The Fuse

Stock futures are modestly higher today as equity players try and decide if February will go out with a bang or a thud. It’s been a rollercoaster ride this month and nothing may be different come March.

This 4000 is pretty sticky right here, short term moving averages are converging at this level. Volatility remains muted, we have seen some moves up and down as we did on Monday but the bias is still neutral.

Overnight we saw more high inflation readings from Europe. Spain, France and Italy all delivered higher than expected numbers from last month. We’ll get a read on the last meeting minutes later this week. Target earnings beat on the bottom line but the company offered horrendous guidance for 2023.

Good earnings report from Zoom last night while Workday beat and raised guidance. These may move sharply today.

The only event here is the end of the month, the SPX 500 stands at 3982, which is down 2.1% on the month. Tomorrow is a big investor event for Tesla.

Pretty strong breadth early in the day but sellers decided to cut positions as we only saw the leaders ahead by 16-12. A virtual standoff.

Volume was down from Friday, not what you want to see on an up session. Plenty of short covering hit early Monday and then after a bout of selling, the market went quiet.

Support is still around 3940, the 200 ma and then 3900 and 3802 on the SPX 500.

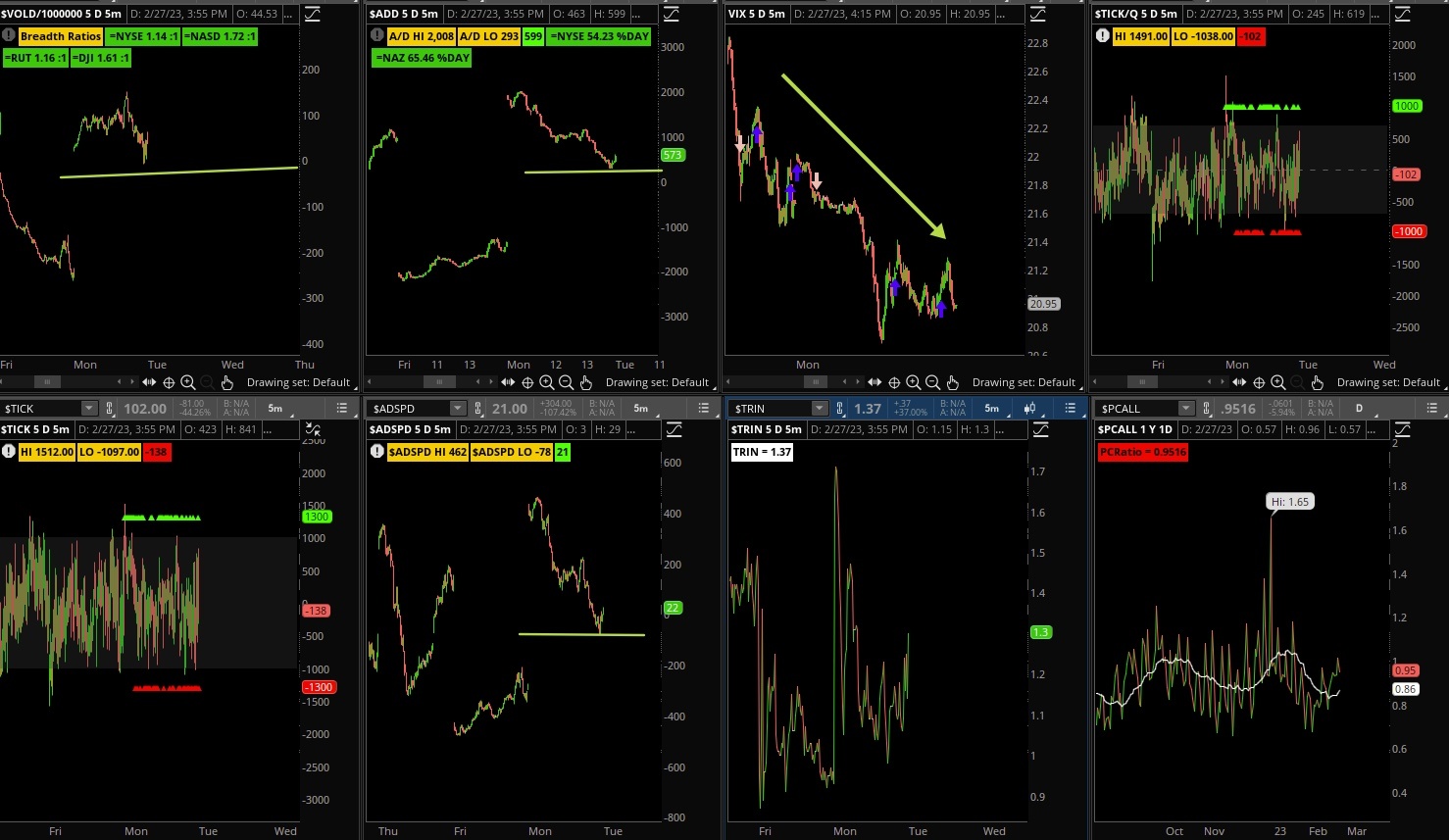

The Internals

What’s it mean?

It was a ho hum day as we see from the indicators. Nothing here really strayed too much from the zero line. When that happens and volatility drops, so does option premium. The ticks (top right, bottom left) were well contained, the ADSPD around the flat line as well. Perhaps some news will drive more activity, but this day was a dud.

The Dynamite

- Tuesday: TGT, NCLH, AZO, RIVN, NVAX, AXON, MNST

- Wednesday: LOW, WEN, CRM, DLTR, VEEV, SPLK, OKTA

- Thursday: BBY, COST, M, ZS, AVGO, JWN, DELL

- Friday: HIBB

US Economic Data:

- Tuesday: PMI, Consumer confidence, retail/wholesale inventories

- Wednesday: global PMI, ISM, construction spending

- Thursday: jobless claims, productivity, unit labor costs

- Friday: PMI services, ism non-manufacturing index

Fed Watch: A few speakers out this week will be talking about inflation and the economy. Last week we had the same situation, but speakers were much more hawkish than expected, talking up higher rates. We currently see a 25% chance of a 50bps hike in March, but plenty of data will be out before then.

Stocks to Watch

End of month, buying of stocks (window dressing)