The Fuse

Equity futures are getting hammered this morning but are well off their overnight lows. Rates continue to creep up as the market battles with inflation news later this week and comes to the realization the Fed is not going to help much with rate cuts. Friday’s job report signaled a very strong economy not in need of help yet.

Interest Rates have turned around this morning, up slightly but now lower as bond buyers step in before the big inflation reports this week (CPI, PPI). Perhaps just a little short covering though, after bonds have been sold off sharply over the last month. The first Fed meeting of the year is in a couple of weeks and many believe now the committee will announce a pause in policy for the foreseeable future. Fed futures then may start pricing in rate hikes if inflation does not fall more precipitously.

Stocks in Europe were lower across the board, the STOXX down .5% overnight. The dollar continued its ascent, gold hammered by about 1% while crude oil is in a bullish trend, up another 2.4%. German 10 yr bund yields rose 3bps, US treasury 10 yr yields rose 2bps, Stocks in Asia were lower, Hong Kong down 1% and Shanghai off .2%>. Japan was closed.

Earnings begin this week in earnest for the banks, we’ll hear from Goldman, JP Morgan, Citi, Blackrock and TSM among others. Some of these names have been drilled in 2025 but their charts show the froth being wiped away, which might bode well for a bullish earnings response.

It’s all about the economy and inflation this week. PPI, CPI and retail sales for December, a good read in on prices and how the holiday shopping season fared. The jobs report last week was strong and portrays a strong consumer, so retail sales might be a beat this coming week. However, sticky prices continue to be bothersome to the bond market and the Fed, nowcast estimates see headline inflation at 4.6% for December, core at 3.6%.

Breadth was horrendous Friday, this indicator is now on a sell signal for the time being. This past week has been all about the breadth and new lows, which continue to expand. That indicator is on a sell signal. Oscillator are bearish but are enough oversold enough to expect a big rally yet. If there is follow-on selling then that could happen later in the week.

Volume was elevated again Friday so another distribution day was notched. That is the 3rd one in 2025 and part of a cluster if you include December. That is bad news for the bulls and the intermediate trend, which is in jeopardy of turning down. High volume moves to the downside indicate big institutional selling is at hand, time to step out of the way.

There is some strong support lower but as we stand now the SPX 500 is right on the 100 day moving average, an area where the market has recovered in the past. Yet, with indicators still pointing in the downward direction the weight of evidence is on the bulls. Price action has been stingy this year, small caps are struggling and remain in correction mode. It seems many in the finance community are loathe to accept it, but the markets are correcting as we speak.

The Internals

What’s it mean?

