The Fuse

Equity futures are mixed this morning but the Nasdaq and ES futures are heading higher, looking to rally further to build on Wednesday’s monster run. However, rates are rising up this morning as that is helping to push small caps lower, and may spread to the rest of the market. Caution still warranted.

Interest Rates are slowing moving back up after getting blitzed yesterday. We might see more rise if retail sales are strong. Fed futures bumped down a bit and now expect to see perhaps two cuts in 2025, but that is still quite optimistic. Rates across the globe continue to creep up, inflation remains a problem.

Stocks were up nice in Europe, higher by .6% on the STOXX, Asia also climbed with the Nikkei up by .3%, Hong Kong a robust 1.2% and Shanghai higher by .3%. The dollar was flat, gold up about .5% and crude oil backing off about 1%. German 10 yr bund yields rose 3 bps, 10 yr US treasuries up 1bp.

Earnings yesterday from banks were strong and kicked off an optimistic earnings season. This morning strong numbers from TSM and BAC while we’ll hear from MS and others later in the day.

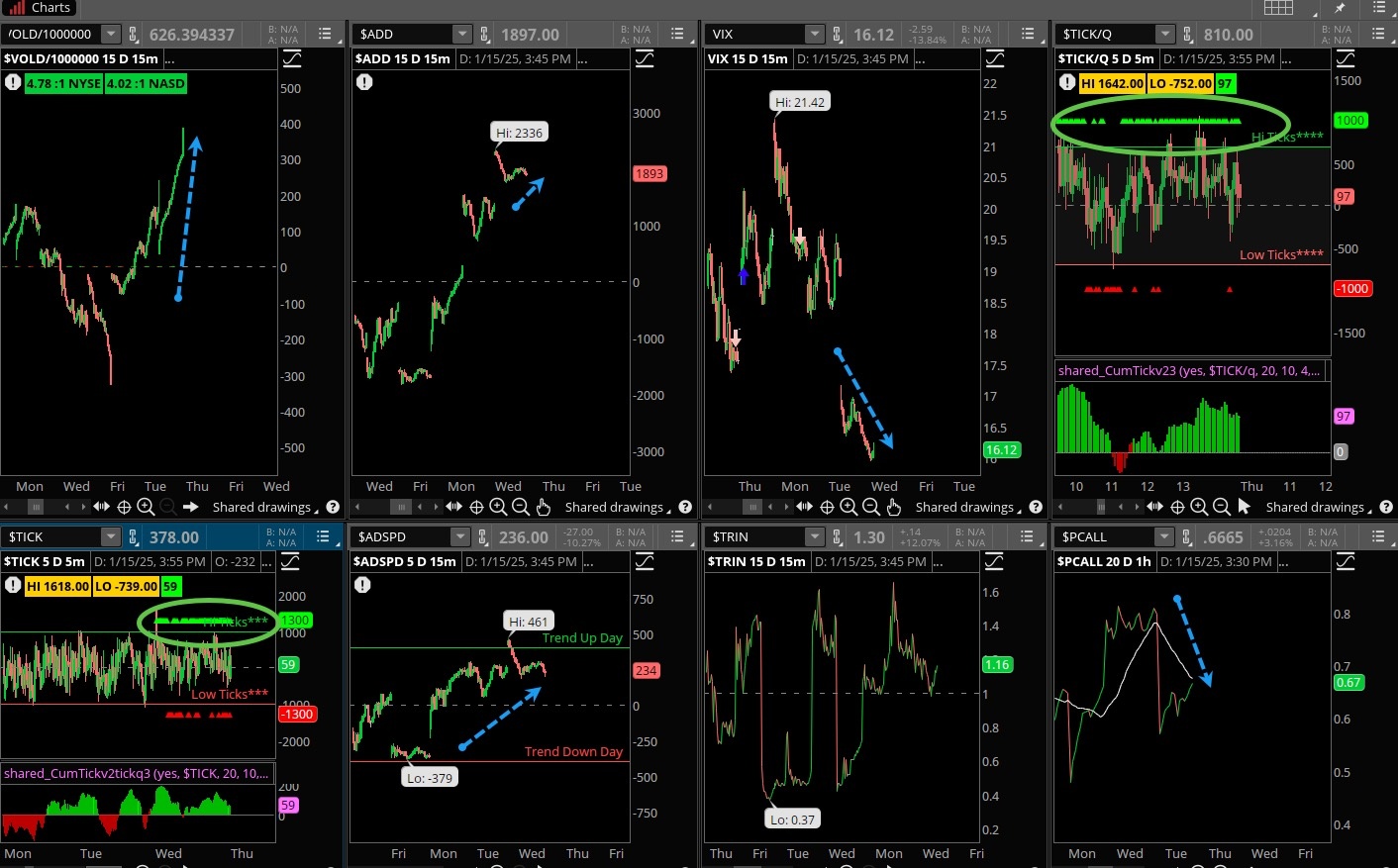

Who knows if the first couple of days this week were setting up for something, but clearly the bulls took some control of the situation on Wednesday and knocked one out of the park. It was a banner day paced by the banks, which several of them reported strong earnings and guidance. Not to mention the better than expected CPI number that helped put a whack in the VIX. Even breadth was good, as you’ll see below.

Breadth is finally back on a buy signal after struggling for weeks. Now, we’ll be looking for some followthrough and more positive breadth but pushing the oscillators well into positive territory is certainly an accomplishment. But, new lows are still advancing though much less than earlier in the month, it will take several trading days of strong cumulative breadth before that indicator turns bullish.

Good volume on the rebound as stocks started higher on the session as volume expanded. That is a huge positive, it was a solid accumulation day for the bulls. As always, some followthrough is key but that can happen over the next 5-7 sessions. Perhaps after the holiday and knee=deep into earnings season that will happen. But Wednesday was a good start.

