The Fuse

Equity futures are starting off slow this morning after a moderate dip overnight. Stocks have rallied smartly early in the week to erase some of last week’s heavy selling and negative moves but have a ways to go. Volatility remains elevated, CPI may trigger some trading but a beat would be needed to shift the markets moving upward.

Interest Rates are sliding in front of a big inflation report, long term rates are dropping into dangerously low territory. Is the bond market’s concern over growth unfounded or fair? Fed funds futures are rallying in kind, the market now sees 4 1/2 rate cuts happening by year end, much different than the committee is looking at. Something has to give, the Fed is usually right so the market may be adjusting soon much as it did in April.

Today is a solemn day in the US as it is the 23rd anniversary of the 9/11 attacks, we never forget. In Europe stocks gained some ground, gold is up as is crude oil, which is rallying more than 2% in early trade. The US dollar has dropped before the release of the CPI for August. German 10 year bund has steadied.

Stocks in Asia were lower, Japan down sharply, 1.5% while Hong Kong and Shanghai also fell nearly 1%.

Earnings from GameStop last night were a disaster, Dave & Buster’s were strong with good guidance. The reports thin out later in the weeek, Adobe and RH report on Thursday evening.

Stocks in the tech sector rose smartly, mostly from overbought conditions. The markets await some inflation data the next couple of days, so that may cause a bit of movement on either side of the trade. Banks were hit hard after JPM and GS said they had seen some softness and estimates were too high. That caused a big move down in the entire financial group. We could see more selling here over the coming weeks if more bank numbers are cut.

Breadth was rather poor and did not portray the strength in the SPX 500 nor the Nasdaq. That’s okay, because Monday’s strong breadth was exhaustive. We must remember the price action matters most, all other indicators are mostly supportive of the price action, rarely a divergence. Oscillators are still negative, new highs are back to trouncing new lows.

Turnover was a bit lower than yesterday but certainly on the better side of things. The bulls would like to seem better turnover on these up session so they can notch a few accumulation days. As it is, the indices are offering some opportunity for accumulation later in the week if all positive for the inflation reports.

Some long-legged candles formed yesterday which means lower levels were successfully tested. That is good news for the bulls, as those levels saw buyers stepping up to the plate to do some buying. It could be those lower levels were cleared for a much bigger move up over the next few days with inflation readings coming out. Resistance for SPX 500 remains at 5,500 but the index is knocking on the door.

