The Fuse

Equity futures are getting drilled this morning on fears that competitor DeepSeek is going to derail the AI revolution here in the US. Remember, there are a million reasons to sell but only ONE reason to buy. If you’re going to try and rationalize each selling moment it is a wasteful exercise. All you need to know is the market is overbought and due for a whack.

Interest Rates are falling in a safety trade for the markets. Bond buyers are back engaged to add more bonds, TLT is up sharply today as the long bond yield is getting hammered. Fed futures are still rather static, awaiting word from the Fed about future policy moves and strategy. The committee meets tomorrow/Wednesday and is likely to pass on moving rates, but may entertain a hike perhaps if that scenario warrants it.

News over the weekend really put a sting into the equity futures. Stocks in Europe were down .7% as SPX futures sold off sharply, nearly 1.6% on heavy volume. Germany’s DAX fell 1.2%, down from all-time highs. Gold is modestly lower as is crude oil. Stocks are concerned over more tariff threats and a potential gamechanger in AI with DeepSeek. In a safety trade, German Bund yields are down 5bps, US 10 yr treasuries lower by 8bps as bond buyers come in heavy. Stocks in Asia were mixed, Japan down .9%, Hong Kong up .7% and Shanghai mostly flat.

Earnings will hit hard this week with four of the Mag 7 names reporting end of week. Those include Meta, Tesla, Microsoft and Apple. In addition, we’ll hear from Mastercard and Visa along with Intel, Chevron, ExxonMobil IBM, Dow and UPS. A slew of names that will no doubt move markets. Tonight is Nucor and Sanmina, tomorrow GM, Boeing, Lockheed Martin, RTX, Synchrony, JetBlue and a few others.

Stocks had another strong week even as the bulls tired out on Friday. This coming week could tell us a lot about how things go the rest of the year. There is the January barometer, as the saying goes, ‘As January proceeds so will the market the remainder of the year’. So far a positive showing but the markets are modestly overbought right now and any news response could be a selling opportunity.

Breadth was positive on Friday but not great, however markets did finish lower and breadth did not contribute to the late selling. Given the fact breadth levels have improved and are near highs on a cumulative volume basis (CVB), we could see a minor pullback in breadth and still not disturb the trend. New highs are back to beating new lows, oscillators are now in overbought territory, so a pullback would not be a surprise.

Volume has slowed down materially as the stock market pushes towards all-time highs. In the case of the SPX 500 that has already occurred, but a pullback in volume in the DIA and QQQ could be the first signs of a tired market. There are plenty of areas where we could see buyers step up if they are disinterested at the moment. We have seen good volume trends this month, especially on the up days. With only five sessions left in January and big earnings on tap it will be a test for the bulls.

Support levels continue to hold firm, the SPX 500 pushed higher off that 100 day moving average last month and continues to make higher highs, higher lows. The Industrials have shown the greatest amount of improvement though, with a very strong push through some resistance levels. This index is now within 1.5% of an all-time high, with some big earnings from the Dow coming out this week it might just make a run.

The Internals

What’s it mean?

