The Fuse

Futures are up sharply as they continue a drive up towards their February highs. Overnight we got a reading on China GDP, which came in better than expected.

As the SPX makes a run to 4200, we acknowledge the markets are bit overbought here, but not extreme. That could change though in the next day or two as more earnings come out. So far, about 90% of those reporting have beaten, but the guidance has been a bit less than desired. Interest rates are down once again on the long end of the curve, but we still see an 85% change of a rate hike coming in May, many believe this will be the last hike for some time.

The strong China numbers overnight are the big news, but we’ll be waiting on some Fed speak later in the week.

Strong earnings from BAC this morning has this stock boosted higher, but Goldman Sachs missed on revenues, which is hitting the Dow Industrials a bit. Lockheed Martin also posted robust gains and is pushing at $500 a share.

Nothing too eventful today other than the Boston Marathon here in New England! However, markets are grinding higher and have been for a few weeks now, the wall of worry is up high. With two weeks left in the month and a slew of earnings news, we’ll see if the bar is set low enough.

Solid breadth all day long as the bulls shook off the cobwebs from the weekend and poor breadth to end last week on a sour note. This bodes well for more upside later this week.

Volume trends are starting to turn upward, and Friday’s late surge only improved those prospects.

A solid comeback from the lows of the day put the SPX 500 above 4150, the first time at that level in more than two months. With positive vibes from earnings season it appears the Feb highs are in reach.

The Internals

What’s it mean?

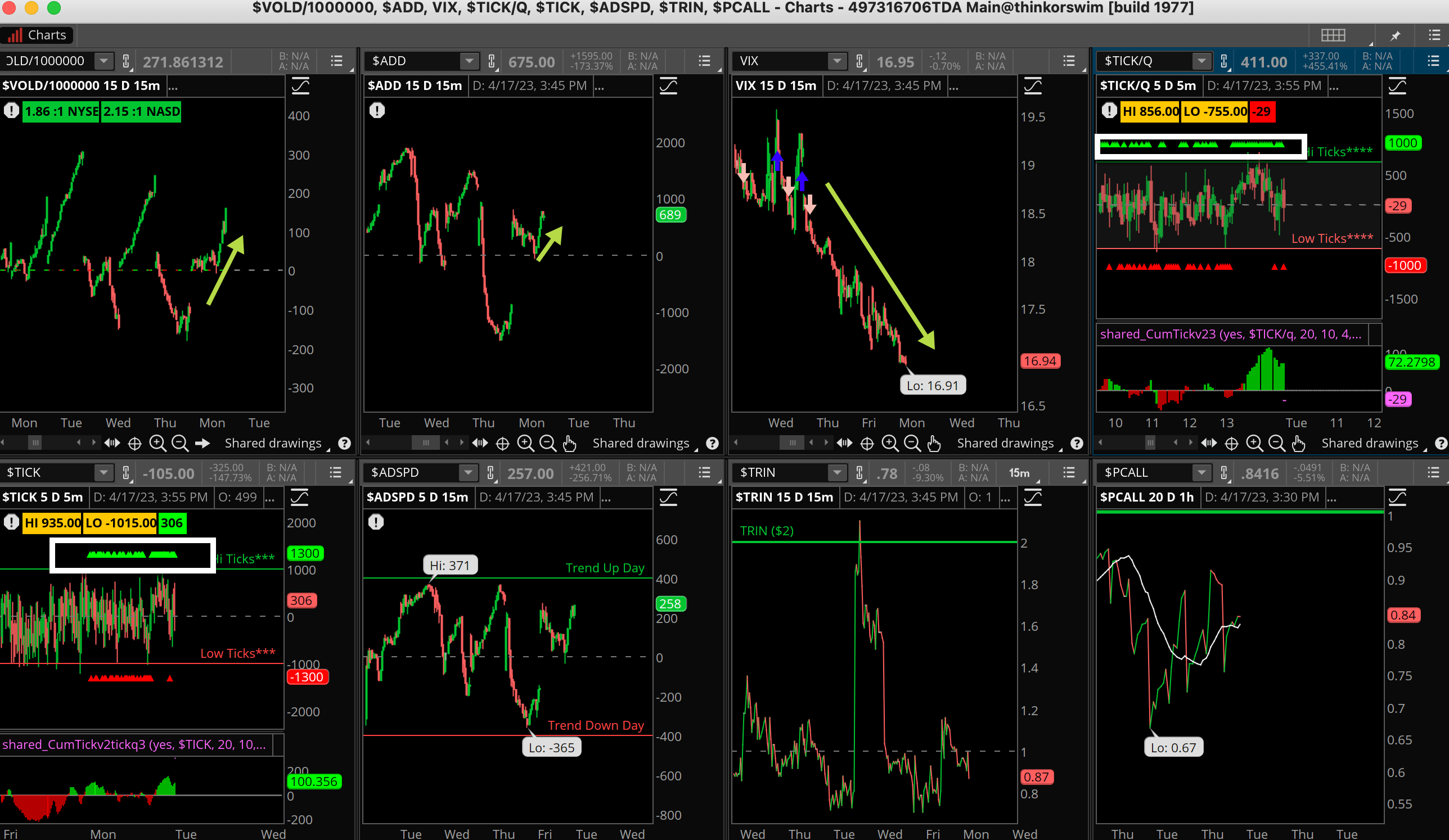

Today was all about the VIX, or the big drop below 17. It’s becoming a game of limbo, ‘how low can you go’. With nary a worry it seems investors/traders are trying their best to push markets higher, and it’s working. Notice the ticks on both exchanges, strong green/yellow ticks all session long, represents strength in buy programs. VOLD was strong as well especially the last couple of hours when markets rallied. This bodes well for more upside this week.

The Dynamite

Economic Data:

- Tuesday: Housing Starts and Building Permits

- Wednesday: Crude inventories, Beige Book

- Thursday: Jobless claims, Philly Fed, Leading indicators, Ex home sales

- Friday: Flash PMI

Earnings this week:

- Tuesday: BAC, BK, ERIC, GS, JNJ, LMT, IBKR, NFLX, UAL

- Wednesday: ASML, ELV, MS, AA, DFS, IBM, LRCX, TSLA

- Thursday: AXP, T, DHI, NOK, NUE RAD, TSM, UNP, CSX, PPG

- Friday: FCX, HCA, PG, SAP

Fed Watch: Fed tool is now seeing about a 75% chance of a rate hike in early May. That’s about as close to a slam dunk as you can get. Fed speakers last week are still hawkish, Friday’s comments from Chris Waller implies the Fed may go even more.

Issues/Stocks to Watch This Week

Tech earnings – The first big week of earnings with several releases, we’ll be keeping a close eye on technology names, which have surged in 2023.

Options – Friday is a big options expiration day, and with so much bullishness recently we could see a bit of those gains given back.

Fed Speakers – Notable on Thursday is hawkish Cleveland Fed President Loretta Mester, who has a significant influence on the committee.

[thrive_leads id=’60674′]