The Fuse

Equity futures are shooting higher this morning after it appears some positive news on tariffs (putting them off) has influenced buyers. This is the last full week of trading in March and the bulls are way behind, 4-6% in all the indices so that is some ground to make up. Quite a bit of rebalancing will occur this week with pension and hedge funds, plenty to buy as we approach the following Monday.

Interest Rates are moving slightly higher as bond traders take some equity risk. Fed futures are still suggesting 3 cuts in 2025 but the FOMC is pretty far away from there. Yet, with a couple more inflation friendly readings (PCE later this week) that might move sentiment in that direction.

Futures are ripping higher following a positive session in Europe. STOXX were up .5%, France and Germany rose up better than that during their session. The dollar fell.1%, German 10 yr bund yields up 1bp while US 10 yr treasury yields declined 3bps, a nice bid under long bonds. Gold is surging, up 11 bucks as crude also shows a nice bid, higher by .8%. Stocks in Asia were mixed, Nikkei down .2% but Hong Kong rising .9% and Shanghai up a small fraction.

Last week of earnings for stocks in Q4 period, not much on the docket but we’ll hear from McCormick, Chewy, Paychex, LuluLemon, Dollar Tree, Canadian Solar, and GameStop.

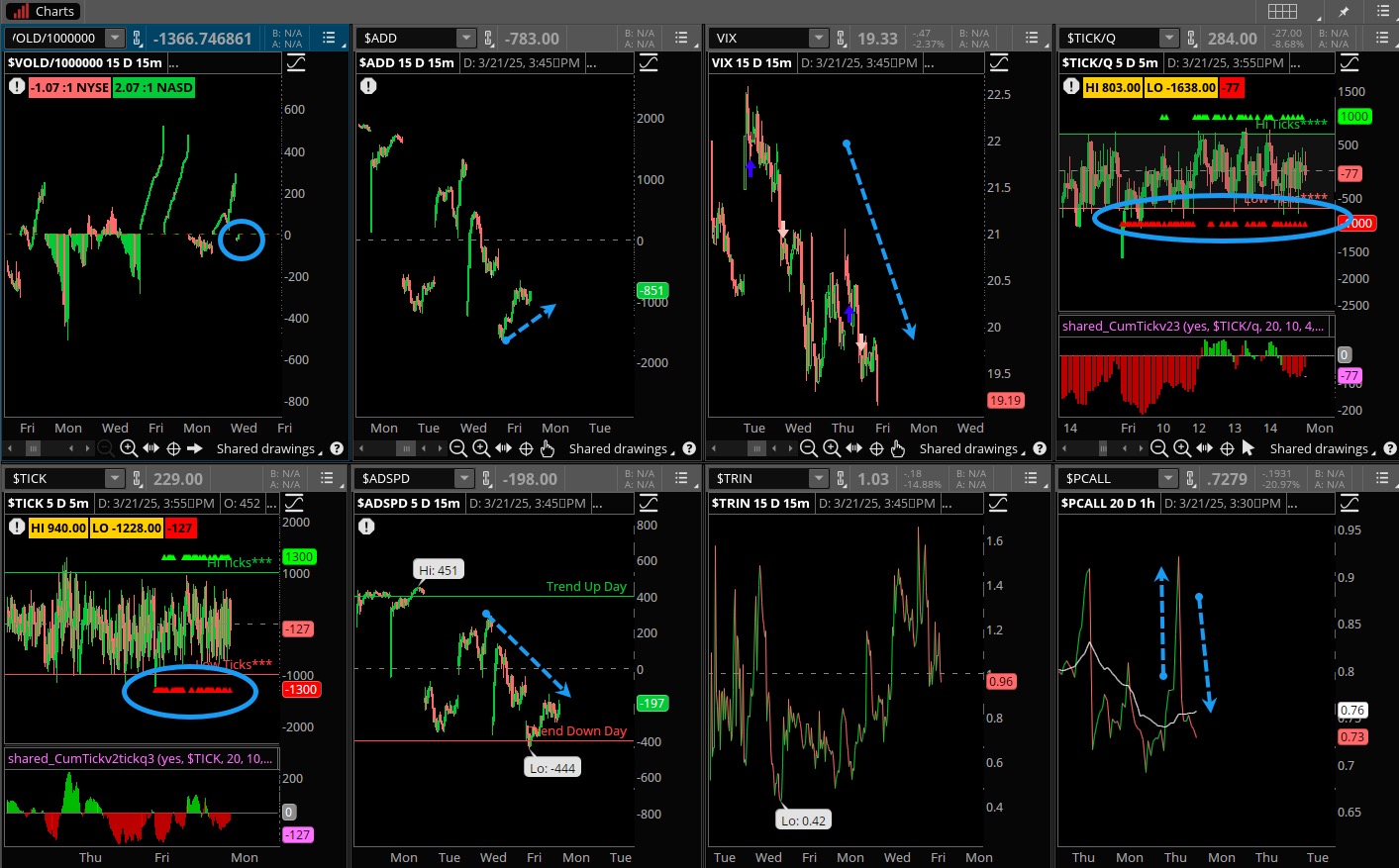

After following Europe down overnight the bulls clawed back on this expiration Friday and got the markets back into the green, sorta (only the Nasdaq was green). The indicators really did not support the rally, which likely came about due to some imbalances from options expiration. We’ll see how the bulls feel about things this week, only six trading days left in March and the indices are sharply lower. April 2nd is coming up fast, which is the big tariff day. Expect volatility to pick up.

Breadth was poor again and that has this indicator on the verge of moving into bearish territory. Oscillators are barely in the green as well, another down session is going to be bad for the bulls. New lows continue to recede, interestingly enough. There have been some good breadth days but this coming week could define where this indicator is going over the next several weeks.

Volume was heavy as we expected. Options expiration was big with 4.5 trillion of notional value expiring by days end. That is a whopper amount, stocks were either called or put to option sellers/buyers so we’ll see how that plays out early today. We may have a bit of a hangover effect from this expiration day but the market players seem to be trying to carve out a bottom.

