The Fuse

Futures are slightly down today as markets await the PPI release. The ES futures remain trapped below 4,200 where it seems to be encountering stiff resistance.

Interest Rates are falling this morning as worry about the debt ceiling issue continues to weigh on investors’ minds. The uncertainty about when /how this will resolve has investors reaching for safety, hence treasury bonds.

CPI came in mostly as expected, the y/y number actually lower at 4.9%. We’ll see about the PPI number today, which was negative in March.

A miss by Disney last night has put the Dow Industrials on the defensive. The Trade Desk posted strong earnings and guidance, Tapestry posted strong earnings and boosted their outlook for 2023.

Some may call this boring action, but we really see this as a consolidation before some big news breaks, and that’ll be later today/tomorrow with inflation reports.

Breadth was stronger than earlier this week and is still clinging to its buy signal. New highs are starting to weaken again versus new lows, but that simply means rotation. Last Friday’s strong rally post jobs report had broad participation.

Volume picked up on Wednesday but so did volatility. Markets traveled more than 1% from high to low and back to highs again. With volatility weak and dropping most of the day that gives stock buyers the green light to add positions.

The range expanded on moderate volume. We still see the markets trapped in a box, but the Nasdaq seems to be making the first move, above some recent resistance. The Russell 2K and the Dow Industrials remain the laggards, but we’ll see if seasonally weak trends reverse before next week’s option expiration.

The Internals

What’s it mean?

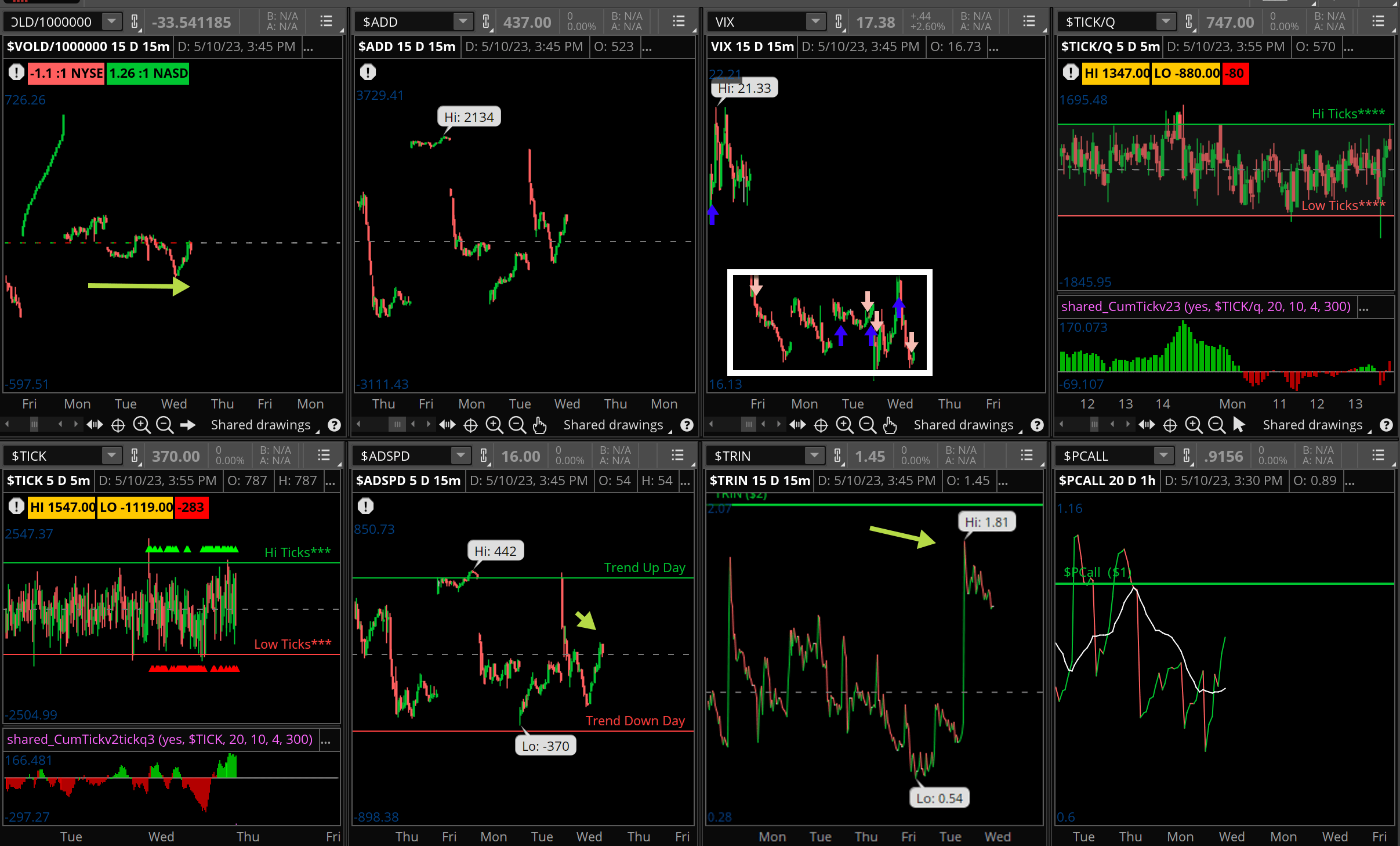

Nothing like a stall in the market to get your juices flowing. Certainly the CPI news was just taken in stride, not much energy to buy stocks yesterday as we see the VOLD, ADD and ADSPD simply hovering near the zero line. Ticks were mostly offset but the sign of complacency is in the VIX, which shows very little worry for stocks.

The Dynamite

Economic Data:

- Thursday: PPI, jobless claims

- Friday: Michigan sentiment, import/export prices

Earnings this week:

- Thursday: CYBR, DDS, TPR, UTZ,, INDI, SANM

- Friday: SPB

Fed Watch:

After last week’s meeting and a quarter point rate hike, we will see if the Fed speakers tone it down. Two Fed speakers later in the week. The key they will be looking for is a reduction in PPI. Inflation numbers were slightly better on the CPI side of things, and now May is looking even better. The wages number last week was much too hot, and while Chair Powell seemed sanguine on more rate hikes, he was adamant about no rate cuts, too!

Issues/Stocks to Watch this week

Volatility – The VIX was smashed down again Friday, far too low for comfort. We’ll see if it rises this coming week.

OPEC meeting – The last time they met it was a cut in production. We’ll see if that happens again, which might be a surprise.

Banks and Congress – Lawmakers say they are monitoring the situation with regional banks and their problems. Let’s hope they don’t step in and try to fix markets as they did once before – that was a disaster.