The Fuse

What are futures doing?

Modest gains this morning in equity futures, Nasdaq getting the bulk of the gains but the SPX 500 is not far behind. This index is less than 1% away from all-time highs and the bulls would like to make a run at it. PPI this morning could do the trick.

News

STOXX in Europe were slightly lower, off .1% but with bigger drops in France and Germany. FTSE was down more, off .6% while the dollar index was flat. Crude is up about 1%, gold and silver modestly lower. Yields are rising in fixed income, Bunds up 2bps while 10 yr US treasury yields up 1bp. Japan rose up again, Nikkei up 1.5% while Hong Kong another strong session, up 1.4%. Shanghai fell .3% on modest trade.

Volatility

As the rhetoric from the Iran War softened as it usually does so does the VIX, which rose up smartly Monday but backed away enough to give the bulls some room to buy stuff. If there is some positive news here it will be reflected in the volatility index.

If you are an existing Market Blast or Trader’s Pass member, log in here:

Interest Rates

Rates are up slightly as fixed income buyers become absent. I think yield moves hinge on the treasury debt auctions this week.

Earnings

Tremendous earnings from AEHR last night, stunning gains today. Also ASML beat and raised guidance, so did Blackrock. We’ll hear from Morgan Stanley this morning. Johnson & Johnson beat and raised guidance too. MTB had a strong quarter, Elevance offered weak guidance.

Events

Markets were grinding higher all day Tuesday trying to negate the down move from Monday. They only cut the losses in half (SPX 500), but new highs are still within striking distance. The action has been rather poor, and I suspect many thought the CPI would bring the markets lower, but it did not. More inflation news today.

Breadth

A win for breadth as the a/d line finished positive, much like it did on Friday’s nice rally. However, if the buyers don’t step up we could see a replay of Monday, which was disastrous for the bulls. Oscillators are back in the green for the NYSE, new highs with a slight advantage over new lows.

Volume

A flip from Monday, somewhat. Distribution day – barely on the Industrials but lower turnover on the other indices though they were higher. I expected to see a bit more volume flowing in after the CPI hit but that did not happen, market players are pretty complacent here with the VIX so low, the worry is that bullish traders are filling the boat, and if there is nobody left to buy there are only sellers left.

Support Levels

Monday was a good test of support, and even overnight some selling hit the indices hard, but we can always rely on earnings to pull the markets through the muck. We’ll call 7.500 on the spx 500 as good support, the Nasdaq is trying to push through 30K on the futures and is nearly there, the small caps are struggling but if rates come down that will change things.

