The Fuse

Equity futures are mixed today as the markets attempt to make it three straight up sessions. We are seeing good early strength however in the small caps, IWM is trying to close above 230 for the first time since it broke down hard in mid December on higher interest rates (long term). Tomorrow’s NFP for January is likely to be a big market mover.

Interest Rates are modestly higher in the early part of the day but that could certainly change with some important economic data released later in the morning. Fed futures remain steady and looking for the next cut to be in either June or July. GDPNow is showing a nearly 4% GDP expectation for this current quarter which begs the question, why does the Fed need to cut at all?

Stocks are rising across the globe, in Europe the STOXX gained .5%, both France and Germany were higher on the day. Gold is backing away from all time highs, silver remains robust, crude oil up .6%. The dollr remains strong, up .3%. German 10 year bund yields rose 2bps, 10 yr US treasury climbed the same amount. Stocks in Asia were higher, Japan gained .6%, Hong Kong and Shanghai up sharply, better than 1.3% each.

Earnings last night were not so hot as Qualcomm, ARM and Align are lower following mixed guidance. This morning a nice beat for AMSC and Lilly, which provided in-line guidance. Tapestry beat and guided up, Yum beat and guided sales slightly higher, strong numbers from Taco Bell. Tonight we have Amazon, Fortinet, Affirm, Cloudflare, Microchip, ELF, Pinterest and Powell.

It was important to see the bulls come back and deliver a win. Markets have been teetering of late right near the all-time highs and just cannot seem to find buyers to cross the finish line. No question we believe the time is coming for new highs to be achieved, specifically on the SPX 500, Industrials and Nasdaq. Sooner rather than later, as the indicators intermediate term continue to support the effort. February is notoriously weak historically after a strong January, but there are several days left to play out and plenty of news as well.

