The Fuse

Equity futures are down this morning as yesterday’s monster rally is digested. The SPX 500 is back above 4100 after a 2 day stint below. With PCE out later this morning and a hot number expected (perhaps 5%), we’ll see how the market handles that piece of news. It is the last trading day of April.

Interest rates are declining once again today as the 10 year yield pushes up past 3.5%. Fed funds futures sold off Thursday as expectations for rate hikes continue to build.

Weaker than expected GDP along with higher inflation, yet the market climbs! Is it a wall of worry, or simply big money positioning for the end of the Fed tightening cycle and slower economic growth?

Names like NET, SNAP, AMGN, and PINS posted weaker earnings but INTC raised their guidance after a modest miss.

Amazon reported after the close and posted a robust gain on the top and bottom line.

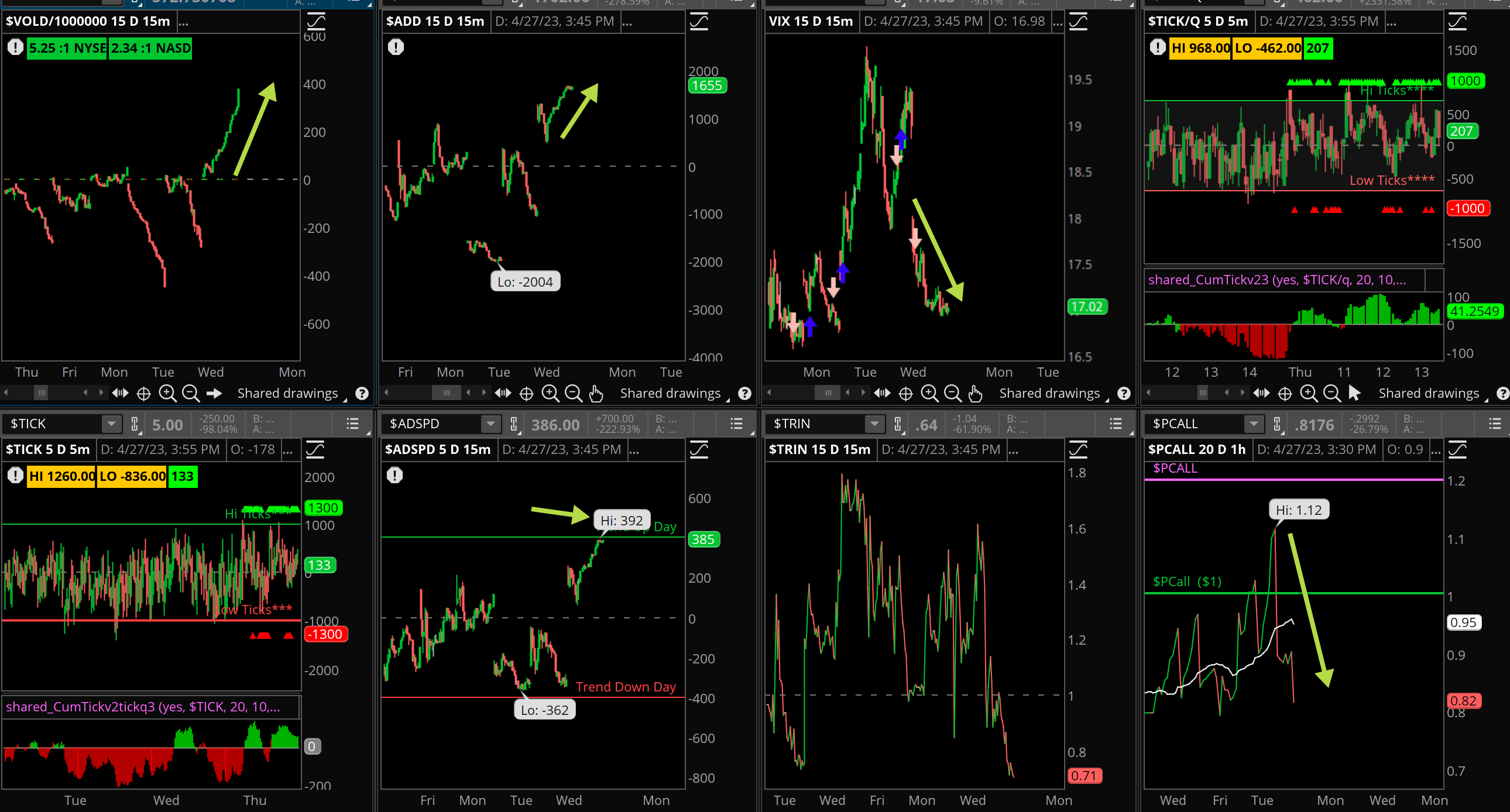

Big turnaround in breadth, another positive day and this will be on a buy signal.

Volume trends were better today, but with so much news coming out and the heavy selling that occurred earlier in the week, no surprise to see markets turn around quickly as short covering played a role.

What’s it mean?

That was quite the bounce back from a moderately oversold condition. The VOLD started out strong and finished the same way, with the put/call ratio notably down off Wednesday’s highs. VIX remains under pressure while the ADSPD nearly put in a trend up day. Good news for the bulls, we’ll see if there is followthrough later today.

The Dynamite

Economic Data:

- Friday: PMI, Employment Cost Indext, PCE, Michigan consumer sentiment

Earnings this week:

- Friday: XOM, , CVX, CHTR, CL, LAZ

Fed Watch: After a bunch of Fed speakers last week we head into the quiet period before the May 2/3 committee meeting. Fed funds futures are showing an 85% chance of a 25bps rate hike at the meeting.

Issues/Stocks to Watch this Week

Earnings – A huge amount of names report this week, more than 1000. Will they beat and raise guidance for the year?

GDP Q1 – First look at the US earnings, Atlanta Fed GDPNow reduced Q1 to 1.1%, and they were spot on.

Housing Data – With a sharp drop in interest rates, there is a slew of data out this week that will give us good information on the health of this sector.