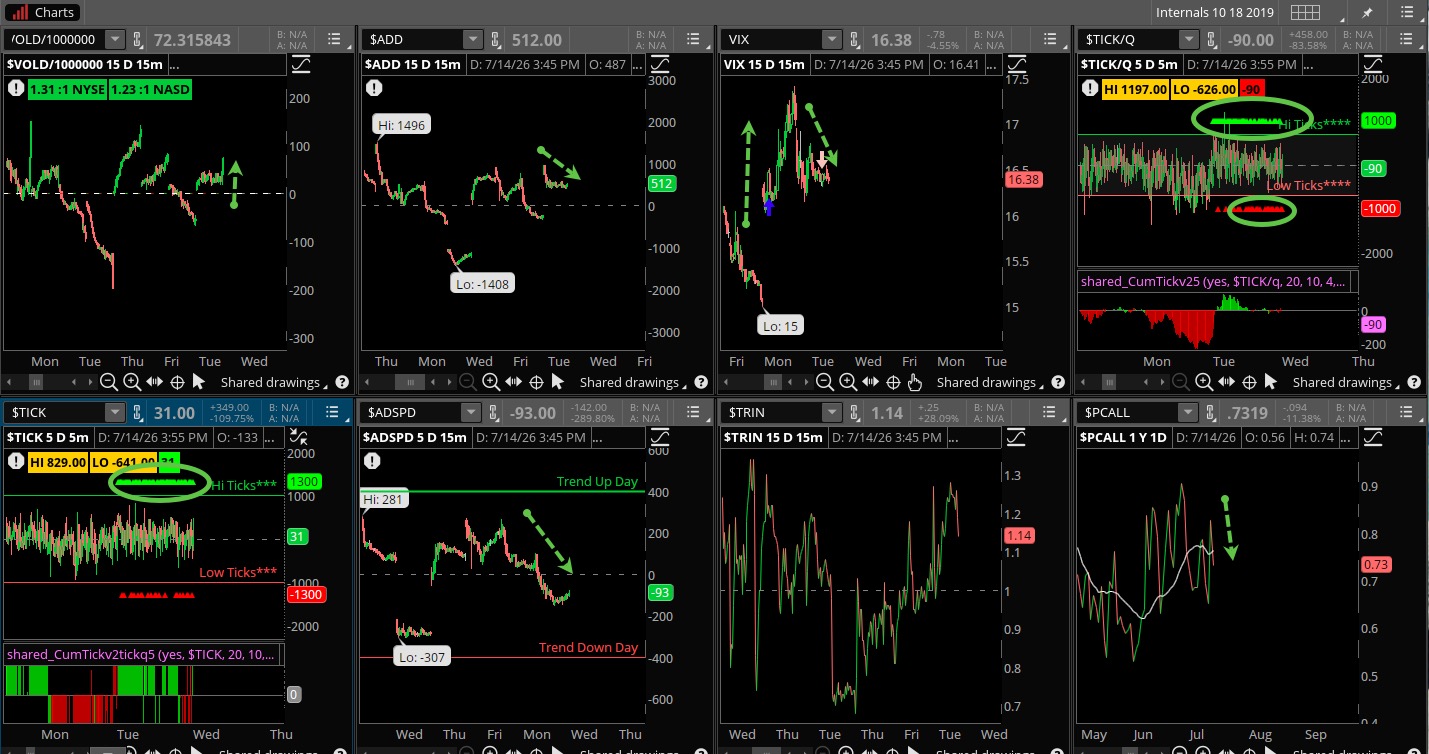

The Internals

What’s it mean?

Back to mediocre internals. The VOLD finished nicely, but the ADSPD and ADD were diverging. Put/calls started to decline again after a pop on Monday, VIX fell nicely after a big rise on Monday. TICKS were strong most of the day but there were some sell programs, as indicated by the concentrated red bars. We’ll see how it goes here today if there is followthrough.

The Dynamite

Economic Data:

- Wednesday:empire state, PPI, pce, Fed Chair Warsh testimony, more fedspeak

- Thursday:Retail sales, philly fed, housing market index, pending home sales, jobless claims, more fed speak

- Friday:Housing starts, import prices, industrial production, cap utilization, michigan sentiment.

Earnings this week:

- Wednesday:ASML, PGR, BLK, MS, CAG, JNJ, ELV, PNC, MTB, CTAS, UAL, JBHT, KARO

- Thursday:UNH, TSM, USB, GE, ABT, STT, CFG, NFLX, ISRG, AA, CNS, WISE

- Friday:RF, TFC, FITB, TRV, SFFI, SKIFY

Fed Watch:

Pay attention this week to Chair Warsh as he talks to Congress about monetary policy. Listen carefully for clues about where policy may be heading, though he has been evasive for weeks. He will face some tough questions this time around.

Stocks to Watch

Chip stocks – with SK Hynix now trading in the US markets there is another competitor for dollars out there, and that might take from Micron, Sandisk and others. This group is key for the markets to retain upward mobility.

Banks – The big banks will report earnings early in the week and optimism is high, with most names at/near all time highs. I suspect strong numbers but any whiff of caution will knock these stocks down sharply.

Volatility – We will again watch volatility closely as the VIX is down to a very low level, near 15%. That is a bit too cozy for market players so expect some giveback, though with earnings up this week not too much.

[/MM_Access_Decision]