The Fuse

Equity futures are rallying this morning, trying to followthrough on Friday’s sharp up move. With so much volatility in the markets right now we are neither overbought or oversold any longer, but that could change with a strong move in either direction. End of month is nigh and that might spur some late buying to keep July in the positive.

Interest Rates are down some this morning as bonds are catching a bid. The 10 year remains bracketed in a range of 4.15% and 4.5%, but the 4.2% level being rather critical. A Fed meeting this week might clear things up a bit, and if rates slide lower it will be beneficial to small cap stocks. The market is not expecting the Fed to move on rates this week.

While US equity futures are rallying we saw robust gains in Europe, the Stoxx higher by 1.2%. The US dollar index is flat, crude oil is down about .5% while gold is higher by .35%. German 10 yr bund yield is down 2 bps, stocks in Asia were mixed as the Japan Nikkei roared higher by 2.1%, Hong Kong also rallied strong but Shanghai was flat.

Earnings from McDonalds this morning were a disappointment but the stock is rallying a bit, perhaps the bad news is priced in already. We’ll hear later from F5 Networks, Sprouts Family Markets, and Lattice, tomorrow am Paypal, Sofi, Pfizer, P&G and Jetblue. It’s a huge week for earnings.

The stock market may be responding to the changes in election polls which is giving rise to volatility. But actually what is happening the market is more in tune with Fed policy and a potentially monumental moment. It has been a year since the Fed last moved rates, a high in July 2023 but now that very tight policy is about to be challenged. That meeting this week could be the pivot or turning point the stock and bond markets are looking for.