Remarkably the SPX 500 finished on its highs of the session as did the Nasdaq, which posted a green day. The gap from the open filled nicely, but there is plenty of work to do. The lows on Friday for the SPX 500 are right near 5,600 as that should hold firm if there is confirmation today. Plenty of worry to go around however and not much on the earnings front to whet an appetite. PCE end of week will be big. Support for Nasdaq is strong at 19.4K.

The Internals

What’s it mean?

It ended up being a positive day for the indices but overall the internals look horrific. The breadth was poor, the ADD in the tank so was the VOLD, the ADSPD weak and nearly a trend down day. We saw heavy sell programs persist for most of the day, the VIX did decline sharply into the end of the trading session. Put/calls fell but after being up sharply Thursday. All in all, a poor session that needs some confirmation today, or it is all for naught.

The Dynamite

Economic Data:

- Monday:SPX flash services, flash manufacturing

- Tuesday:philly fed, consumer confidence, new home sales

- Wednesday:Durable goods, St Louis Fed President

- Thursday:Jobless claims, GDP revision, trade balance, retail/wholesale inventories, pending home sales

- Friday:income/spending, PCE, consumer sentiment

Earnings this week:

- Monday:LUCD, OKLO, KBH, DFLY

- Tuesday:CSIQ,RMBL, MKC, PONY, GME, WOR, CRVS

- Wednesday:DLTR, CHWY, JKS, PAYX, CTAS, MVIS, WOOF, VRNT, JEF, HBF

- Thursday:WGO, SACH, IPHA, LULU, BRZE, KULR, OXM, SKYH

- Friday:IPA, SLE, ZSPC, LIQT

Fed Watch:

The Fed came and did their thing last week, deciding to keep rates where they are and not offering too many clues as to their intentions. They did talk about starting to put an end to the QT program, reducing their sales of bonds to prevent a major liquidity crunch. As or inflation, Chair Powell believes tariffs will be a drag on the economy and bring up inflation, at least in the short term. A couple of fed speakers out this week talking up the economy.

Stocks to Watch

Banks – Financials have started to show better relative strength. No doubt they will be the leaders into the new month as earnings season gets underway in April. Top of the charts is JP Morgan but we will also be watching Goldman, Morgan Stanley and Citigroup as those names rally to the 20 day moving average.

Market Volatility – The VIX continues to be the story of late. The fear index has been on the rise lately and remains stubbornly high. However, release of the Fed notes last week pushed volatility sellers to work the VIX downward. Uncertainty over tariffs keeps a bid in the VIX though, we’ll see how much movement in the markets happens./span>

Tariffs – With the April 2 deadline looming towards across the board tariffs on other countries, we still have some uncertainty whether these are going to take hold or not. That is causing some angst but when the deadline passes (assuming it is not extended) we will have more clarity.