The Fuse

What are futures doing?

After a huge blowup yesterday stock futures are poised to gain back some lost ground, but there is more work to do – likely next week. The deal with Iran appears to have been signed and markets are looking ahead. Kevin Warsh had his first press conference, the markets had a rather odd response.

News

Markets in Europe were weak following the late selloff in US indices. The STOXX down about .2% but Germany was higher by .2%, FTSE fell .8% as crude oil continues its march lower. Gold and silver are paring recent gains. The US dollar index fell .1%, US 10 yr treasury yields fell a whopping 6bps, German bunds were flat. Japan ripped higher again, up 1.6% but China’s markets were lower, Hong Kong off 2.2% and Shanghai down .4%.

Volatility

With the deal signed with Iran and in front of a holiday weekend the VIX is in decline, heading back towards the mid teens. Yesterday’s burst in volatility was not unexpected as too many were leaning to hard on the bull side of the boat. Wednesday brought both sides more into balance.

If you are an existing Market Blast or Trader’s Pass member, log in here:

Interest Rates

Big move down in yield on the long end of the curve this morning with 5’s, 10’s and 30’s all dropping sharply. No doubt this is in response the hawkish tone by new Fed Chair Kevin Warsh, the short side of the curve is not well bid, seeing a hike or two later in the year. High yield remains very attractive still, the 2/10 spread continues to flatten which may not be the best approach for equity markets.

Earnings

Both Accenture and Kroger with a miss this morning on earnings have those two names backing away and retreating sharply.

Events

One thing we knew that would be different about Kevin Warsh was his approach to the Fed, the message transmission and his attitude towards current Fed style. His unique view is counter to many of his predecessors, and if you’re a market historian then you know things are going to shaken if not stirred a bit. Markets realized this was going to be a challenge, volatility kicked up and took the markets on a ride. Calm water ahead though, I believe.

Breadth

Breadth made another big turn lower as the decliners had a decisive advantage, nearly 3-1. However, we’ll give the benefit of the doubt to the breadth buy signal for now, still on since earlier in the week. Yet, if we have another huge down session here (unlikely into a 3 day holiday) then we could see a mess next week. Volatility rose up and could be sold down in front of the long weekend as per usual.

Volume

Heavy turnover yesterday, hence a distribution day as volume exceeded Tuesday’s levels. Given the fact much of the volume came in the last 2 hours was of no consequence, markets tried to shake of the Fed Chair’s message of change but sellers had the advantage. Look for some very heavy turnover numbers today.

Support Levels

Markets made an adjustment yesterday, probably with some volatile action due to the big expiration today and long weekend to come. Short term support levels were tested and may have succeeded, we’ll have to see in the coming days. Prior to the Fed statement/press conference some groups were actually up strong, and new highs were achieved in those sectors like banks and chip equipment. All for naught.

