The Fuse

Equity futures are backing away this morning after a nice overnight bid was replaced by selling. That may change of course during real time hours, but money flows out of stocks has been an issue of late. As we stumble into the last few days of the month and quarter there will be plenty of jagged moves.

Interest Rates are rising slightly this morning as bonds overseas started to lead the charge lower. We still see the trend in long term rates as lower, the 5, 10 and 30 yr yields having entered into downtrends. However, recent low yields (4.2% on the 10 yr for instance) are the lower bound, so a slight bounce is evident.

Crude oil is up modestly in front of supply data, gold is down a bit as is silver. In Europe the Stoxx gained .4%, the dollar index climbed while stocks in Asia mixed, Japan up 1.3%, Shanghai .8% and Hong Kong was flat. Rivian got a big investment from Volkswagen, Apple with another big upgrade and NVIDIA is higher in the pre-market.

Earnings from FedEx last night were strong but so was guidance. The stock is up sharply this morning and will likely push the Dow Transports higher on the day. Paychex had a nice beat and guided slightly higher, General Mills is down sharply after missing earnings/revenue and offering soft guidance. Tonight a big report from Micron, also Jefferies will report.

Better action on Tuesday as the tech sector woke up from a three day slumber. This group was led by, who else? NVIDIA, which rallied 4% on pretty good volume. But other big tech names like Google, Intuitive Surgical, Microsoft and Meta helped push the markets up, though breadth was soundly negative.

The bifurcation continues with big caps separating from the Industrials and small caps. Breadth was atrocious for a day like this, but when the Russell 2K cannot move ahead then we are left to settle for mediocre internals (see below). Oscillators turned lower though we won’t say if this is negative yet until the end of the week.

The industrials were sharply lower and tacked on higher volume, hence a distribution day. Yesterday’s largest rally in the face of other weaker markets seemed suspect at the time, and with no followthrough we just continue to see this index muddling through. Until there is a breakout on high volume we are stuck in a range.

Is the support going to be tested even lower? It’s possible, but the bulls are just not letting go. However, some sectors like semis have shown weakness recently, same as housing and some retail. We still think a 2-5% correction is coming and would be welcomed by long term investors to reset the markets. As it is, there is quite a bit of giddiness and froth, VIX still very low.

The Internals

What’s it mean?

