The Fuse

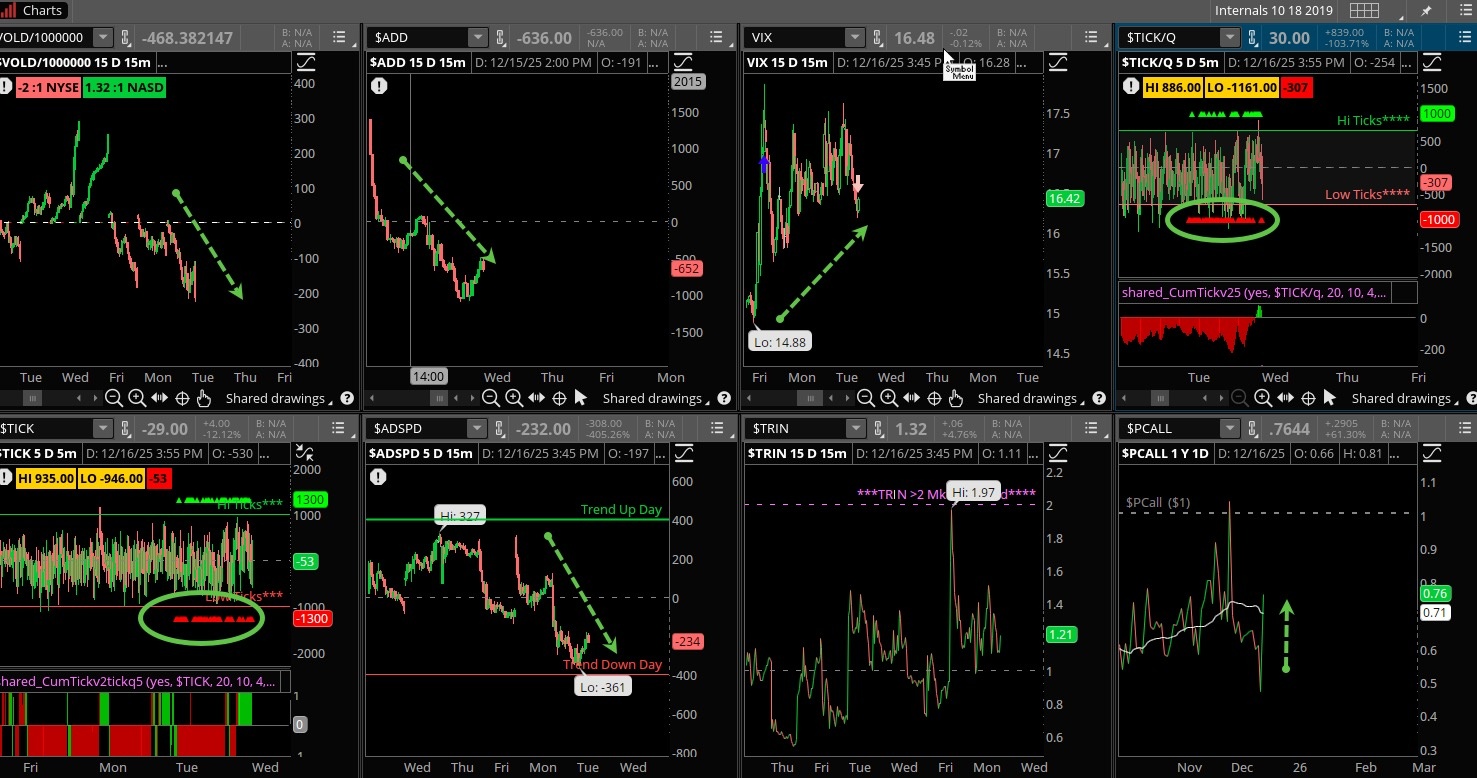

Equity futures are rebounding modestly but are still down for the week. Perhaps three days in a row of down is going to be enough to get buyers off the sidelines. Coming up on a short week of trading (next week) we could see volatility come down a bit more, but they are still rather low. Today January becomes front month on volatility and there is a healthy premium between VIX and the vx futures, so that is bullish for markets (but it is a condition).

