The Fuse

EQuity futures are modestly soft here but that could change a bit later as some data is released. Tomorrow we’ll have the November jobs report and and wages. Overnight bitcoin tagged the elusive 100K level and now appears ready to push through there to more new highs.

Interest Rates are again notching a bit higher today as bond sellers trim some gains and prep for next week’s Fed decision. Chair Powell spoke yesterday and did not give many clues as to the committee’s direction other than ‘they are trying to find the neutral rate’ and letting the ‘data lead the decision-making process’. Same as it ever was!

Stocks are looking to break out of a range this week and it might be bitcoin that takes the lead. The crypto hit 100K last night and may roar higher from here. Overnight stocks in Europe stabilized, the French government was tossed out as that country’s stock market saw a bit of volatility. The Industrials closed above 45K for the first time ever, the dollar fell .3%, crude oil is down about .5% while gold and silver are flat. Hong Kong stocks were down nearly 1%, Japan and Shanghai negligible gains.

Earnings last night from Five Below were very strong, but weakness was seen in Synopsis and American Eagle. This morning earnings from TD, Signet and Dollar General while tonight we hear from Ulta, Veeva, Gitlab, LuluLemon and Docusign.

A super strong day again as buyers just poured it on all session and really kicked it into high gear following an interview with Chair Powell at Dealbook. He did not say too much to tip the Fed’s hand, remember they have a meeting next week where they are likely to cut rates one more time. The market is expecting that policy move and would be highly disappointed if it did not get a cut. That said, stocks are pretty much overbought now and could be due for a pullback at any moment.

