The Fuse

After a long weekend stocks are backing up a bit and are on the defensive. Gold and silver prices are up, yields are higher and the VIX is rising. The new month gets started today and it is often pretty bumpy in September, we’ll see how things go but a negative start during this short week could be troublesome.

Interest Rates are ripping higher today as global inflation is around us. No question the tariffs have contributed to some inflation but in the eurozone those numbers are far higher than expected. Two year yields are higher as well, fed futures are backing away from aggressive rate cuts and the 30 yr is moving back up.

Stocks across the pond were down modestly overnight, the STOXX down .5% led down by France and Germany. The FTSE was off .4%, the US dollar index with a big surge up .4%, gold is sharply higher as is silver. Crude oil is up more than 2.5%. Yields are up as well across the board, German 10 yr bunds and 10 yr US treasury yields up 3 and 4 bps respectively. In Asial Japan climbed .3% but China markets were lower, Hong Kong down .5%, Shanghai off .4%.

Earnings should be interesting this week. Tonight we hear from Zscaler and HealthEquity, tomorrow Macy’s, DollarTree, Campbells, J.Jill and then Salesforce and Credo along with Asan, Figma, Gitlab and American Eagle. Thursday brings Broadcom, Lululemon, Docusign, Guidewire and Samsara.

The markets held their breath waiting for a strong report from NVIDIA this week, it got one but the reaction was poor. We warned earlier on the week that perhaps a good number was already priced in. Further, some data seems to portray inflation still being a problem, something Chair Powell has widely viewed as unwanted. Trading at/near all-time highs is impressive though, but leading into this new month is going to get dicey.

