The Fuse

Equity futures are mixed after a strong push higher early in the overnight session but has backed away. The Industrials and small caps seem ready to keep their rally going, which could last a few more days. With support for the market from other groups that means we’ll have expanding breadth, much like we saw yesterday.

Interest Rates are backing away again after rising up a bit Tuesday. The trend is rates is now lower with the 10 yr yield firmly below the 200 day moving average. High yields spreads are tight still, new record highs for JNK and HYG, TIP is rising which tells us the market is worrying about inflation still, fed futures don’t care as they see at least 3 1/2 cuts in 2025, more than than Fed expectations.

Stocks overseas were modestly higher, the STOXX in Europe gained .2% led by France and Germany. The FTSE gained the same, US dollar index was up also .2%. Gold is slightly higher as is silver, crude oil is up 1.5% on good volume. German 10 yr bund yields and 10 yr US treasury yields were higher by 3 bps, and in Asia stocks were mixed with Japan down .6%, Hong Kong up .6% and Shanghai barely changed.

Earnings are sparse this week as we turn the page on the quarter and get prepared for the next earnings season.

The start of July was somewhat bifurcated, with good strength in the industrials and small caps but the tech stocks really taking it on the chin. That’s not a surprise when you think about it. A strong month of June coming after an equally strong month of May and then suddenly some profit-taking just before earnings season gets underway. A good but not great start to the new month, perhaps some new money flows will get put to work before the long holiday weekend.

