The Fuse

Equity futures are up modestly on this triple witching Friday. Options, options on futures and index options expire today. We are likely to see a heavy volume print end of day and some volatile action, though with a holiday shortened week coming up the VIX will be under pressure.

Interest Rates are up this morning as bond traders take some profits into the weekend. No doubt rates could be headed lower after the better than expected CPI from November. Some wrangling though about the. data but it certainly showed prices coming down. High yield spreads remain tight, fed funds futures now see a better chance of a cut at the March meeing (55%), but not much more in 2026 priced in yet.

Stocks are mixed this morning and more subdued, well off their highs from overnight. In Europe the STOXX was flat, France barely up, the same for FTSE. The dollar index climbed .2%, gold is slightly down but silver and crude are higher. German 10 yr bund yields and US treasury 10 yr yields both rose 2bps, In Japan the Nikkei gained 1%, Hong Kong and Shanghai with solid gains.

Earnings last night from Nike and FedEx beat cut expectations but these stocks are not inspiring much confidence. No clear catalysts to improving their businesses, the charts were not looking bullish. KB Home also reported a weak number. Later today we’ll have Carnival.

Good but not great breadth yesterday as the bulls managed to end the slide at 4 sessions in a row. But, the A/D was not all that impressive, a 16-10 advantage that rings hollow after the strong showing by the indices. Tells you there is not a strong commitment on the bull side. Oscillators are moving higher though and through the zero line, we look for seasonal trends to start taking hold over the next couple weeks.

Decent volume but the trends are still bearish. A one-off rally day on low volume does not constitute good conviction, and there is some worry the bulls may not step up and play. Look for a big volume print by the close today as this is triple witching options expiration.

A decent CPI report had the bulls energized early and often Thursday, perhaps the 4 day pullback was enough to tag some support levels, like the Nasdaq did with the 50 day moving average. We have seen these ‘one day wonders’ before however, and if the bulls go on strike the sellers may re-appear today.

The Internals

What’s it mean?

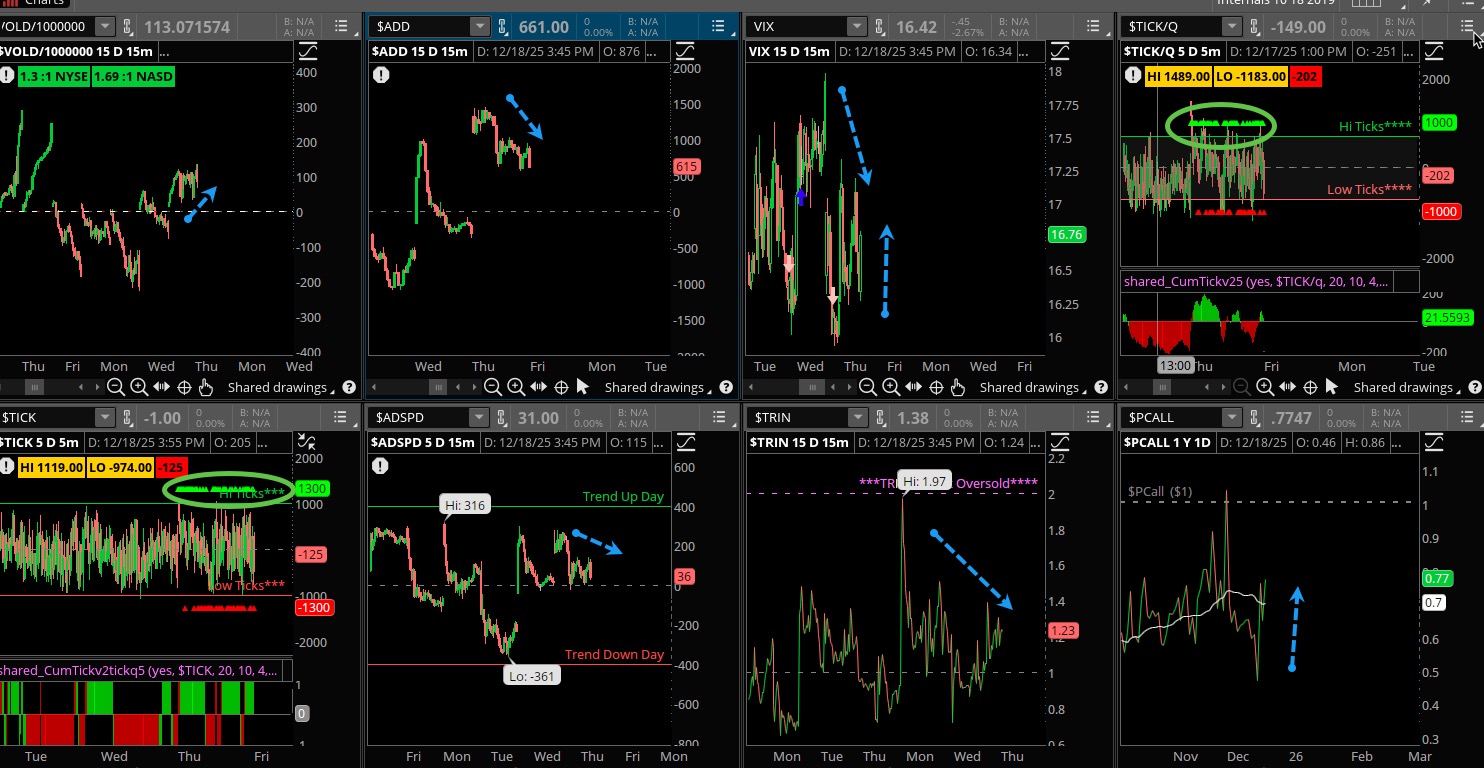

Positive day for the internals but just not overwhelming. Sure, the bulls pulled it out and the internals were bullish but it could have been so much better! Still, VOLD green and the ADD positive is good showing, PUT/CALLS down and the VIX down sharply was a good sign. Ticks were mostly green as the buy programs were over the top. Good, not great day for the internals.

The Dynamite

Economic Data:

- Friday:Existing home sales, consumer sentiment

Earnings this week:

- Friday:CCL, CAG, LW, PAYX, WGO

Fed Watch:

Well the Fed did their thing last week and cut rates one more time, bringing the funds rate to 3.5%. That is still a bit restrictive policy but Chair Powell indicated that may be the last cut for awhile. The projections indicate one cut in 26 and one in 27, which may be pulled up. so that means a 3% rate by beginning of 2027, which may be the right policy figure. Lots of fedspeak this week before the holiday takes hold.

Stocks to Watch

AI – Much angst at the end of the week over some worries on the growth path of AI. Too much spending? Too much capacity? Even the dot.com days of 2000 when overbuilding happened seems to weigh on everyone’s minds. Expect some resolution soon.

Financials – Banks had a strong week as rates were lowered, this will help businesses grow and along with it bank loans. JPM was beaten down but came back in a huge way end of week. Looking for some continuation into the end of the year.

Volatility – The VIX is curiously low here with quite a bit of uncertainty, but perhaps it will just stay low until year end. We often see that happen but with recent saber rattling about rates, employment and inflation we could see more traders taking protection.