Interest Rates are up again across the curve as worries over inflation continue to persist. A couple of fed governors took this stance again yesterday, wages were strong in the November labor report released yesterday. High yield spreads are tight and continue to thrive in a strong economic environment. Fed futures mostly unchanged, January cut seems to be off the table.

Stocks were up again in Europe, the STOXX higher by .3% led by increases in Germany and France. The FTSE added a robust .9%, dollar index up strong by .3%, yields on 10 yr US treasuries rose 2bps, in Germany down 1bp. Gold is up slight while silver rips higher again, crude oil bouncing back – up 2%. Japan climbed .3%, Hong Kong and Shanghai with nice gains at 1% or better.

Earnings last night from Lennar were a miss and the stock is down sharply on the news. General Mills had strong earnings and is up a bit this am, also Jabil is reporting numbers. Tonight we hear from Micron, tomorrow am Accenture, Darden, Factset, Carmax, Birkenstock and Cintas.

Stocks were down from the start and barely made a run at the unchanged level, preferring to let this day go as a loss. That makes three down sessions in a row, not common over the last several months but the bears are serving notice. Can the bulls get back on track? Most definitely, but it is going to take some heavy lifting volume to make it happen, otherwise there is just chop trading at best.

Another poor breadth day now has the bulls on their heels. Oscillators are now negative, and that may not be a tragedy yet but clearly the traders are not interested in adding stocks. Poor breadth is often a pre-cursor to worse action, we’ll have to see if it materializes. New highs still ahead of new lows but barely, Nasdaq is firmly in the red, more than 100 new lows vs highs yesterday.

Chalk up another day of distribution, these are starting to cluster and could be signaling some more weakness down the road. Professional selling is a sign that big money is getting out of the way, often before a spurt of selling occurs. We have seen this happen lately, early November before the bulls came to the rescue around Thanksgiving. At the time, there was plenty of opportunity to get on board, but sellers are starting to make some noise. Time for doing LESS.

The SPY tested the 50 moving average yesterday, the Nasdaq sank below it, the small caps and Industrials are still well above it. We could see a bit of movement lower in these indices, the problem being they will drag the others down with it. .

The Internals

What’s it mean?

Quite the bearish day for the internals, the VOLD weak as was the ADD, the ADSPD nearly had a trend down day. Put/calls raced back up, the ticks were mostly red, especially on the bruised Nasdaq. VIX was higher but is still reflecting complacency. Just nothing positive out of the internals this day.

The Dynamite

Economic Data:

- Wednesday:Fedspeak

- Thursday:Jobless claims, CPI, Philly fed index

- Friday:Existing home sales, consumer sentiment

Earnings this week:

- Wednesday:JBL, GIS, ABM, TTC, VERU, SPIR, NMTC, MU, WS, EPAC, MLKN

- Thursday:ACN, FDS, DRI, KMX, CTAS, FCEL, BIRK, ISSC, NKE, FDX, KBH, BB, AVO, SCHL, HEI

- Friday:CCL, CAG, LW, PAYX, WGO

Fed Watch:

Well the Fed did their thing last week and cut rates one more time, bringing the funds rate to 3.5%. That is still a bit restrictive policy but Chair Powell indicated that may be the last cut for awhile. The projections indicate one cut in 26 and one in 27, which may be pulled up. so that means a 3% rate by beginning of 2027, which may be the right policy figure. Lots of fedspeak this week before the holiday takes hold.

Stocks to Watch

AI – Much angst at the end of the week over some worries on the growth path of AI. Too much spending? Too much capacity? Even the dot.com days of 2000 when overbuilding happened seems to weigh on everyone’s minds. Expect some resolution soon.

Financials – Banks had a strong week as rates were lowered, this will help businesses grow and along with it bank loans. JPM was beaten down but came back in a huge way end of week. Looking for some continuation into the end of the year.

Volatility – The VIX is curiously low here with quite a bit of uncertainty, but perhaps it will just stay low until year end. We often see that happen but with recent saber rattling about rates, employment and inflation we could see more traders taking protection.