chance of a cut next week.

Stocks are mostly flat around the world, the STOXX in Europe was unchanged, the dollar rose up slightly while gold is rallying. Crude is off about 1% in early trade, German bund yields were flat while US treasury 10 yr yields are up 2bps. Stocks in Asia were mixed, Japan down but China and Hong Kong ripped higher.

Very strong earnings from Veeva, Asana, Docusign, Gitlab and LuluLemon last night has these names vaulting higher in pre-market trading. We move next week into phase 5 of earnings season, a few big names into the end of the year but very few until about six more weeks. Only 17 more days of trading in 2024.

Good action yesterday but really not packing any punch as stocks continue to drift. It seemed we might have a good move higher but some selling hit later in the morning as stocks could not recover. Perhaps that is due to the low volatility we are experiencing.

Breadth once again was poor and reflected the drop in small cap stocks, which fell below some support yesterday. We have experienced mediocre growth in breadth over the last week or so, oscillators have just turned negative as well. New highs continue to push up and crush new lows, that longer term indicator still in tact.

Volume trends are weak and are not expected to push higher in the coming weeks. However, we may see a bit of a surge after Christmas due to some rebalancing efforts by hedge funds, mutual funds and pensions. Stocks are having a great year once again and if you’re sitting there waiting for a pullback that never happens you just might find yourself in a quandary.

A bit of a pullback to let the moving averages catch up is a good thing, though it may not feel good at the time. Certainly with the strength in the indices this year it is difficult to pinpoint proper entry points, but for the patient trader/investor waiting fort that move back to the 20 day moving average has proved to be golden.

The Internals

What’s it mean?

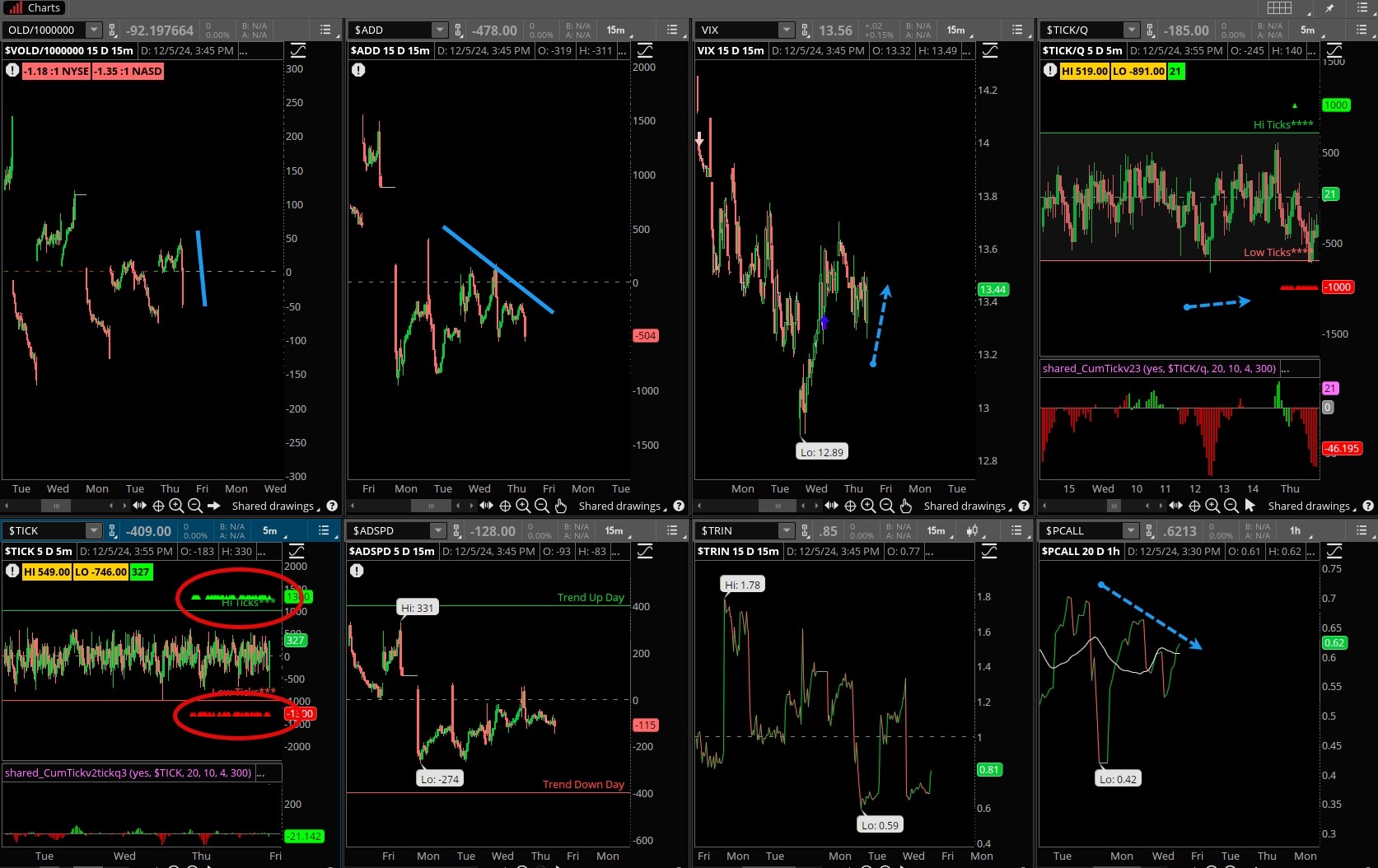

Mediocre day on the internals, the VOLD slipped down end of day as did the ADD, lots of sell programs as well. The ticks were dominated by red, the Nasdaq especially with only a handful of green ticks. VIX is down pretty low here and is due for a bounce, but any push higher is likely to be sold (which is bullish for markets).

Put/calls remain low here.

The Dynamite

Economic Data:

- Friday:NFP report, consumer sentiment, consumer credit, Fedspeak

Earnings this week:

- Friday:GCO

Fed Watch:

Not much fanfare as only a couple of fed speakers this week, Goolsbee and Musalem. Most of the chatter recently has been worry about sticky inflation, the data has been telling us this as well. The next Fed meeting is Dec 10, the last of the year, the market is looking for a cut but may be disappointed.

Stocks to Watch

Sentiment – No question momentum is on the side of the bulls. This is the first week of trading in the most bullish month of the year, and coming off a spectacular November the best bet is on a continuation rally. This week is important to see if that momentum continues or if the market is looking to take a rest.

Retail Stocks – Coming of a very strong first holiday weekend, we may see a pop in some retail names as these companies ready for a big finish towards Christmas. Pay attention to deals and discounting.

Energy – Oil has been going sideways a bit but with a OPEC meeting coming up soon that may change, if the cartel decides to slice production.