The Fuse

Equity futures are rallying this morning, attempting to put together a third straight up session following some strong bank earnings early today and a rally from other markets overnight. With a moderately oversold condition stocks are ripe for a big rip to the upside if the conditions are right.

Interest Rates are actually falling a bit this morning, some good news for the bulls as there is optimism over long term interest rate trends. Perhaps the 4.8% yield on the 10 year is as high as we’ll go, but inflation readings need to be more benign. Growth is strong but so is inflation.

Stocks rallied smartly in Europe, higher by .3% while the dollar fell .1%. Yields in Germany fell 2bps while US treasury yields were also down 1bp. Stocks in Asia declined, Japan down .1%, Shanghai down .4% but Hong Kong up .3%. Gold, silver and crude are up.

Earnings begin this week in earnest for the banks, we’ll hear from Goldman, JP Morgan, Citi, Blackrock and TSM among others. Some of these names have been drilled in 2025 but their charts show the froth being wiped away, which might bode well for a bullish earnings response. Monday evening had some really strong numbers from KBH and guidance as well.

Chalk up another winning day for the bulls, though it was a close call until the end. The SPX 500 managed to squeak out a modest gain, the small caps were the star however, the IWM rising up more than 1% on the day. Tech stocks have been struggling though, the MAG 7 names all finished lower. With big earnings coming up next week in tech it’ll be interesting to watch the action and how traders respond to what is being said. It’s not a good policy to be bearish during earnings season, so any press into downside should be tempered.

Finally a good day of breadth but it needs some followthrough today, then there is a possibility of some bullish activity down the road. Oscillators are still negative however, the Nasdaq finished poorly but might have a turnaround day here. New lows continue to expand and trounce new highs. If breadth can string together a few good sessions there is a possible buy signal coming up.

Overall volume was okay but that means the participation was sparse. We have come to the point of the month where the bulls need to ‘put up or shut up’, basically step up and start buying stocks or risk more downside. Price action has been good but turnover has simply been mediocre. Even as small caps won the day Tuesday, the turnover was not much better than the prior few sessions.

It seems each day we have test of lower levels and before the dam gives way buyers step in to save the day. It is uncanny, but that’s life in a high volatility world. Stocks continue to slosh back n’ forth in a wide range, presenting good short term trading chances but with little followthrough. Eventually something is going to break one way or the other. The weight of evidence though is clearly on the bulls, seasonal weakness is upon us.