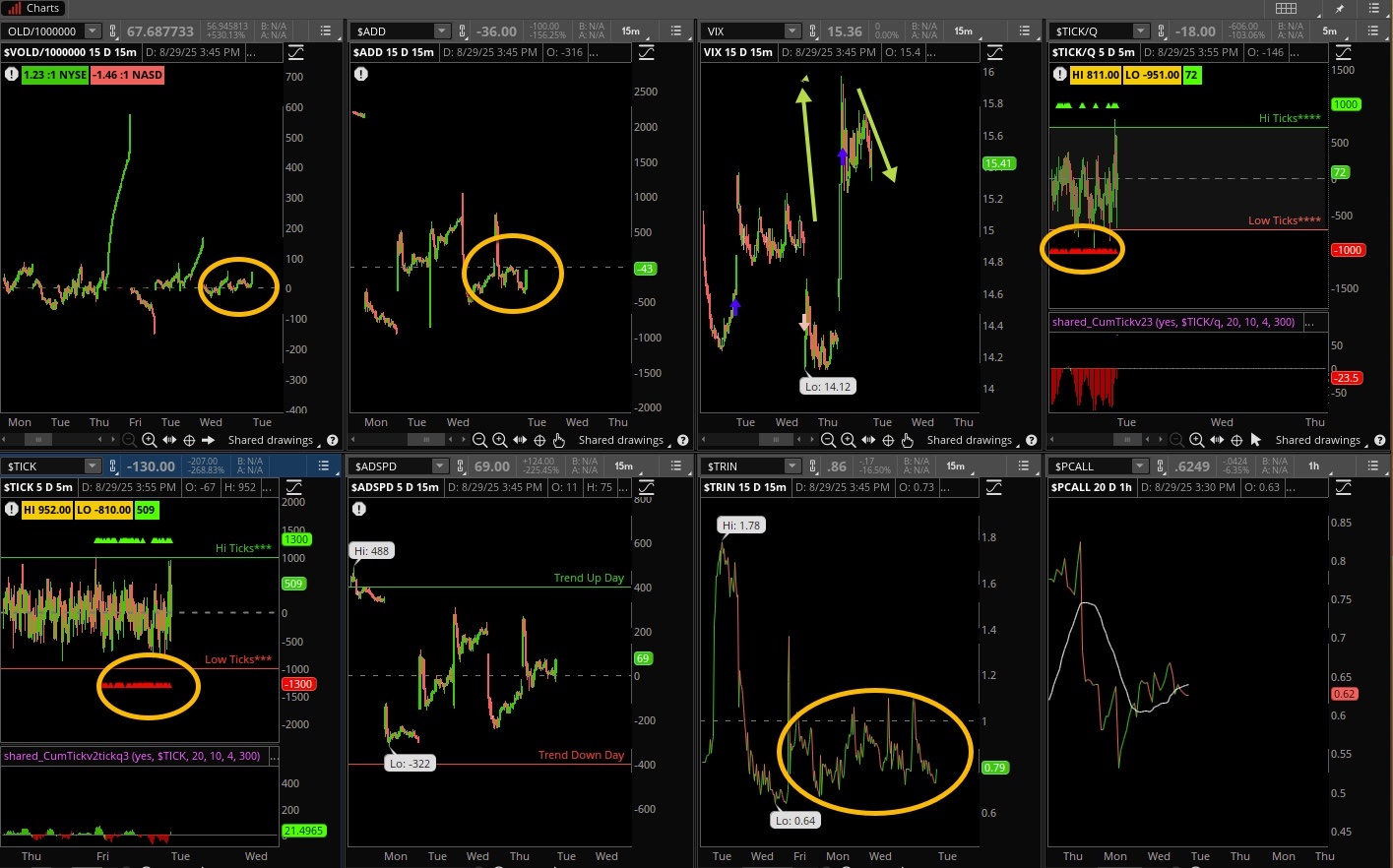

Breadth was negative but not all poor considering the deeper losses in the SPX 500 and Nasdaq. Oscillators are mostly straddling the zero line, what one might expect when volatility is quite low. New highs continue to trounced new lows, that indicator is on a buy signal.

Volume printed another low day but we might start seeing more turnover in the coming weeks. If we do get a rise in volatility as we might expect over the next several days look for an expansion of volume. Though we have jobs data this week and a few big earnings reports there is not much more to drive the turnover other than new highs, which most traders tend to stay away from.

Are the indices struggling to make new highs here or is this just a seasonal trend working its way through? Hard to say but clearly the indices are churning here, some of the big volume and price days we had recently need some time to work off their overbought conditions. As it stands, stocks may pull back here to the 20 day moving average again where traders will re-assess where things are at. That could be a one percent down move.

The Internals

What’s it mean?

More sideways and lethargic action for the internals. There is just no momentum here save for a couple of recent days. For the most part, VOLD and ADD have been banished from the bulls’ cause. We don’t look at TRIN too often but notice how low that indicator has been for a couple weeks now. VIX rose but finished off its highs, while TICKS were mostly red all session – many sell programs. that may continue today.

The Dynamite

Economic Data:

- Monday:n/a

- Tuesday:PMI, construction spending, ISM manufacturing

- Wednesday:Fedspeak, JOLTS, factory orders, fed beige book

- Thursday:jobless claims, ADP, productivity, trade deficit, ISM services, fedspeak

- Friday:jobs report for August, wages

Earnings this week:

- Monday:n/a

- Tuesday:NIO, ASO, SIG, ZS, HQY

- Wednesday:DLTR, M, CPB, JILL, CXM, CRM, CRDO, AI, AEO, GTLB, HPE, PD, ASAN, FIG

- Thursday:FLWS, SCVL, TTC, DAVA, CRMT, GIII, CIEN, BRC, DLTH, AVGO, LULU, DOCU, PATH, IOT, BRZE, CPRT, GWRE, TTAN

- Friday:ABM

Fed Watch:

We have heard quite a few opinions from the those on the Fed about how/when monetary policy should shift. On Friday Governor Waller said ‘lets just get on with it’, meaning a rate cut cycle should start. That is not exactly where Chair Powell resides, his opinion weighs heaviest. Data still seems to show inflation is elevated beyond the Fed’s target but labor this week is going to be a key number.

Stocks to Watch

Volatility – Once again, the market remains complacent and could be paying it back huge this week. The VIX is sublime, residing under 16% for awhile now. It is not bearish until it starts to rise, which could be at any moment.

NVIDIA – After strong earnings and guidance the stock took a hit on Friday. Can it stabilize and recover? Not much news to drive it in either direction, so maybe some base-building is in order.

Jobs – The August labor report will be watched closely on Friday to see if weakness continues from the prior months. It would only seem fitting after the BLS commissioner was dismissed to see numbers suddenly rise, but that’s a topic for another day.