The Fuse

Equity futures are mixed this morning with Nasdaq in the green but other indices slightly in the red. After Monday’s sharp move up we could expect to see a bit of easing by the buyers, especially with so much important data coming up later in the week.

Interest Rates are moving up, the 10 yr rising 1-2bps in early trading, the 2 yr yield is moving lower but the 30 year is threatening to break towards 5% again. High yield products (ETF) are ticking at all-time highs, and Fed Funds Futures remain steady.

Stocks rallied and piggy-backed on the US markets in overseas trading, The STOXX up by .3%, led higher by gains in France. Stocks in Asia were higher, the Nikkei in Japan up 1.3%, Hong Kong up a robust 1.4% and Shanghai ripped higher by 1.5%. Gold is moving slightly higher, better gains in silver while crude oil catches a bid. The dollar index fell .1%, yields are up as the German 10 yr bunds and US 10 yr treasury yields climbed 1bp.

Earnings start trickling in this week with HELE, STZ, WDFC amd a few other smaller names. Bigger earnings hit the following week.

A solid day for the bulls right out of the gate as the first full week of trading in January. The Santa Claus Rally turned into a bust for the third straight year, barely. The index (spx 500) needed to rally about 1% or so and was actually higher than that for a bit during the day before some late selling took the bulls down some. If they can gain some momentum here before the jobs report it bodes well for running to an all-time high this week. For it’s part, the Dow Industrials did have a positive SCR.

Better breadth again much like Friday, but the oscillators only pushed up modestly. Yet, they are positive and that means there is a chance to run up a bit more, seasonal trends are bullish as well. New highs trounced new lows yesterday, this indicator on a buy signal which could carry the markets for awhile. Internals were bullish (see below).

Solid day of turnover, but only accumulation days from the SPX 500 and Industrials. Nasdaq and small caps were up but turnover was not better than Friday. That is not really a problem though, we may see a bit more turnover later in the week, if breadth stays positive there is a chance to see the QQQ and IWM pull right up towards those old highs, which would be a great start to the new year. Look for more volume as we come towards Friday’s labor report.

As mentioned last week the test of the 20 or 50 ma was enough of a pullback to interest the dip buyers. It is this sort of ‘scary’ move down that creates some doubt, we usually see/feel that with a rise in the VIX but that did not happen, save for a quick run to 17% and right back down. The market is quite bullish here leading into an important earnings season, and the wall of worry is up.

