The Fuse

Equity futures are rallying this morning as we kick off the first trading day of July and the first session of the second half of 2024.

After a stellar first half for SPX 500 and Nasdaq, the other indices (Industrials, small caps) will try and catch up and push the other indices. July 1st (today) is often the best trading day of the year.

Interest Rates are up slightly as we start the new month. Fed futures are still portraying a couple of rate cuts, we may hear something different (or the same) when the meeting minutes are released on Wednesday afternoon.

Gold is rising a bit this am as is crude oil, above $82 a barrel. In Europe the Stoxx were higher by a robust 1.1%, the dollar fell against the euro but german 10 year bund yield climbed. In Asia stocks were higher, the Hong Kong market was closed but Shanghai rallied. We’ll be listening closely tomorrow to Chair Powell’s speech in Portugal.

Earnings are not in focus here this week, only Constellation Brands is the biggest name on the docket.

Not many events this week other than the start of a new month and quarter, and a short trading week. Thursday markets are closed, a another rare midweek holiday in observance of the July 4th holiday. The jobs report will be out following that holiday session and we’ll be watching it carefully to see if growth continues.

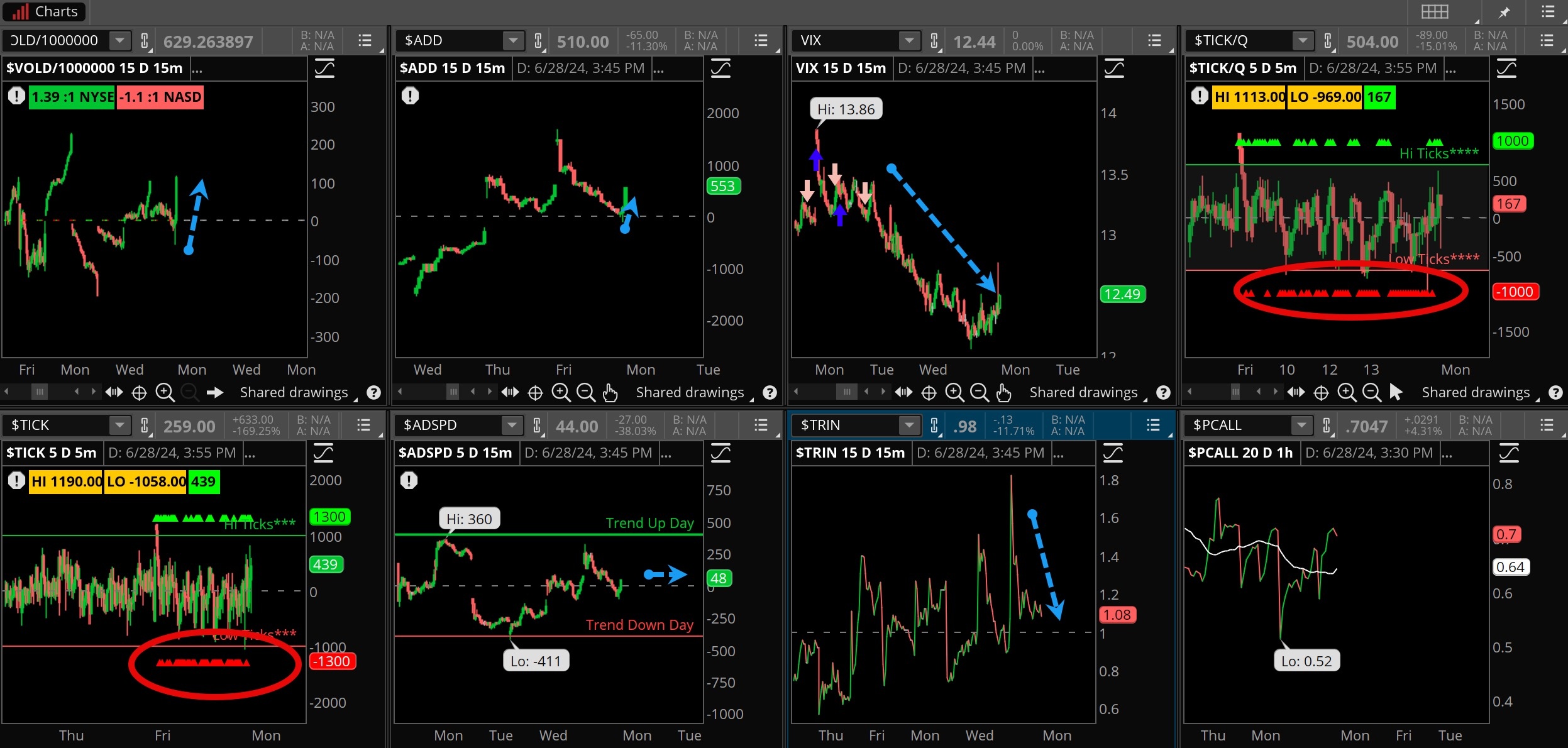

The breadth has been poor all week, save for Thursday which was not all that impressive. We did find the oscillator turned positive after Friday’s close but it was not convincing. Perhaps there is time for that! New highs on NYSE are starting to rise but the Nasdaq remains negative. If that starts to improve in the weeks ahead stocks may have some room to move higher.

Volume was pretty strong Friday as a big expiration day was upon us. The end of month and quarter is often a heavy volume session especially at the end of the trading day. This past week showed lethargic trade as we commence with the summer trading season. Often flat, low and dull which creates volatility and opportunity, if you’re looking carefully.

This past week tested the 5,450 level each day, so we are going to call that support for now. That is a pretty good level to hold, but if it fails then 5,400 is good support followed by 5,375 gap that needs to fill. The Nasdaq shows good support at 19,500 then 19,200 is the gap to fill.

The Internals

What’s it mean?

Not much oomph from the internals here. A positive PCE number Friday moved markets higher but then they flopped. Yet, the VOLD finished strong as did the ADD, but not much above zero. Ticks were pretty even though, VIX had a minor tick higher while put/call remains low. First of the month often sees strong money flows, Mondays have been pretty strong most of the year.

The Dynamite

Economic Data:

- Monday:SPX PMI, construction spending, ISM

- Tuesday:JOLTS, auto sales

- Wednesday:ADP, services PMI, factory orders, ISM services, fed meeting minutes

- Thursday:N/A

- Friday:employment report for June,

Earnings this week:

- Monday:

- Tuesday:MSC

- Wednesday:STZ, BB

- Thursday:N/A

- Friday:N/A

Fed Watch:

This past week we heard from several Fed speakers who seem to like the trend inflation is taking. That would be lower of course, the PCE from May showed a flat month/month and lower annual number, not to the 2% target but getting there. It is increasingly like the Fed is going to cut rates at some point in 2024, more likely in September if more data shows the trend continuing. All eyes/ears on Chair Powell on Tuesday as he speaks in Portugal, later in the week NY Fed president Williams is out twice. We’ll also have the Fed meeting minutes released Wednesday during the day from the June meeting.

Stocks to Watch

Volatility – The VIX remains extremely low here and could even bust lower with a holiday coming up. We often see volatility recent and sell off before a holiday session. The VIX is telling us buyers and sellers seem satisfied at this level.

Technology – After a stellar first half of the year can the momentum continue? Nasdaq had a strong 17% gain following an amazing 2023.

The uptrend remains in tact as sellers are not interested in letting go just yet, certainly not while the Fed looks ready to pivot towards an easier policy.

Name – event, level, your expectation