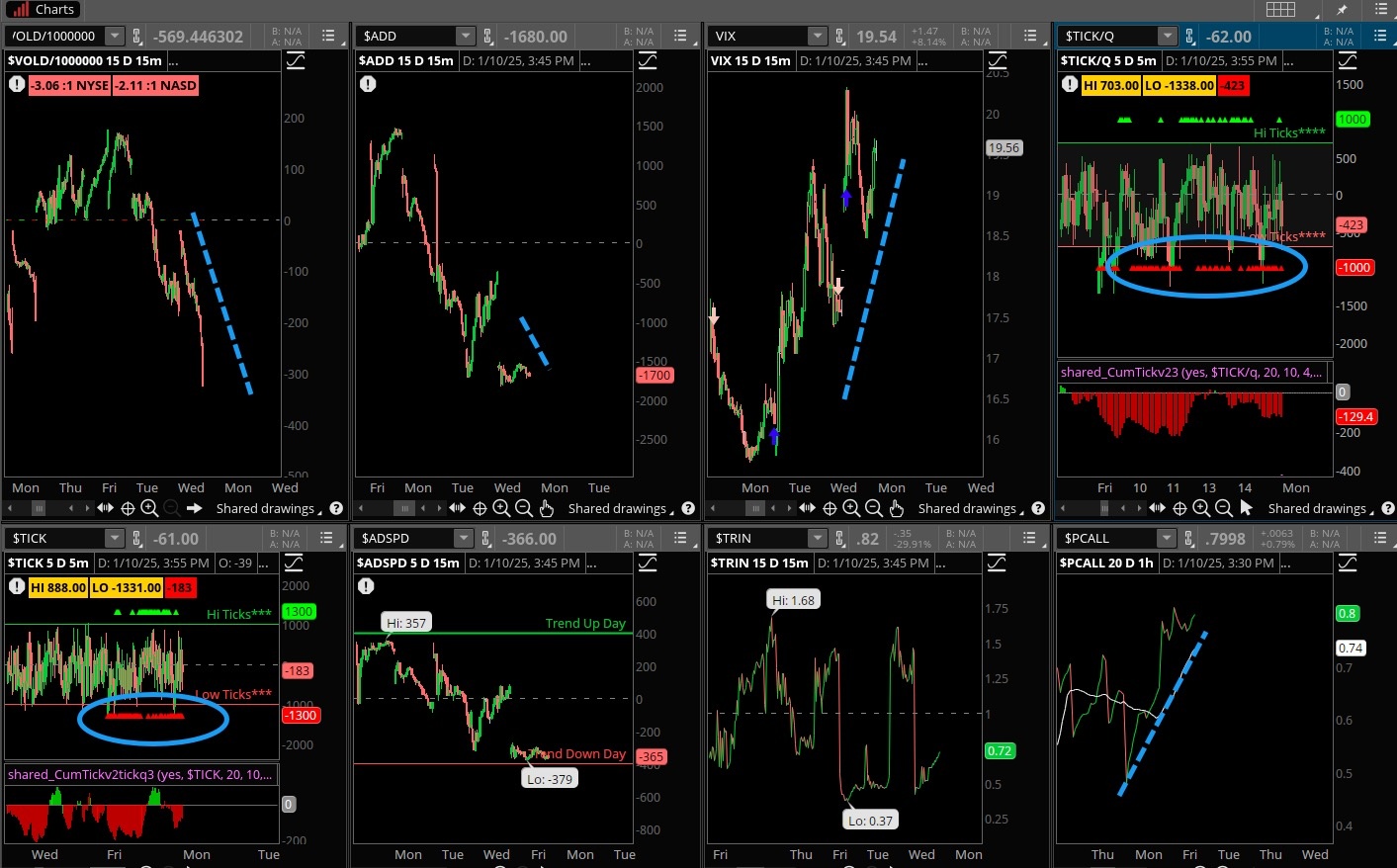

More nasty internal data as the VOLD just collapsed from the start of trading and never looked back. ADD was down all day as well, put/calls are on the rise as is the VIX. It all adds up to a very poor market here, the internals have been flashing this signal for weeks. Ticks very red, solid sell programs all session long.

The Dynamite

Earnings this week:

- Monday:KBH, AEHR

- Tuesday:CVGW, KARO

- Wednesday:C, JPM, WFC, BLK, BNY, FUL, SNV

- Thursday:TSM, GS, BAC, UNH, MS, USB, PNC, INFY, MTB, JBHT

- Friday:SLB, RF, FAST, TFC, STT, SFY

Economic Data:

- Monday:US Federal Budget

- Tuesday:PPI, NFIB optimism

- Wednesday:CPI, empire state index

- Thursday:Jobless claims, retail sales, philly fed, homebuilder confidence, business inventories

- Friday:housing starts, building permits, industrial production, cap utilization

Fed Watch:

Several Fed speakers are out this week and they will have some data to discuss. The prior week we heard from the rather hawkish Mikki Bowman who stated that rate cuts are unlikely for the foreseeable future. That notion comes from higher inflation and strong growth following the solid December payroll report. Five speakers through Wednesday will give us a preview of fed policy as they see things unfold.

Stocks to Watch

Yields – Bond yields moved up this week, the 10 year tagging 4.8%. That is not surprising as the trend in bonds has been to sell fixed income. But is it too bearish? We’ll find out later this week.

Volatility – January is not acting as many would have hoped for, with high volatility and poor data. The VIX is at relatively high levels now, higher than it’s been in over a month and trending upwards. If that continues so will the market correction.

Bank Earnings – We’ll hear from the major banks this week including JPM, GS and MS. They have been floundering of late but that could be a nice opportunity to add some shares on the cheap.