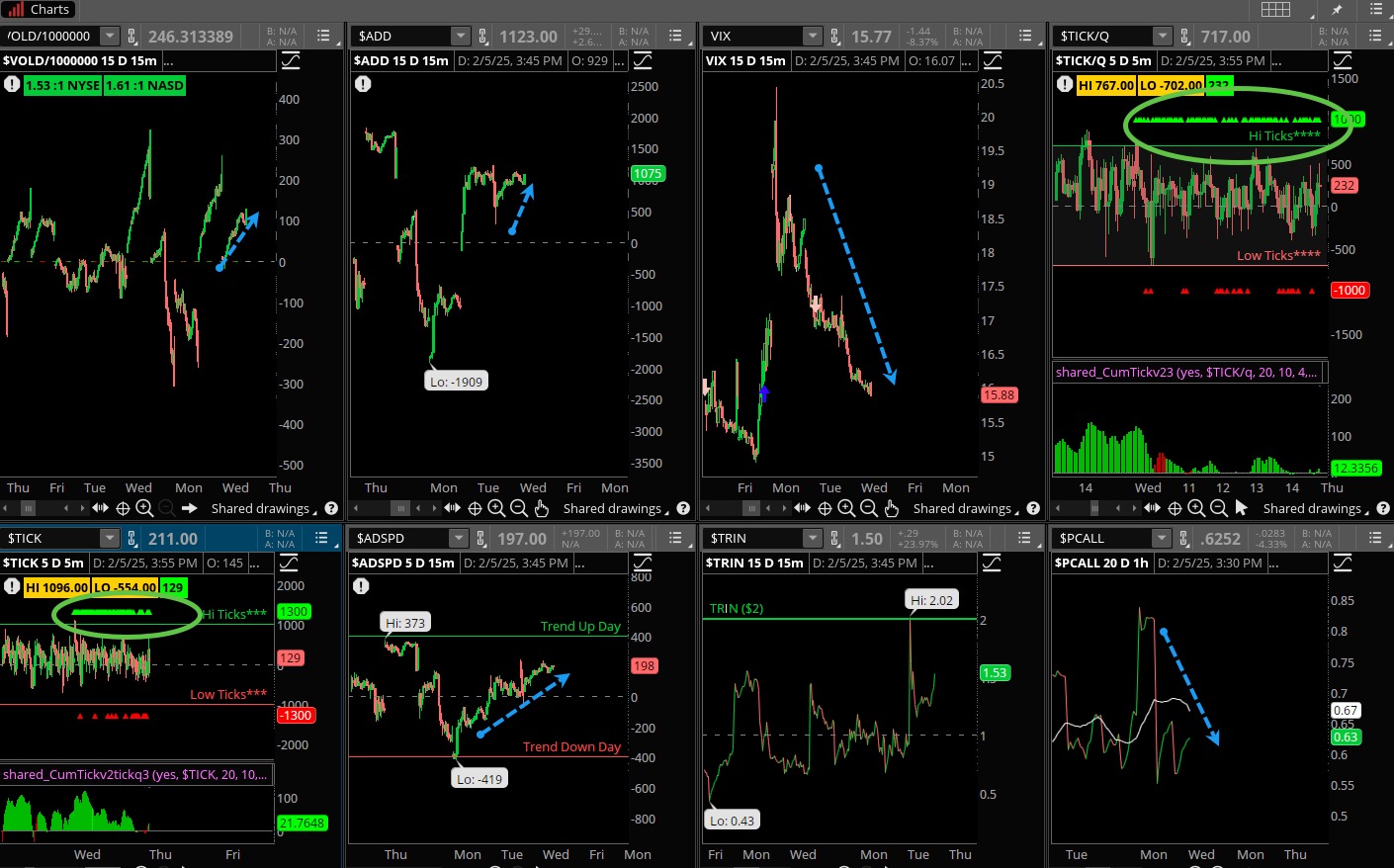

Another positive day of breadth is good news if you’re a bull. Though early on in the trading session it did not appear we would see the light of day. Stocks were slammed hard as a result of poor Google earnings along with Uber and poor action in Disney. But the dip buyers were active again and pulled off a win by the end of the session. Oscillators are now firmly above the zero line, new highs trounced new lows once again, that indicator remains on a buy signal.

Volume trends are not really showing their hand right now. Only the DIA gave an accumulation day while the other indices were positive but not nearly as much turnover as Tuesday. That is worrisome only to the extent a lack of commitment at these higher levels could make stocks vulnerable. Regardless, the price action is still positive and with dip buyers stepping in when stocks go down we will eventually feel some of that heavy volume.

Each day that the market dips and gets bought up like yesterday is another day of fortification for the uptrend. It was a dazzling display of no fear by the bulls, where the market was taken lower by sellers only to rise back up and close at the highs of the session. That is a signature move for a bull market.

The Internals

What’s it mean?

A solid performance by the internals, good strong breadth and VOLD picked it up, too. Put/calls sank as did the VIX, which tells us sentiment is bullish here, investors see no harm done on the horizon.

That sort of complacency is worrisome though, but won’t matter until the chart breaks. TICKS were green and strong all day, plenty of buy programs hitting all session long. A followthrough day for the bulls would be encouraging.

The Dynamite

Economic Data:

- Thursday:Jobless claims, productivity, Waller and Logan speak

- Friday:Jobs report, Bowman speaks, wholesale inventories, consumer sentiment and credit

Earnings this week:

- Thursday:LLY, RBLX, COP, PTON, HSY, BMY, TPR, YUM, POWL, PINS, FTNT, AFRM, AMZN, ELF, NET

- Friday:CBOE, NWL, KIM, FLO

Fed Watch:

After last week’s Fed meeting we have a slew of speakers set to talk it up. This coming week is big for data, including the January jobs report. The committee’s decision to sit on rates for the first time since last July at this point was telegraphed, and the next meeting in March is likely to be the same conclusion. The data is going to guide them toward policy, right now it is in pause mode.

Stocks to Watch

Jobs Data – After December’s surprisingly good report the consensus is for something a bit less. Chair Powell and the committee seem pleased with the employment situation, 4.1% unemployment is a good place the for economy to continue growing.

Big Tech Earnings – We will hear from Amazon and Google this week among a smattering of other names in various sectors. Earnings have by and large been pretty strong this season with solid guidance. Let’s see if that continues.

Tariff Response – Tariffs are suddenly on the table, whether for real or a threat. Twice this week the stock market reacted negatively to the news, volatility rose up and pushed markets down for a time.

That has to be worrisome to the bulls but opportunistic to everyone.