The Fuse

Stock futures are pushing a bit higher this morning as traders await the important PPI number to be released before the open. Yesterday’s CPI was mostly in line, still reflecting some sticky inflation. Later today we’ll hear from Chair Powell just before the close of trading.

Interest Rates are coming off their recent highs, bond are rallying a bit this morning. That could change of course with the PPI release today and retail sales on Friday am. The 2 year yield remains strong around 4.3%, this bond telling us inflation is likely to remain for some time. Fed funds futures have backed away somewhat, seeing perhaps 3 rate cuts only in 2025 rather than 6 a few weeks ago.

It’s been nine days since the election and Donald Trump is shaping his cabinet, which may have a trickle down effect on the economy and thus the stock market. Overnight saw strength in Europe, the Stoxx up .3%, the dollar continued its amazing climb,, gold is getting hammered again, down 1% while crude remains in a range, it is up .5%. German bund yields were flat, US treasury 10 yr yields were also flat, stocks in Asia were down. Japan was off .5%, Hong Kong and Shanghai lost big time, down 2% and 1.7% respectively.

Earnings from Cisco last night were very strong with good guidance, this morning very strong guidance from Disney after a mixed quarter, that stock is higher by 5% and is helping to lift the Industrials. Tonight we’ll hear from Applied Materials and a few smaller names, Alibaba on Friday morning.

The digestion of recent gains continues. Stocks were mixed but stymied again by the poor performance of small cap stocks. The Russell 2K (IWM) was down sharply again, off 1% on higher turnover. We usually see higher interest rates as the culprit but this time around it was simply an overheated market. That said, the CPI number came in line with expectations and many breathed a sigh of relief but then soon realized the market may have priced it in, selling hit right then. Will tomorrow’s PPI be the same response?