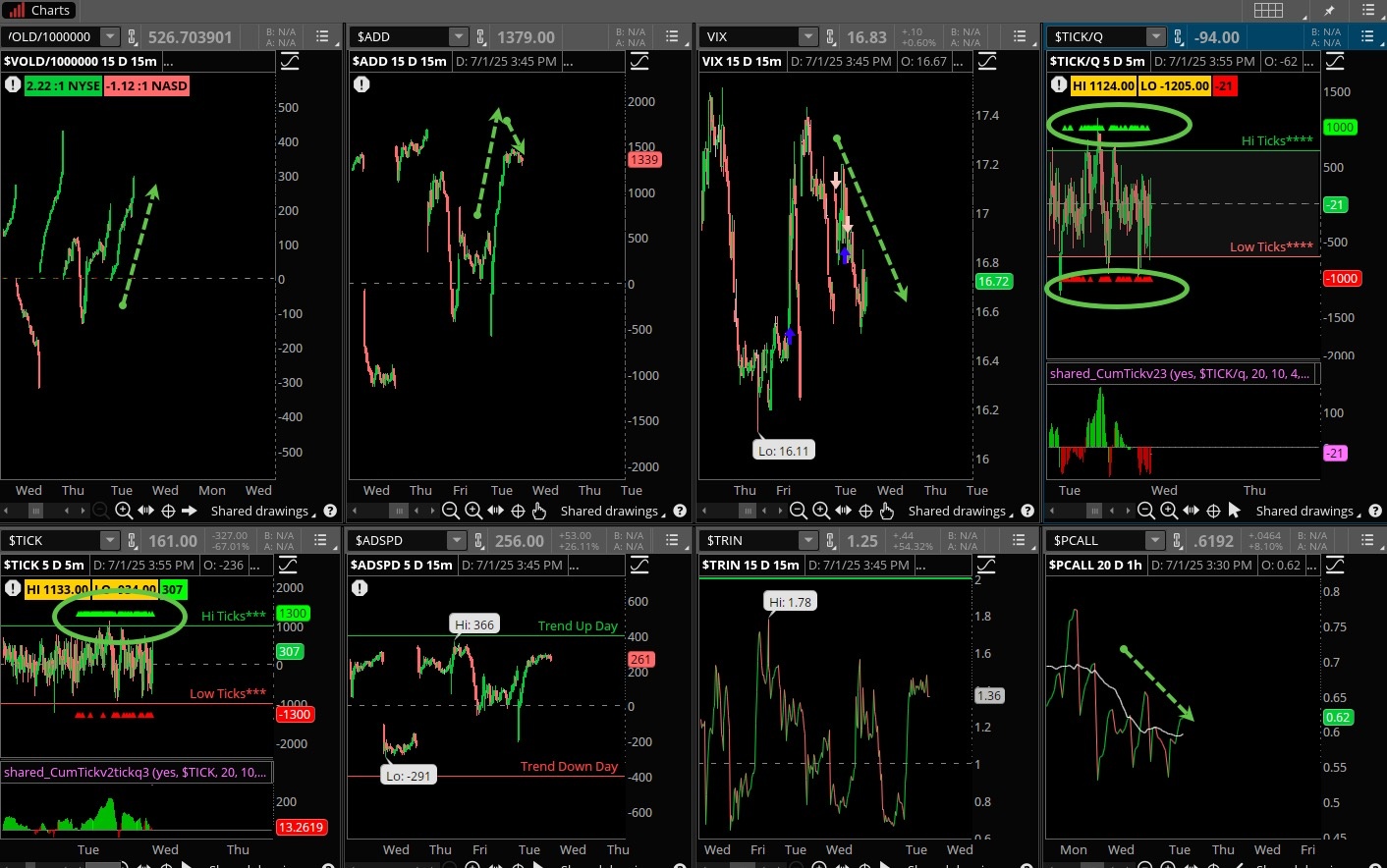

Really solid breadth, we can thank the small caps and widespread breadth for that. A clear win for the bulls when it comes to breadth, nearly 3-1 positive as the oscillators continued to cruise higher but are not overbought yet. That may happen by the end of the week if the momentum continues to be strong. New highs continue to expand as this indicator is on a buy signal.

Strong turnover on the positive indices like the IWM and DIA is bullish while weaker turnover on the bearish indices like the SPY and QQQ is also rather bullish. We may see volume really fade hard as we wind up the short trading week but pick up later in the month. Summer is notorious for poor volume sessions, which can linger beyond Labor Day.

Short term support areas were tested yesterday but the bears had little conviction to make it count. Clearly the bearish traders are getting scared about a squeeze, which is now a psychological advantage for the bulls. Still, there is support much lower at 6,030 and 5,920 what Nasdaq has good support at 22K.

The Internals

What’s it mean?

Some very strong internals yesterday pushed the indices higher (industrials and small caps). Having the IWM lead the way meant we had strong breadth, and we see that with solid VOLD adn ADSPD. The ADD was positive but well off the highs of the session. Put/calls were slanting lower again, ticks came in strong on the NYSE but about even on the Nasdaq. VIX fell again and remains quite low..

The Dynamite

Economic Data:

- Wednesday:ADP employment

- Thursday: NFP report for June, jobless claims, services PMI, factory orders, ISM services

- Friday:N/A

Earnings this week:

- Wednesday:UNF, FC, ZENV

- Thursday:N/A

- Friday:N/A

Fed Watch:

Not much on the Fed’s calendar for speakers this week but I’m sure they will be watching the data closely. Recent comments from Governors has them leaning towards a more loosening policy, but according to Chair Powell more data needs to be analyzed. Last week on Capital Hill he did acknowledge inflation is moving in the right direction (down) but needs to continue the process.

Stocks to Watch

NVIDIA – The big semiconductor stock closed at an all-time high last week and helped to bring up others in the group. If this momentum continues then the Nasdaq will drive up other names, too.

Coinbase – This stock really pushed higher this past week and was the best performer in the SPX 500. COIN has strong ties to crypto and bitcoin, which is trying to break out from a recent range.

Volatility – Having fallen sharply over the last few weeks the VIX finds itself at levels last seen in February, just before a hailstorm of volatility hit the markets. In front of a holiday however we often see VIX fall or at least stay down, that is likely to be the case this week.