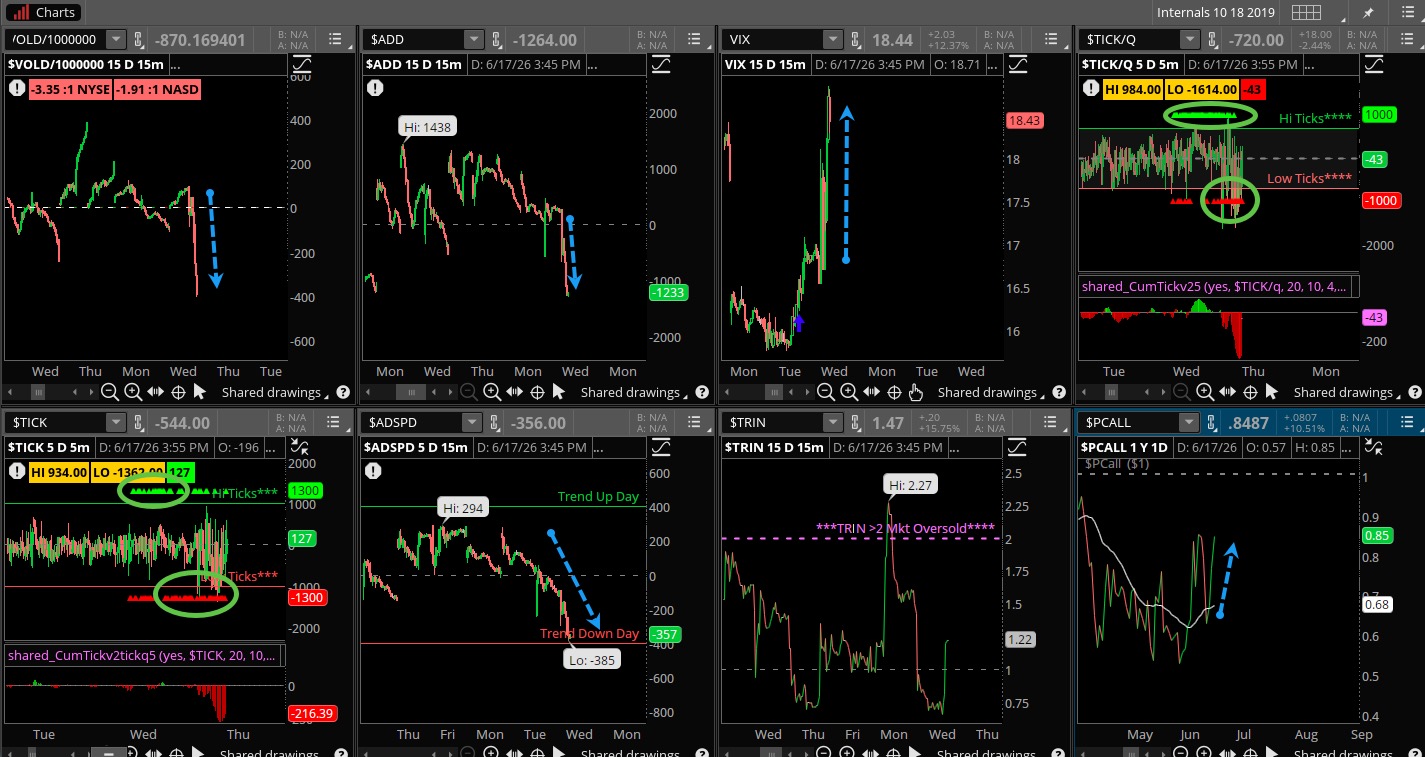

The Internals

What’s it mean?

Just nasty on the internals, the VOLD hit with some powerful down moves as did the ADD, while the ADSPD had a trend down day, first time in awhile. We can chalk up this poor action to the misdirection early in the day and then the expiration later on Thursday, but suffice to say the internals were not supportive. VIX spiked but still finished under 20%, Ticks had a slew of sell programs late in the day that cused the big turn, and put/calls were rising late in the day. Some order restored would be a good start to the long weekend.

The Dynamite

Economic Data:

- Thursday:jobless claims, Philly Fed, leading index

- Friday:Holiday

Earnings this week:

- Thursday:KR, ACN

- Friday:N/A

Fed Watch:

The week we have all been waiting for! This is the first meeting chaired by Kevin Warsh, a seasoned veteran of the Federal Reserve Board who is providing some new leadership following the end of Jay Powell’s term. I expect to see/hear much of the same from the new Chairman, the committee will have a new set of economic projections, no move is likely in rates in this week’s policy decision.

Stocks to Watch

SpaceX – By all accounts a successful IPO last week, but now the hard part begins. Options start trading on Tuesday, volatility is going to start being priced in as sellers are lurking. It’s going to be an interesting week for this new issue.

Interest Rates – The facts are clear and understood, inflation is starting to rise and may soon cause more price increases to occur. With the Fed meeting this week I suspect they will show some concern, else we could see bonds selling off in a big way.

Iran War – Will there finally be an agreement? It has been bountied around for weeks now but nothing in writing. Thursday seemed as if the two sides were close, markets rallied sharply. This is a short week and maybe an agreement is coming by the July 4th holiday. Wouldn’t that be ironic.

[/MM_Access_Decision]