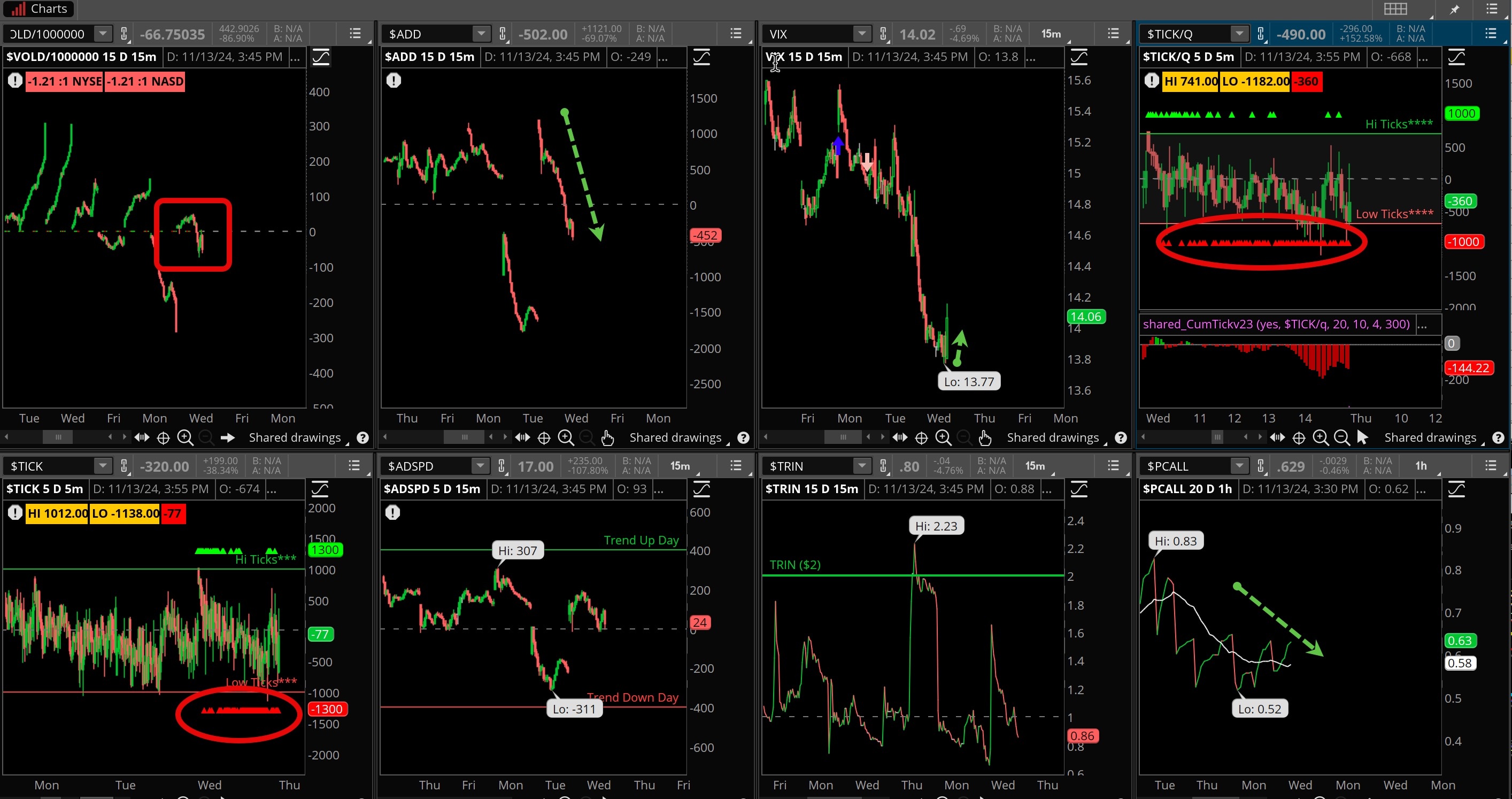

Breadth was noticeably weaker again yesterday with the decliners just beating out the advancers. With early strength and a fade late in the day it is getting harder for dip buyers to flex their power. If stocks don’t rally this group will disappear and the markets will be left in the dust. There could be some downside action as this indicator is now on a sell signal. New highs continue to beat new lows however, and the oscillators are mildly oversold.

We saw better turnover on the SPY but it was a positive day, barely. Other indices had lower turnover, thankfully for IWM and QQQ, which would have notched distribution days if volume was higher. As it is, these indices have been under a great deal of pressure, and more volume to the downside will ignite a slew of more selling, should the dip buyers depart for the time being.

Stocks continue to test some shallow levels but refuse to break. That tells you the strength of this market rally, which continues to show where the power is. Tech names were fairly strong and distributed rather evenly. We still see good support on the SPX 500 down at 5870, resistance at recent highs around 6010 or so. The Industrials remain buoyant, 45K is not far off for this index.

The Internals

What’s it mean?

More of the same Wednesday, the VOLD just can’t seem to get it together, the ADD made its highs early and just was drowning the rest of the session. Ticks were awful, mostly red and increased during the trading day. The VIX did hit low numbers, under 14% at one point and bounced. We might see another run lower after the PPI release. If this is the modest corrective action after last week’s surge, it should be ending rather soon.

The Dynamite

Economic Data:

- Thursday:Jobless claims, PPI, Fed speakers (including Chair Powell)

- Friday:Import prices, Empire State Manufacturing, Retails sales, industrial production, cap utilization, NYF President John Williams

Earnings this week:

- Thursday:DIS, AMAT. POST, JD, AAP

- Friday:BABA, BKE, FL

Fed Watch:

The committee delivered a big rate cut last week, and now the market is focused on December. The futures market sees a strong possibility of this happening, but the data is going to need to come in as hoped for. This is a huge week for Fed speakers, and Chair Powell will be heard as well along with some other important names. Interesting they are all coming up with some important inflation data.

Stocks to Watch

Nasdaq – New highs for this index as it is now taking taking the lead. Remember in 2023 this index was up 53%. That is not likely achievable again but having the power to bring the other markets up is a huge advantage.

Tesla – After the election results, Elon Musk’s company really stepped on the gas and moved higher. The all-time highs are about 30% away but this stock has incredible momentum and could certainly make a run there before year end.

Inflation – With CPI and PPI readings due out this week, the expectations are for the core to continue dropping. The Fed has made great progress in bringing down prices but more work is needed. Policy is still restrictive, but with better inflation numbers the committee will bring rates down faster.