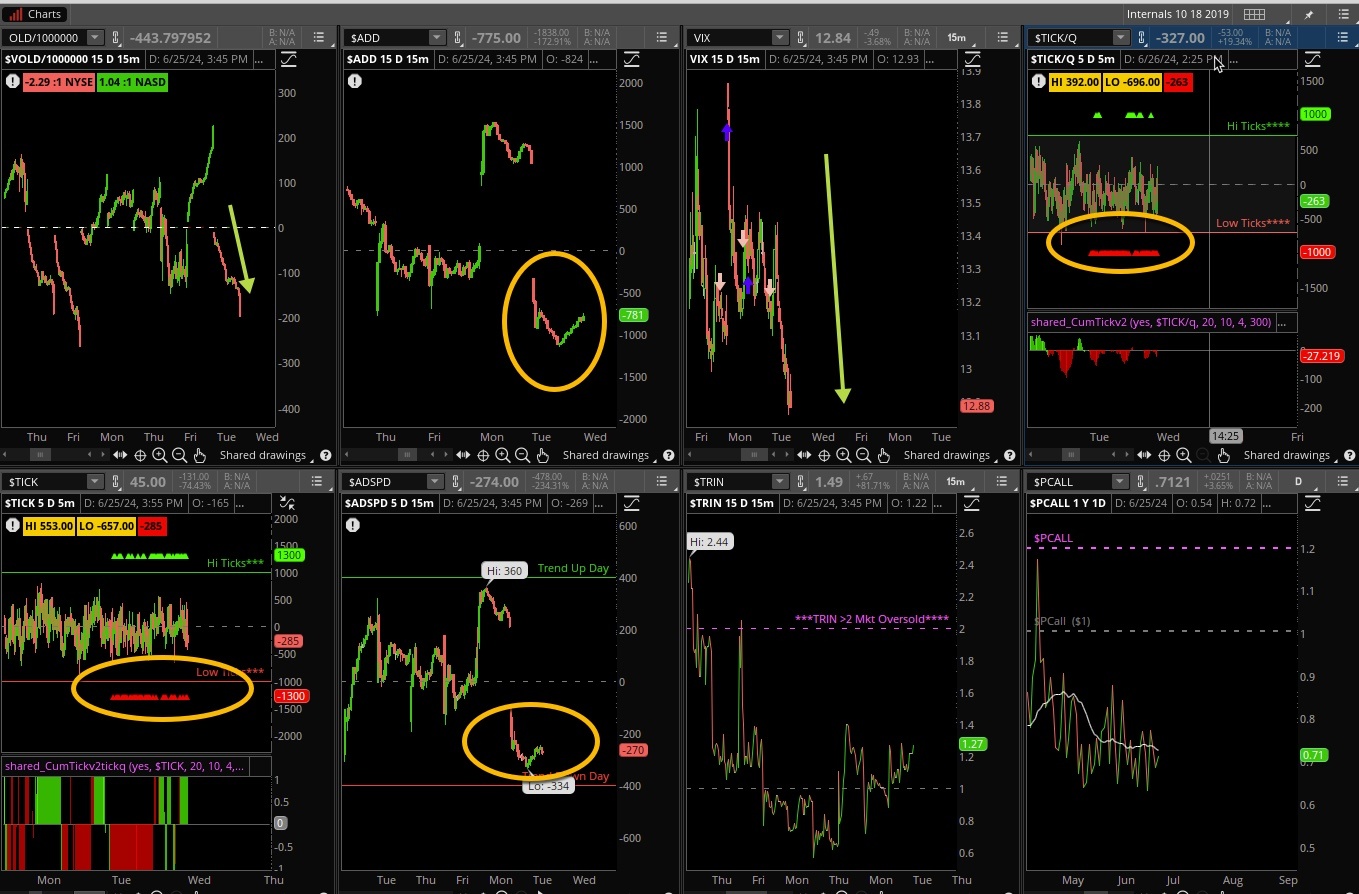

Nothing good to say about the internals. Atrocious is the best way to describe the result. Just look at how miserable the VOLD ended, the ADD and ADSPD just floored. Ticks were mostly red. But, the VIX was weak and stayed down, hence not much need for protection as the pricing seems to be fair for volatility. Markets were mostly higher, which is clearly a headscratcher with these internals. Will there be better internals this week? We hope so.

The Dynamite

Economic Data:

- Tuesday:Chicago Fed National, consumer confidence, Housing price index

- Wednesday:New home sales, crude inventories

- Thursday:jobless claims, adv retail/wholesale inventories, durable goods, GDP (third estimate), pending home sales

- Friday:May income/spending, PCE, Michigan sentiment

Earnings this week:

- Tuesday:CCL, FDX

- Wednesday:PAYX, GS, MU, BB, LEVI, JEF

- Thursday:MKC, LIN, NKE, AYI, WBA

- Friday:

Fed Watch:

Fed speak was out in force last week as the Fed governors pretty much stuck to their statement the prior week. It’ll be a month before the next meeting so plenty of data to divulge. We’ll have two speakers this Monday, three on Tuesday and another on Friday. Most likely the recent data will not yet convince the committee to cut, though markets are basically predicting a cut in September then one in December.

Stocks to Watch

Housing – Some pretty lousy home data last week and a bunch more coming this week. Could this be the tree that falls to start an economic slowdown? It could be, but if rates decline even more look for another cycle up to begin.

Sentiment – Consumer sentiment and Michigan sentiment will be released this week, and most consumers have been downright negative on the economy. Perhaps it is just a hunch or maybe just their situation, but if sentiment continues to deteriorate that may have consequences for equity and other markets.

Quarter – It has been a strong quarter for stocks even with a poor April. I’m sure the bulls would like to see a strong finish into Friday’s close. SPX 500 is up nearly 17% for 2024 so far, an amazing accomplishment following a strong 2023.