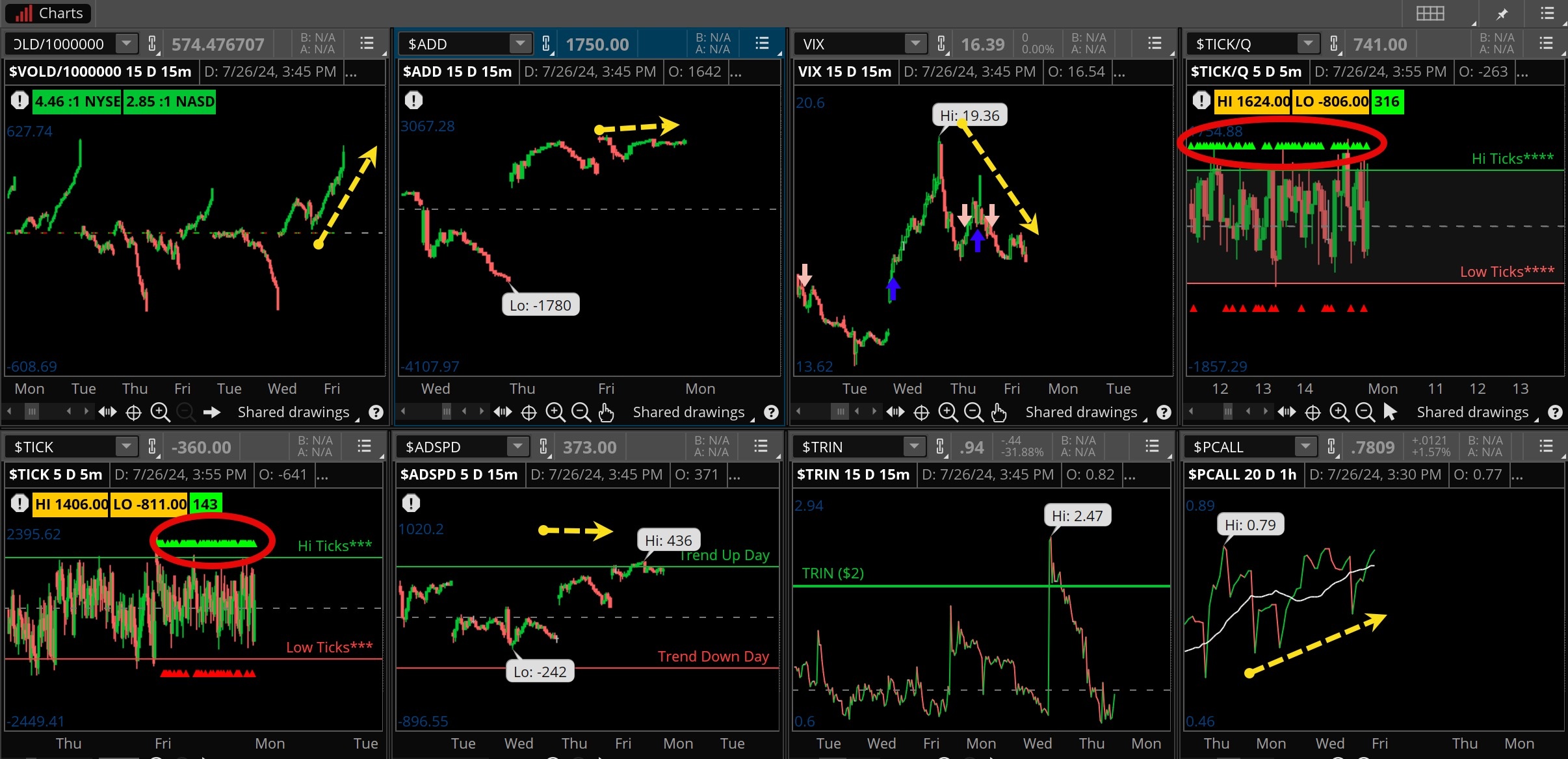

Breadth was outstanding Friday with leadership again from the small caps. The IWM is now within spitting distance of an all-time high, which could easily be achieved this coming week. That would likely bring more strong breadth. Oscillators are back up and rising while new highs are once again trouncing new lows.

This indicator is on a buy signal again.

Volume expanded a bit in the morning and afternoon signaling work being done by big institutions. That sort of activity lends good support to price levels and as long as the turnover is robust any lower levels may be difficult to penetrate. High volume on the up days is immensely bullish.

Support for the SPX 500 clearly at the 50 ma, that level may be holding Thursday’s low. The Nasdaq has support at the 100 ma, that average is still not out of the woods. A few up sessions though might go a long way. The Industrials, which had been beaten up badly has good support at 39,990.

The Internals

What’s it mean?

The bulls conquered the day! It was a very strong bullish day for the internals, nearly all at their peaks of the day on the close. The VOLD led the charge, a robust move as did the ADD. The ADSPD (lower) led a trend up day, vix declined as it should and the ticks are very green all session long, which bodes well for today’s trade.

The Dynamite

Economic Data:

- Monday:N/A

- Tuesday:Home prices, consumer confidence, JOLTS

- Wednesday:ADP employment, employment cost index, PMI, pending home sales, FOMC interest trade decision, Powell press conference

- Thursday:Jobless claims, US productivity, US PMI, ISM manufacturing, construction spending

- Friday:Labor report, factory workers

Earnings this week:

- Monday:MCD, ON, FFIV, ROMBS, SFM, WELL

- Tuesday:GLW, LGIH, PYPL, PG, QSR, SYY,AMD, CZR, FSLR, LC, MSFT, QRVO, SWKS, SBUX

- Wednesday:ADP, BA, CNHI, DD, KHC, MAR MA, RDWR, TKR, AMZN, CAKE, EBAY LRCX, META, QCOM

- Thursday:ADT, COP, CMI, ETN, HSY K, LH, SHAK, UTZ, AAPL, BZH, NET, DASH, ROKU, SNAP, OLED

- Friday:CVX, XOM, CHD, LIN, PIPR

Fed Watch:

The day has arrived, could this be the change many have been waiting for? The Fed kicks off their next two-day meeting on Tuesday and is likely to leave policy on hold one more time. The FOMC has not moved rates in a year but that may be changing with the September meeting, which fed futures are pricing in a 100% chance of a cut. We’ll be listening to the language and if the committee sees the trend in lower inflation continuing, the strength in the economy and the risk of imbalances in the system.

Stocks to Watch

Bonds and Rates – With the Fed meeting this week there is likely to be a sea change in bond yields, which could move sharply lower if the statement is perceived as dovish. No expectations for a rate cut this time around though, but certainly in September. We’ll be watching the 4.2% level on the 10 year.

Apple – the big device company reports earnings this week and while the stock is off all – time highs from a few weeks ago, there is the promise of an AI phone coming which could be a massive refresh of iPhones worldwide. This may not be a great quarter but it’s all about the guidance.

Microsoft – The stock was hit hard last week following the CrowdStrike debacle. Can they get their mojo back, and will they continue to see expansion in AI, spending and data? These areas lifted Microsoft last quarter and will be watched carefully. Looking for a high single digit gain in earnings this quarter, the stock is off 10% from recent highs.