The recent support levels held firm this week, The SPX 500 managed to hold down the 5,780 level after filling the gap left post-election. Nasdaq held firm just above the 100 day moving average but the start of the week has been the Industrials, which gapped up again and held a very tight range but closed just under the 50 ma. That could be problematic if the index does not penetrate it soon, but we’ll give it a few days to see if the bulls can make it happen.

The Internals

What’s it mean?

Yesterday we mentioned if the CPI were taken well then volatility sellers would be active. That was an understatement! The VIX was punished all day long following the news release, the VOLD finished strong and check out those ticks, Nasdaq was green nearly the entire day. A banner session for the bulls, the rout was on the from the start. ADSPD and ADD finished off their highs but we’ll give them a chance to post better numbers this week.

The Dynamite

Earnings this week:

- Thursday:TSM, GS, BAC, UNH, MS, USB, PNC, INFY, MTB, JBHT

- Friday:SLB, RF, FAST, TFC, STT, SFY

Economic Data:

- Thursday:Jobless claims, retail sales, philly fed, homebuilder confidence, business inventories

- Friday:housing starts, building permits, industrial production, cap utilization

Fed Watch:

Several Fed speakers are out this week and they will have some data to discuss. The prior week we heard from the rather hawkish Mikki Bowman who stated that rate cuts are unlikely for the foreseeable future. That notion comes from higher inflation and strong growth following the solid December payroll report. Five speakers through Wednesday will give us a preview of fed policy as they see things unfold.

Stocks to Watch

Yields – Bond yields moved up this week, the 10 year tagging 4.8%. That is not surprising as the trend in bonds has been to sell fixed income. But is it too bearish? We’ll find out later this week.

Volatility – January is not acting as many would have hoped for, with high volatility and poor data. The VIX is at relatively high levels now, higher than it’s been in over a month and trending upwards. If that continues so will the market correction.

Bank Earnings – We’ll hear from the major banks this week including JPM, GS and MS. They have been floundering of late but that could be a nice opportunity to add some shares on the cheap.