The Fuse

Futures are lower this morning as the stock market remains mildly overbought. Further, many are hesitant to commit capital before a debt ceiling agreement can be reached. It continues to be a stock picker’s market.

Interest Rates are headed higher this morning as the long end of the curve remains a sell trade. Rates have risen sharply higher this month as the 10 year is right close to 3.75%.

As it relates to the debt ceiling talks, they were constructive yesterday but details need to be hammered out. Overnight, news from across the pond was slowing economic data and inflationary trends, though one analyst believes the UK will miss having a recession.

Solid earnings from Dick’s and Lowes but a guide lower from the latter has not inspired buyers to step up to the plate. Some big tech names like Intuit and Palo Alto report earnings tonight.

Some big earnings coming up this week including NVDA, SNOW, COST, MRVL,LOW, DKS and ZM. All eyes/ears again this coming week on Washington and the debt ceiling discussions.

Breadth improved as the dip buyers continue to be active. Why not? When volatility remains low and even drives lower it means the environment is buyer friendly. However, we must be aware of the complacency as a reversal can happen at any moment.

Volume continues to weaken as we head into the holiday weekend. Much of the hesitancy is waiting on a deal in Washington, which may stoke some volatility and volume before too long.

Still seeing strong support below at 4100 and then 4050 on the SPX 500. For the Nasdaq 100, the clear support level is now 13.3K, which was finally exceeded and confirmed over a week ago.

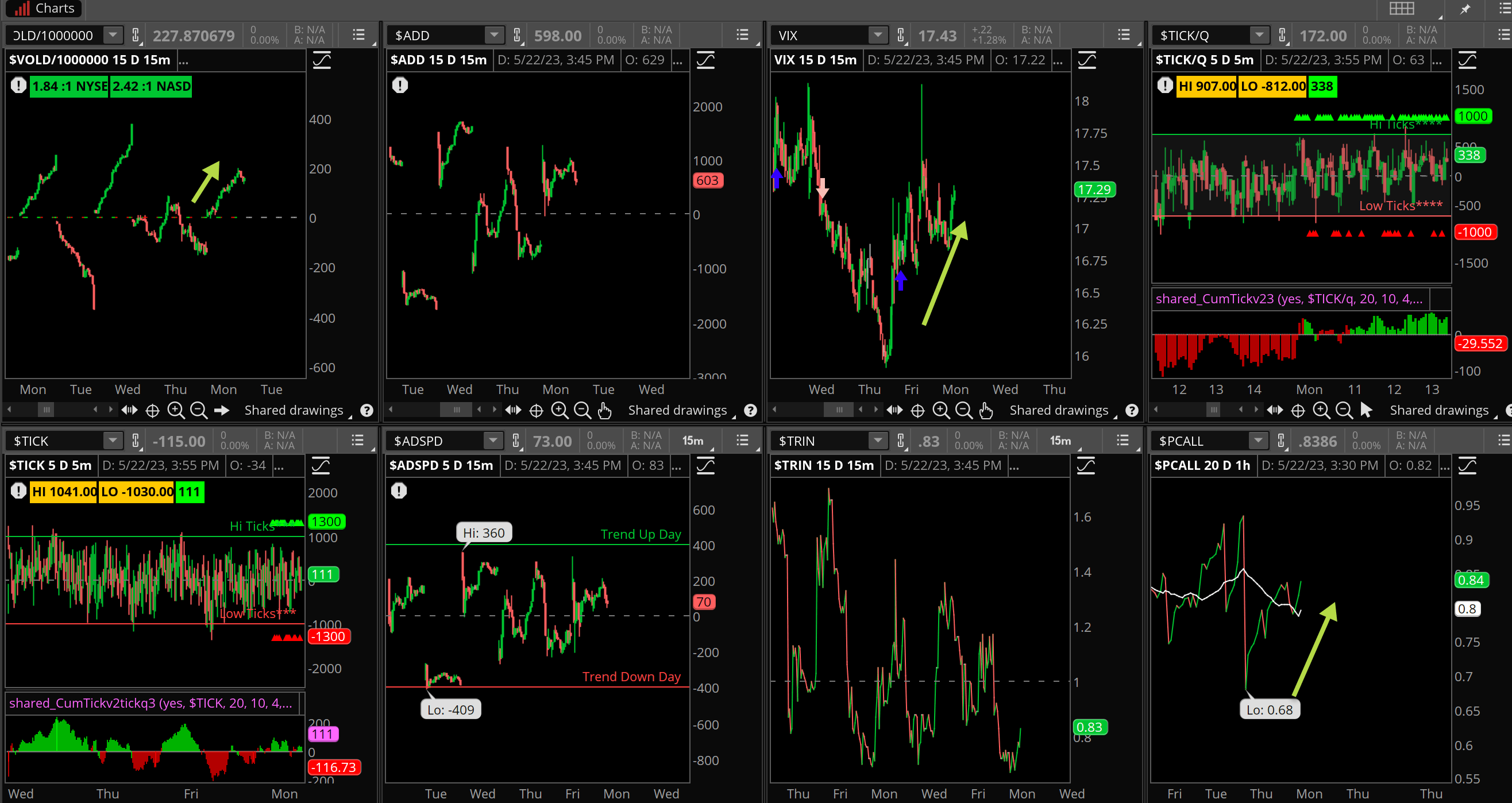

The Internals

What’s it mean?

Markets were off to a slow start Monday but did manage to rally. Unfortunately, the highs were eclipsed the SPX 500 was unable to close above 4,200. The internals were not impressive, but the VIX is suddenly catching a bid. VOLD was moving positively most of the day but crashed late, while put/call is starting to rise again, that is notable. Some strong sell programs hit during the day, those were seen on the ticks. Meaningful? Not yet, but we’ll have to see if they expand in time.

The Dynamite

Economic Data:

- Tuesday: Global Flash Manufacturing and Services PMI, New Home Sales April

- Wednesday: Mortgage applications, crude oil inventories

- Thursday: GDP second estimate, jobless claims, pending home sales

- Friday: PCE for April, Durable goods, Michigan sentiment

Earnings this week:

- Tuesday: AZO, BJ, DKS, LOW, WSM, A, PANW, URBN VFC

- Wednesday: ANF, ADI, DY, KSS, AEO, ELF GES, NVDA, SPLK

- Thursday: BBY, BURL, DLTR, RL, COST, DECK, GPS, ULTA, MRVL, VMW

- Friday: BIG, BAH, BKE, HIBB

Fed Watch:

Four Fed speakers out yesterday and all were pretty hawkish on monetary policy. We have one more coming up this week and possibly Chair Powell later today at a luncheon.

Stocks to Watch

NVIDIA – This stock is up strong in 2023 on hype and promise with AI. They will deliver earnings on Wednesday, we’ll see if it is a sell the news event.

Washington DC – Those dreaded debt ceiling talks continue as we march toward a hard deadline.

Volatility – In front of a holiday week, we often see volatility get smashed down by the end of the week.

[thrive_leads id=’60674′]