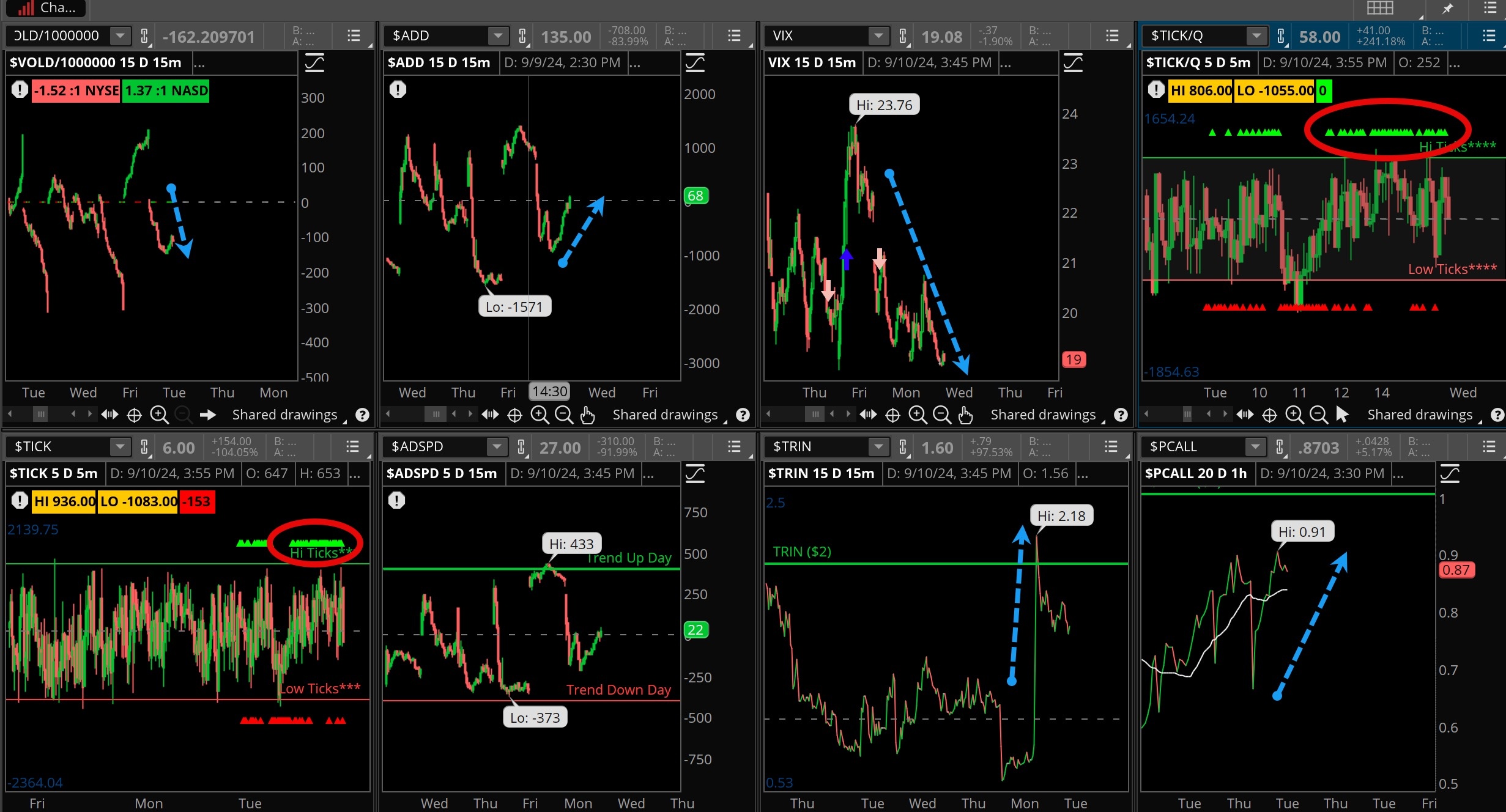

The Internals

What’s it mean?

A less than exciting day for the markets, the internals show a low VOLD but a much better ADD. That tells us the volume was not supporting the price moves, and that could wind up being dangerous. Put/calls are on the rise too, ticks were mostly red early when sell programs took hold, but buyers came back during the last hour of trading. The VIX did fall once again and stands right near 19%. A bigger move down could trigger an avalanche of buying. TRIN made a big move above 2, which tells us the skew between ADD and VOLD was wide.

The Dynamite

Economic Data:

- Wednesday:CPI

- Thursday:Jobless claims, PPI, federal budget

- Friday:Import prices, consumer sentiment

Earnings this week:

- Wednesday:VRA, OXM

- Thursday:BIG, KR, SIG, ADBE, RH/span>

- Friday:N/A

Fed Watch:

No fedspeak this week, the committee is in their quiet period before next week’s crucial meeting. The data this past week still shows the economy is chugging along at a moderate pace, though some metrics in the labor report see chinks in the armor. A few fed speakers during the week stated the committee is ready to commence with a rate cutting policy which in our view will last quite awhile as the FOMC looks to reduce the tight conditions that have existed for a couple of years.

Stocks to Watch

Apple – A big event is scheduled for this week, but recent weakness in the stock means there has been little excitement to buy Apple. Can that sentiment turn around or will this new iPhone introduction (likely) be another excuse to do more selling.

Inflation – In Jackson Hole we heard Chair Powell declare the time had come for rate cuts to start. That of course could start next week, but there are still important inflation reports to consider this week. Will the CPI confirm the Fed’s view that inflation is right near target?

Nasdaq – It was the worst week in a year for stocks, the Nasdaq took the brunt of the punishment. Can it recover or will we see another lower higher, lower low in the weekly chart? The 50 week moving average is not far down from here, about 800 points which can be tagged easily with elevated volatility (currently).