The Fuse

Amazing rip higher on futures as volatility collapses following the win by Donald Trump. The anticipation is high along with expectations the economy and the stock market. New all-time highs are within reach today if the market gains hold.

Interest Rates are backing up as the new administration perhaps would put in place some inflationary policies. The 30 yr is pushing higher, the 2 year yield now above 4.2% after it was gently sliding backwards. Today starts the Fed meeting, where they will discuss policy and likely cut rates one more time to 4.5%.

Clearly the big news overnight was a win for the Republicans, but there are losers too. Hong Kong’s market fell sharply, down 2% Shanghai only a bit but that may change tonight. Europe on the other hand was up very strong, 1.4% while the dollar popped 1.3%. German bund yields fell 3 bps, US treasury yields mushroomed higher, 12 bps to 4.4%.

Earnings last night from SuperMicro last night were an unmitigated disaster. Microchip also spit the bit, so did Exact Sciences. This am strong earnings from CVS. Tonight we’ll hear from ARM, Qualcomm, ELF, Applovin, Mercado Libre and a few others.

A very solid day for the indices, stocks started off strong and finished even stronger. The best work was done by small caps, which rallied nearly 2% on heavy turnover. That made sense with interest rates dropping for the first time in days. If there is a strong followthrough day we are looking at massive momentum to the end of the year.

Solid breadth puts this indicator on the cusp of a buy signal. What is impressive about Tuesday’s action clearly was the landslide of advancers over decliners, better than 5-1. We have not seen that sort of skew in weeks, but the bulls have notched a good win. Oscillators are back to neutral, Nasdaq is positive while NYSE is modestly negative. New highs starting to expand again over new lows, this indicator can be on a buy signal very soon.

Strong volume yesterday as the indices triggered an accumulation day. That means big institutional sponsorship, hedge funds and mutual funds were loading up all day long. Perhaps a signal the election is over and it is time for the stock market to move forward. We have a big Fed meeting starting today that will have some influence for sure, and probably bring in more volume.

There is little doubt 5,700 is good support. Just below that level the market held on Monday, and with a followthrough today the bulls would be hopeful. Nasdaq has even better support levels at 20K, while the Industrials see 42K as support but sights set on new highs. Small caps are the real deal though, with levels at 220 holding. A move above 230 would cinch a move to new all-time highs.

