The Fuse

Equity futures are trying to regain some ground today but may have a tough time doing so with this being Friday. Markets are no longer overbought but are now trying to find some footing above the recent lows at 4,103 on the SPX 500.

Interest Rates are rising on the long end again as bond sellers remain active following the shockingly poor treasury auction yesterday.

Not much news overnight but Chair Powell delivered a hawkish message yesterday that spilled over, Europe was lower overnight, the Asia Pacific index was lower by nearly 1% while Emerging markets were also down about 1%. Gold is off by about the same while crude oil is higher by more than 1%.

Earnings were good for TTD last night but the guidance was very soft and missed estimates. Unity also was poor along with Wynn, missing their targets as well.

Markets were rocked after a very poor bond auction pushed rates higher. Stocks have been punished when rates have risen sharply and that was the case yesterday, no bids could be found following the auction. Further, Chair Powell did not hint at the committee’s policy position shift to a more dovish view, and reiterated their hawkish stance.

We mentioned the other day how poor breadth had been this week and it would eventually fall on the markets. That happened yesterday, breadth is back on a sell signal following a rout. Four straight days of negative breadth was enough to do it, we’ll see if the sellers finish it up today and turn around the markets next week.

Heavier turnover should be a minor concern as the sellers took control and released stock in size Thursday. One day of distribution (it was a strong one) should not be a concern yet, but a few more will be, there are many gaps lower that need to be filled, down to 4,125 or so.

The air is thin up here as the bulls are gasping right now. Any sort of negative news like a bad bond auction is going to push the markets down, but how far is the question. The 4,400 level on the SPX 500 was approached yesterday but failed to tag it. The Russell 2K is failing to hold again and is heading back down, that could drag the rest of the market with it.

The Internals

What’s it mean?

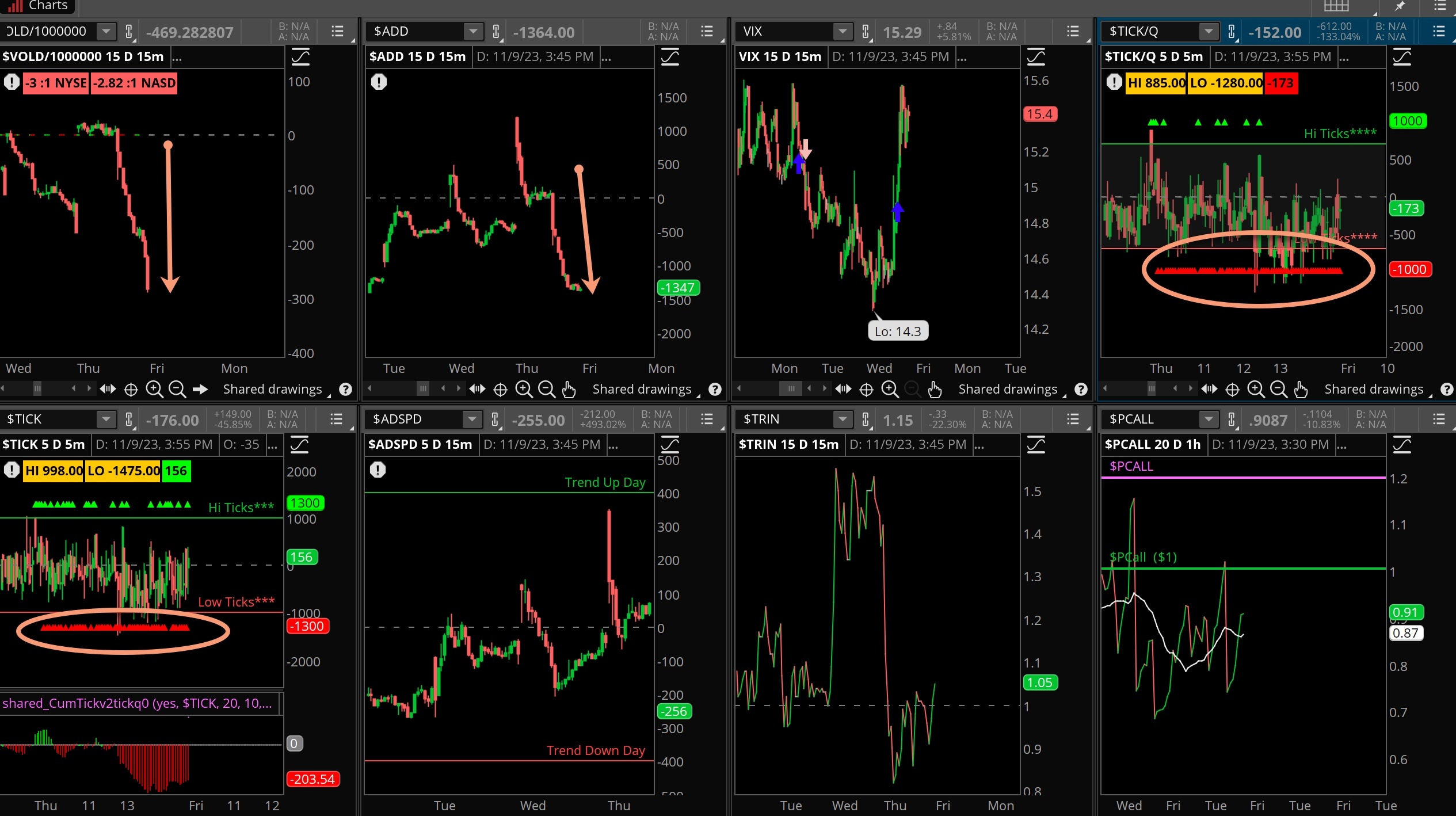

We mentioned yesterday the heavy put/call reading above 1 and that would be a concern to the bullish case, especially short term. Well, that did them in, along with a more concentrated amount of red ticks in both windows. The VOLD was straight down too, we haven’t seen that in a couple of weeks. A one-off? We’ll have to see, but certainly the gains made recently could be harvested. A higher low in the chart would be very bullish, but the down move would have to stop soon.

The Dynamite

Economic Data:

- Friday: Michigan sentiment, treasury budget, consumer sentiment

Earnings this week:

- Friday: MGA

Fed Watch:

Quite a few Fed speakers out this week including Chair Powell who threw cold water at the market. The implication the committee is not finished yet seemed to be lost while stock buyers were busy, but his message rang loud and clear yesterday.

Stocks to Watch

Disney – The House of Mouse will deliver earnings this Wednesday and after a stellar week the setup is there for some disappointment following the release. However, if the stock pulls back it could be a good buying opportunity.

Interest rates – This past week saw a huge drop in rates on the long end of the curve, and the stock market rallied on it. That move down in yield was exaggerated enough, but many still see inflation coming down. We need to see more evidence, else rates will climb right back up.

Seasonal patterns – November is considered on of the best performing months for the stock market over the last 20 years, tied for first.

It is even better than December when Santa Claus is due to arrive. We’ll see how far this seasonality is carried.

[thrive_leads id=’60674′]