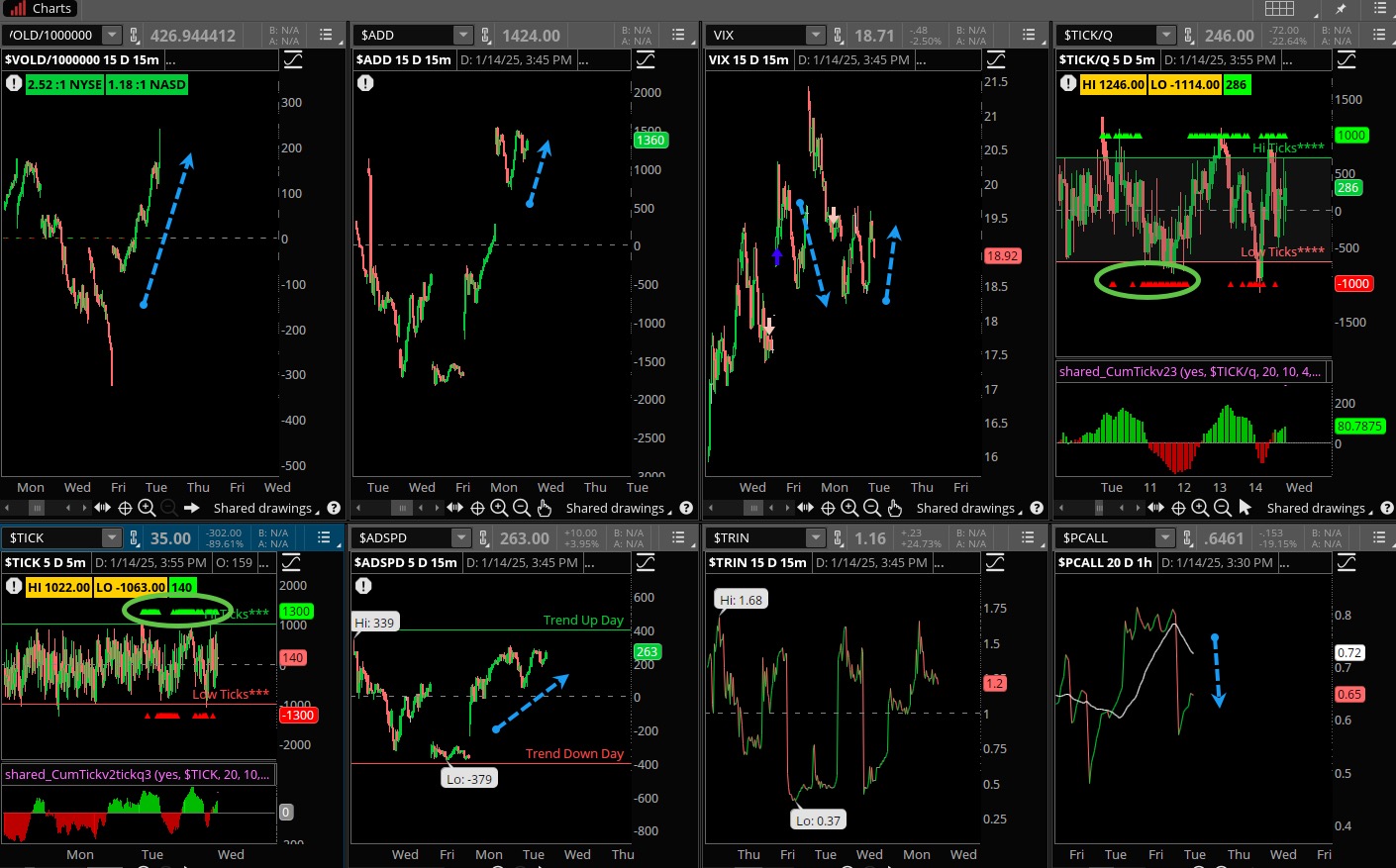

The Internals

What’s it mean?

Internals were actually pretty good most of the day but with some strong buy programs the last 10 minutes of trading the VOLD shot higher, the ADD finished positive while the ticks came in strong on the green side. Put/calls finally backed away as markets were pretty oversold in the short term. ADSPD was strong and finished on the highs, the VIX was — well, volatile – finished lower on the day. If CPI is taken well volatility sellers may get active.

The Dynamite

Earnings this week:

- Wednesday:C, JPM, WFC, BLK, BNY, FUL, SNV

- Thursday:TSM, GS, BAC, UNH, MS, USB, PNC, INFY, MTB, JBHT

- Friday:SLB, RF, FAST, TFC, STT, SFY

Economic Data:

- Wednesday:CPI, empire state index

- Thursday:Jobless claims, retail sales, philly fed, homebuilder confidence, business inventories

- Friday:housing starts, building permits, industrial production, cap utilization

Fed Watch:

Several Fed speakers are out this week and they will have some data to discuss. The prior week we heard from the rather hawkish Mikki Bowman who stated that rate cuts are unlikely for the foreseeable future. That notion comes from higher inflation and strong growth following the solid December payroll report. Five speakers through Wednesday will give us a preview of fed policy as they see things unfold.

Stocks to Watch

Yields – Bond yields moved up this week, the 10 year tagging 4.8%. That is not surprising as the trend in bonds has been to sell fixed income. But is it too bearish? We’ll find out later this week.

Volatility – January is not acting as many would have hoped for, with high volatility and poor data. The VIX is at relatively high levels now, higher than it’s been in over a month and trending upwards. If that continues so will the market correction.

Bank Earnings – We’ll hear from the major banks this week including JPM, GS and MS. They have been floundering of late but that could be a nice opportunity to add some shares on the cheap.