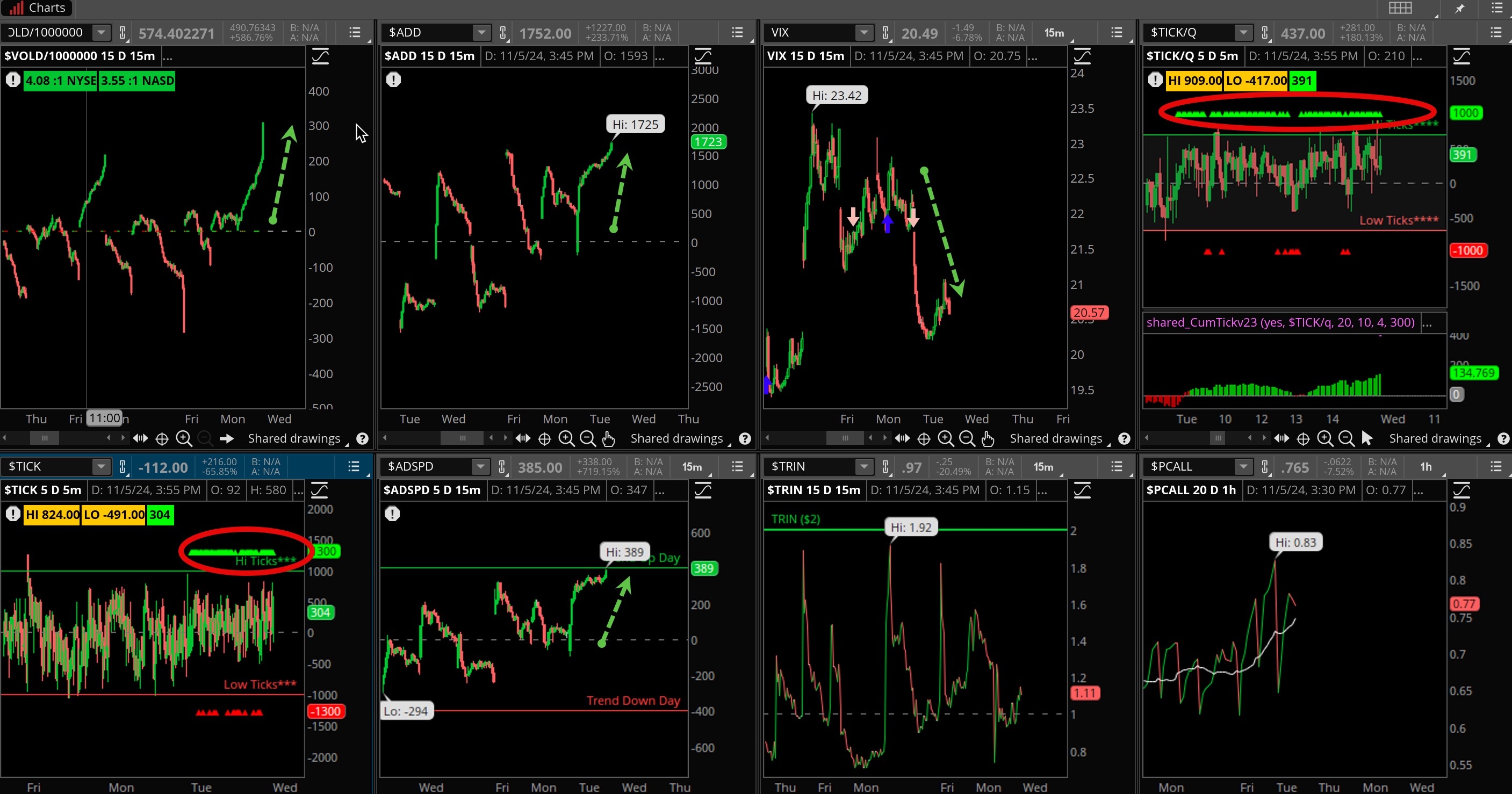

The Internals

What’s it mean?

Huge turnaround for the internals, a sparkling turn. TICKS were green all day, buy programs in effect. Check out the VOLD, straight up end of day, something we haven’t seen in over a week. ADSPD was nearly a trend up day, ADD finished strong, something we have not seen recently, while the VIX was slammed. That could continue this week.

The Dynamite

Economic Data:

- Wednesday:SPX final US services PMI

- Thursday:Jobless claims, productivity, FOMC rate decision, consumer credit, inventories

- Friday:Consumer sentiment

Earnings this week:

- Wednesday:CELH, CVX, TEVA, TM, JCI, ARM, AMC, QCOM, ELF, APP, IONQ, CLOV

- Thursday:VSTR, GOLD, DDOG, HAL, HSY, MRNA, DKNG, ANET, SQ, RIVN, U, TTD, AFRM, FNET, PINS, ABNB

- Friday:SONY, IEP, FLR, NRG

Fed Watch:

Another Fed meeting is upon us and the Fed futures market predicts a cut after Thursday’s meeting. That is likely the case as the committee has no reason to disappoint the crowd, but debate about a December cut will certainly be heard. The job report Friday (poor) may be an anomaly, but if it is slowing that quickly a faster rate cut policy may be appropriate.

Stocks to Watch

Election – We have finally come to the day that can change the US. We should know how things turn out later in the week, the effects on the market and economy will be analyzed.

Federal Reserve – The seventh meeting of 2024 will take place this week, the committee is largely expected to cut rates once more, this time by .25%. That may not sound like much but with lower inflation it makes sense for the committee to bring down borrowing costs.

Earnings – It is another big week of earnings as the season comes into the halfway point. 1/3 of the SPX 500 reported last week and very little damage was felt. Many stocks reporting this week have strong chart patterns and formations, we’ll see if that continues to be the case.