The Fuse

Equity futures are weak this morning following a volatile session Thursday when the SPX 500 fell 1% at one point but did manage to rally back sharply by the close. It’s clear the indices are in a mild distribution just before the biggest earnings reports hit later this month. Further, uncertainty and turmoil in the Middle East has investors worried in the short run and deciding to exit stocks for now rather than wait it out.

Interest Rates are modestly higher on the long end of the curve in pre-market as traders await the critical PPI inflation report. Yesterday’s move by markets and rates following a HOT CPI was indicative of the volatility in a market that has plenty of uncertainty. The worry of course is if inflation no longer declines and sticks above the Fed’s goal of 2%.

News of a strike by the US/UK contingent led air strikes over Yemen in response to persistent attacks on ships in the Red Sea. This has brought on some nervousness in markets and the reaction in crude and gold is real, with crude oil higher by 4% and gold up by 1.5%.

Other commodities are catching a bid as well.

Earnings were out this am on some big banks, most beat earnings estimates though JPM and BAC missed revenue forecasts.

WFC beat both top and bottom line, UNH came in with a beat but is getting hit on weaker costs. Delta came in with strong numbers again but only guided in line.

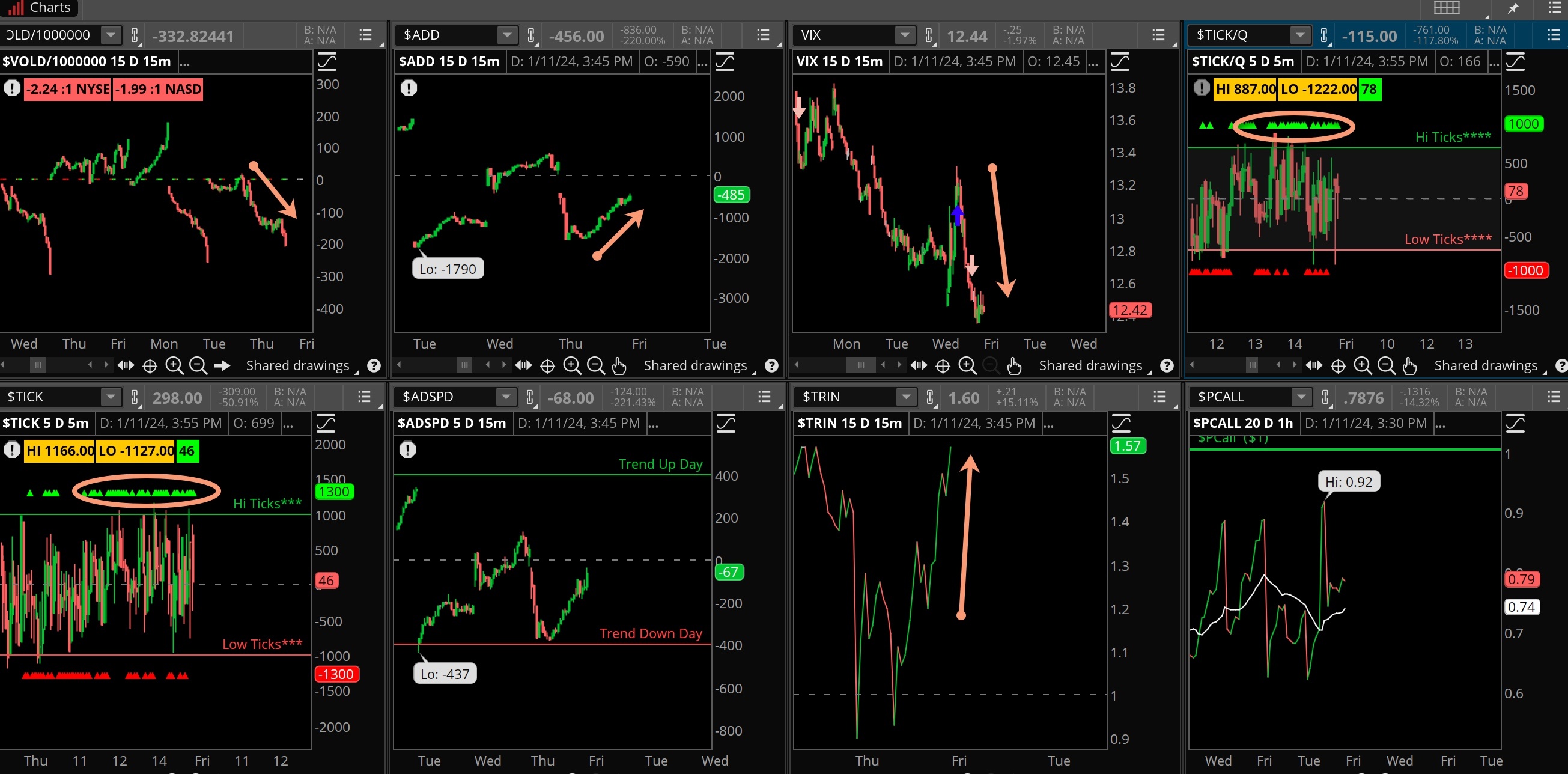

Breadth was negative once again but improved during the day. There is has been nary a bid this week following Monday’s very strong numbers. This indicator is now on a sell signal, though it flips back n’ forth. We could be hitting a soft patch in the market action here in the coming days until the end of the month.

Volume rose up on Thursday as it appeared we might see a day of distribution, but prices made a stick save and finished well off their lows. Still, the action was pretty bearish all day long especially for the industrials, but they did manage to post a win. Today may bring some heavy turnover as we end the week following the release of a big economic number.

Overnight futures showed some good strength but by the opening bell it was all for naught. The highs were just inder 4,840 and if we had opened there it would have been a new all time high. Resistance for the SPX is still at 4,800 as that level seems to be something of interest. Perhaps the PPI number, if benign and taken will will be the catalyst to bring markets to new highs before the holiday weekend.

What’s it mean?

Stocks were drilled most of the day yesterday following some hot CPI numbers. The internals however were rather mixed, notices the divergence in VOLD and ADD, the latter strengthening as the day went on. That same theme followed the TICKS where we saw the green arrows accumulate later in the day. This caused a distortion with up/down volume vs issues, hence a rise in the TRIN. That will be corrected today.

But the picture is mixed here, we have a three day weekend so we often see volatility sold into the holiday.

The Dynamite

Economic Data:

- Friday: PPI

Earnings this week:

- Friday: BLK, BK, C, DAL, JPM, UNH, WFC, BAC

Fed Watch:

The release of the prior meeting’s minutes last week struck a tone of cautious optimism. On the one hand, the committee seemed pleased with the trend of inflation coming down and acknowledging their strong rates have been working. On the other hand, they dismissed the ‘all clear’ signal completely, preferring to err on the side of caution even as the economy starts to slow down. They introduced the idea of rate cuts in 2024 but refused to say when, keeping with their style of waiting on the data. This week might have some member talking down the rate cut expectations set in futures markets.

Stocks to Watch

Oil – Crude oil has been creeping higher of late in response to turmoil in the red sea but also likely due to more supply constraints.

That will keep a nice bid under crude as we see WTIC make another run towards $80. The chart is getting bullish here.

Banks/Financials – Friday is the first big day of earnings for Q4 and we’ll hear from some big major banks (see above). What they say about their business, credit, liquidity and financial conditions will be crucial. These stocks have run hard for three months so any bit of caution is likely to get slapped down.

Apple – A couple of downgrades this week following the end of the quarter has put Apple investors on their heels. In years past these pullbacks have been tremendous buying opportunities, is this going to be another one? The stock tagged the 200 ma on Friday.