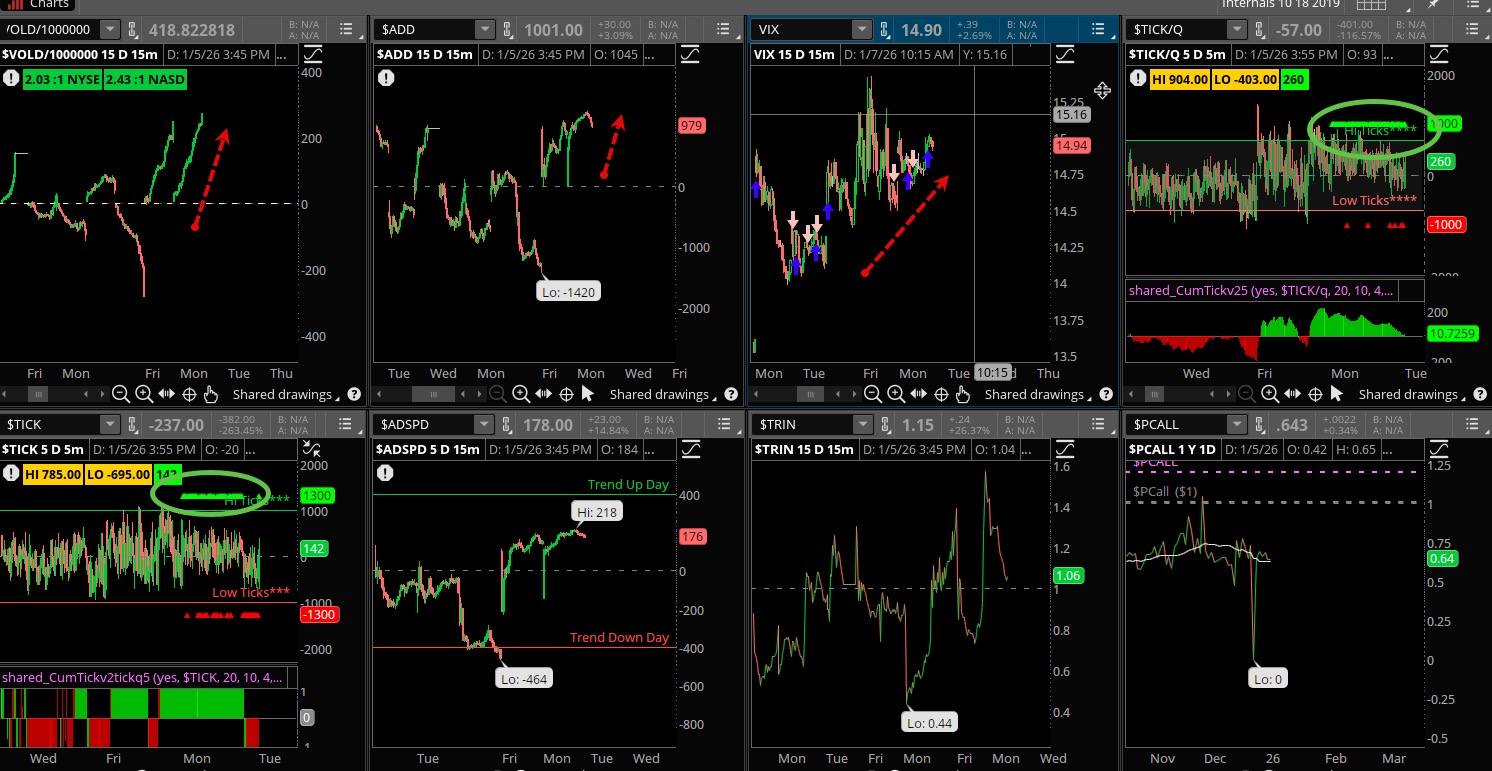

The Internals

What’s it mean?

Stellar day for the internals, look at that strong VOLD and ADD, finishing near highs of the day. Impressive were the ticks, notably the Nasdaq which had a slew of buy programs hitting all day long. VIX was up a bit, some may be concerned over that but it is not important here with volatility so low. The market was already complacent coming into today, and that means eventually a big whack will happen – just not yesterday. We could have seen a better ADSPD, that would improve with better small cap statistics.

The Dynamite

Economic Data:

- Tuesday:Services PMI, Richmond Fed Barkin

- Wednesday:ADP, ISM services, JOLTS, factory orders, Bowman speaks

- Thursday:Jobless claims, productivity, trade deficit, consumer credit

- Friday:NFP for December, hourly wages, consumer sentiment, Barkin speaks

Earnings this week:

- Tuesday:ARR, PENG

- Wednesday:APOG, MSC, ACI, STZ, JEF, AZZ, PSMT, SAR, RGP

- Thursday:SNX, HELE, RPM, SMPL, NTI, TLRY WDFC, AEHR, GBX

- Friday:

Fed Watch:

Fed speak is back, the countdown is on to a new Fed Chairman and with the change in the calendar a new set of Fed Presidents become very important. The first meeting of the year is at the end of the month, markets are not seeing a cut here in January but 50/50 for March.

Stocks to Watch

Technology – CES starts up this week in Las Vegas and is widely followed by analysts and technology experts. We often see deals of some sort happen during this week, as NVIDIA CEO will be a keynote speaker. Should be interesting.

Oil, Energy – With the US invading oil-rich Venezuela it stands to reason crude oil may rise in the short run. That is going to cause some big headaches for those short crude may be in for a rude awakening.

Magnficent 7 – This group has been the notable slacker in the markets of late but we could see them turn the tables as we head to a big earnings season.

[thrive_leads id=’60674′]