The Fuse

Futures are modestly lower before open as we await word from the BLS about the latest reading on inflation. The CPI will be announced at 830am est today and is expected to be hotter than last month. The Cleveland Nowcast is looking for a 7% month/month annualized figure.

Interest Rates are pulling back this morning as bond prices are on the rise. However, the inflation data today/tomorrow will skew rates.

Debt ceiling continues to be the topic of conversation each day. The drama was taken to another level yesterday with the Speaker talking tough.

In the end, a deal will get done (who knows when) but the uncertainty rises up before. Germany’s CPI came in at 7.2% y/y but that was in line with estimates.

Last night horrendous earnings from Twilio and Airbnb with their guidance below consensus. However, Upstart managed to skip by and is popping in the pre-market, Wynn delivered strong numbers. Today a big miss by Roblox has this stock down 17%. Later today we’ll hear from Disney, The Trade Desk, Unity, Robinhood and Beyond Meat.

Some may call this boring action, but we really see this as a consolidation before some big news breaks, and that’ll be later today/tomorrow with inflation reports.

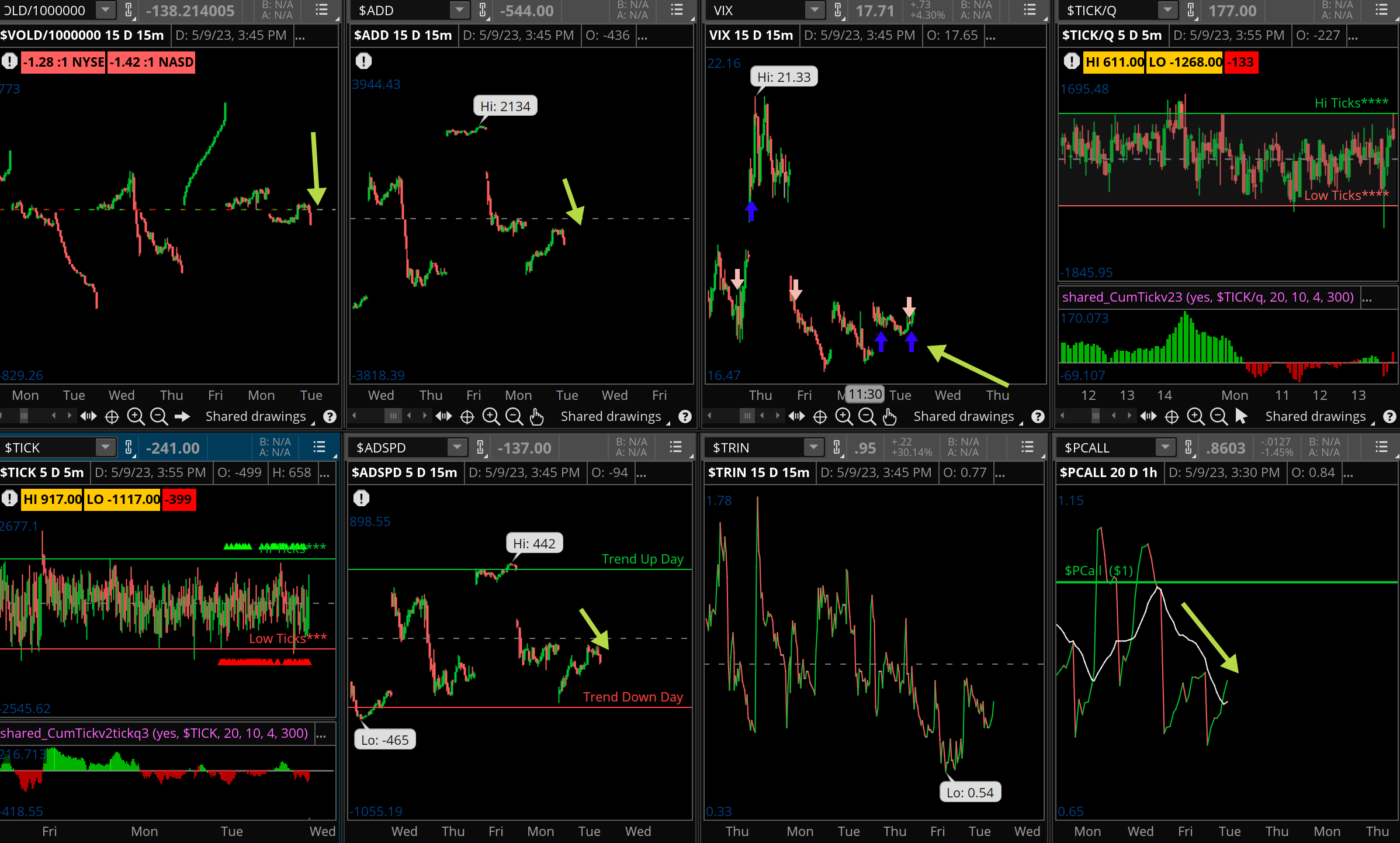

Breadth on Tuesday was again poor, stocks were rather unstable all session long as players started hunting for stops up and down the market.

We never really saw the markets get any traction to the upside, perhaps waiting for something to happen first.

Once again volume was poor to the upside as the bias was bearish all session long. We’ll have to see if some earnings news today stokes some buyers to step up, or if we’ll have a leg down towards 4100 or lower.

Another very tight trading range and the SPX 500 moved within a 15 point range Tuesday. That is not too common but can be expected when the VIX remains low and realized volatility is also very low.

The Internals

What’s it mean?

Much like Monday there was nothing much to glean from the internals. A late day selloff however did turn the VOLD, ADD and ADSPD lower, but that was likely due to some last minute positioning before big new hits in the morning. Put/calls are relatively low here, while the VIX is equally low and may try another run at 20%. If so, markets will feel some heat.

The Dynamite

Economic Data:

- Wednesday: Mortgage Apps, CPI, Crude oil inventories

- Thursday: PPI, jobless claims

- Friday: Michigan sentiment, import/export prices

Earnings this week:

- Wednesday: RBLX, WEN, ALRM, CAKE HOOD, TTD, DIS

- Thursday: CYBR, DDS, TPR, UTZ,, INDI, SANM

- Friday: SPB

Fed Watch:

After last week’s meeting and a quarter point rate hike, we will see if the Fed speakers tone it down. Two Fed speakers today and two more later in the week. The key they will be looking for is a reduction in PPI. Cleveland nowcasting has CPI climbing to 7.2% on their estimate for April. The wages number last week was much too hot, and while Chair Powell seemed sanguine on more rate hikes, he was adamant about no rate cuts, too!

Issues/Stocks to Watch this week

Volatility – The VIX was smashed down again Friday, far too low for comfort. We’ll see if it rises this coming week.

OPEC meeting – The last time they met it was a cut in production. We’ll see if that happens again, which might be a surprise.

Banks and Congress – Lawmakers say they are monitoring the situation with regional banks and their problems. Let’s hope they don’t step in and try to fix markets as they did once before – that was a disaster.