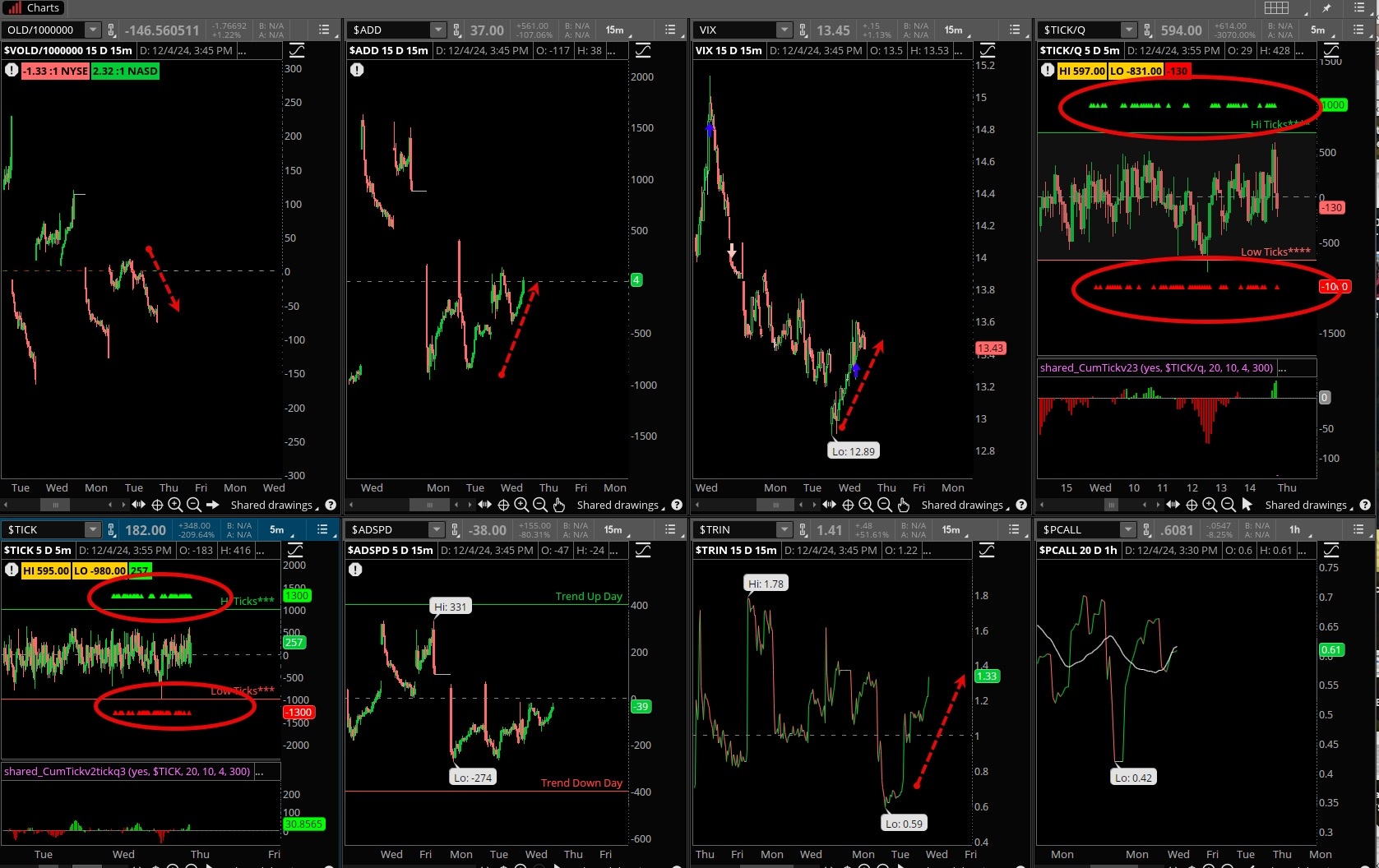

It would have been nice to put a solid breadth day as a bow on this session but it was not to be. It was a mediocre breadth day, not even close to matching the price action. It tells us the under that hood internals are not supporting the price action at the moment, and that could be troublesome if the internals like breadth, depth and volume don’t improve. We always consider the price action as king so let’s not jump off a bridge just yet.

A really good volume day yesterday as the influence. from Salesforce was evident. Strong turnover on the QQQ, DIA and SPY notched accumulation days, nice to get these when the indices are hitting new all-time highs. We could see more volume start coming in later in the week when the jobs data is released Friday.

Without checking back to support levels the market becomes more and more vulnerable to sharp pullbacks. As it is, the overbought condition is getting curated and will be well overbought in a couple of sessions. Does that mean doom? Of course not, but don’t be surprised if there is a slew of selling that shows up before next week’s Fed meeting.

The Internals

What’s it mean?

It would be delightful if the internals would simply confirm the price action but that is not happening. For days now there breadth, VOLD, ticks and other internals have simply been mediocre. This is not a dealbreaker for the indices though, but looking at weakness in VOLD and VIX starting to rise again should give the bulls concern. Ticks were evenly distributed, the ADD actually improved on the day.

The Dynamite

Economic Data:

- Thursday:Jobless claims, US trade deficit

- Friday:NFP report, consumer sentiment, consumer credit, Fedspeak

Earnings this week:

- Thursday:DG, TD, CSIQ, SIG, BMO, CAL, KR, CM, LULU, PATH, ULTA, DOCU, GTLB, HPE, IOT, VEEV, ASAN, WOOF

- Friday:GCO

Fed Watch:

Not much fanfare as only a couple of fed speakers this week, Goolsbee and Musalem. Most of the chatter recently has been worry about sticky inflation, the data has been telling us this as well. The next Fed meeting is Dec 10, the last of the year, the market is looking for a cut but may be disappointed.

Stocks to Watch

Sentiment – No question momentum is on the side of the bulls. This is the first week of trading in the most bullish month of the year, and coming off a spectacular November the best bet is on a continuation rally. This week is important to see if that momentum continues or if the market is looking to take a rest.

Retail Stocks – Coming of a very strong first holiday weekend, we may see a pop in some retail names as these companies ready for a big finish towards Christmas. Pay attention to deals and discounting.

Energy – Oil has been going sideways a bit but with a OPEC meeting coming up soon that may change, if the cartel decides to slice production.