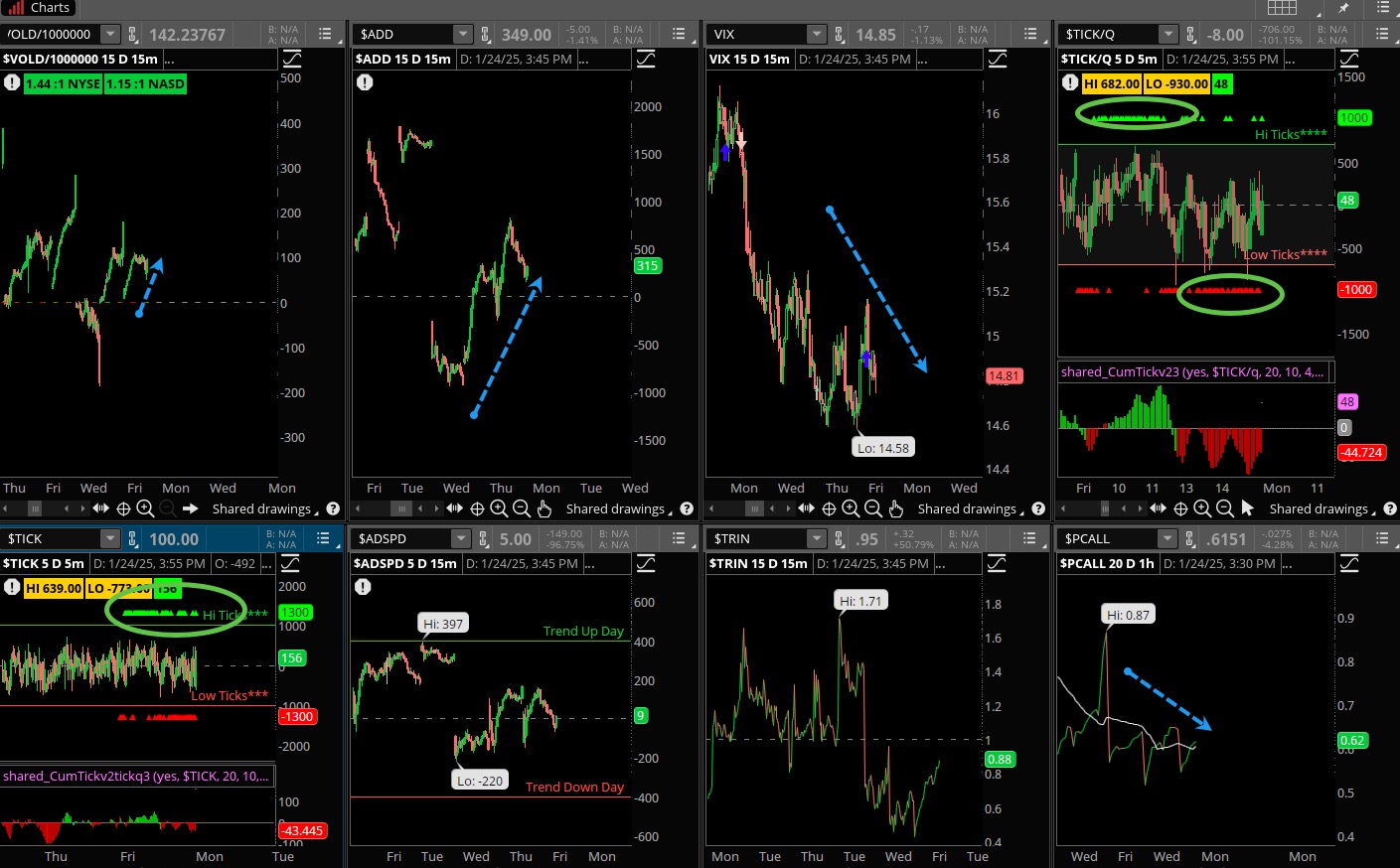

Nothing too exciting with the internals on Friday, other than the ticks showing us the bulls ran out of energy late in the day. That’s quite alright though, given the strong buying that occurred earlier in the week. The VIX slid one more time and is now firmly below the key 200 day moving average. VOLD finished higher but the ADD and ADSPD well off it’s highs of the session. Put/calls are still racing lower and looking towards a buy signal soon.

The Dynamite

Economic Data:

- Monday:New Home Sales

- Tuesday:Durable Goods, Home Price Index, Consumer Confidence

- Wednesday:Retail/Wholesale inventories, trade balance, FOMC rate decision, Powell press conference

- Thursday:GDP first look Q4, jobless claims, pending home sales

- Friday:Employment cost index, PCE, income/spending, chicago PMI

Earnings this week:

- Monday:SOFI, NUE, T, SANM

- Tuesday:BA, GM, RTX, SFY, JBLU, KMB, SYY, SBUX, SAP, LOGI, CH, FFIV, SYK

- Wednesday:ASML, TMUS, ADP, DHR, TEVA, GD, VFC, NDAQ, TSLA, META, IBM, MSFT, LRCX, NOW, CLS, WDC

- Thursday:UPS, MA, DOW, NOK, LUV, CAT, CMCSA, MBLY, AAPL, INTC,V, KLAC, TEAM, BKR, DECK

- Friday:XOM, CVX, ABBV, CL, PSX, CHTR

Fed Watch:

The first fed meeting of the year with four new voting members this week. Fed funds futures are predicting a pause this time around and for the next meeting, but the May session might be the one where a cut is announced. Regardless, it will be important to listen to the press conference closely for clues on future monetary policy. As always, the data matter most here.

Stocks to Watch

Interest Rates – The first fed meeting of the year is this week, also the first one after a change over in the Administration. Chair Powell is locked in and focused on how to manage monetary policy, and with recent strength in jobs, manufacturing and pricing pressures it seems the committee is ready for a rather long pause. We’ll know more after the press conference Wednesday.

Mag 7 Names – It’s a big week for the Mag 7 as four of these names will report during the latter portion of the week. Is Tesla overdone? Will Microsoft and Meta push their AI initiatives even further? We’ll know more this week, and of course Apple on Thursday evening.

GDP – The first look GDP for Q4 is out Thursday morning after the Fed decision but the committee has a good read on growth. The Atlanta fed GDPNow says we grew about 3% in the quarter, we’ll have to see how much was driven by inflation. Employment cost and PCE Friday will be important to watch, too.