The Fuse

Equity futures are rallying modestly this morning with no news over the weekend to wake up volatility. The VIX however is a bit higher today as it has been stretched from away from the September future. We’ll see that gap narrow a bit more as we get closer to the future expiration. Other than that, a week to pay attention to the data.

Interest Rates are pushing lower in front of the fresh August inflation data. Those reports will be out later this week, but given the fact bonds have been strong lately the momentum continues. 2 year yields are down and headed much lower on Friday following the labor market report (weak). We also saw longer term yields drop as well. There is a good feel for a rate cut next week, futures markets are even predicting a chance at a 50bp cut, though that is quite small.

Stocks in Europe were up nicely, the STOXX higher by .3%, led by nice gains in Germany and France. FTSE added a small fraction, gold is barely up while silver is on the move. Crude oil is up nicely, higher by more than 2% while the US dollar index fell .1%. German 10 yr bund yields fell 1bp, US 10 yr treasury yields rose up 1bp and in Asia strength in Japan, up 1.5% and Hong Kong along with Shanghai as well.

Earnings are sparse this week but we will hear from Oracle on Tuesday, a report which could move markets. Kroger is also very interesting along with Synopsis and Chewy. As we move our way towards the end of the month the big reports will start slowing down and other catalysts will be needed to keep the market afloat.

A down day but will off the lows as the markets start to grapple with some potential weakness in the economy. Two consecutive weak labor reports might have the Fed concerned about keeping up with trend growth. The futures market now points to likely three cuts in rates to the end of the year, the first one about 99% baked in for next month’s meeting.

Breadth was pretty good actually considering a down day for markets, that is unusual. But given the fact money is rotating around it is not a surprise. The small cap IWM has been moving higher and with it comes better breadth. Oscillators are now positive, that is a good sign for the bulls to continue this rally.

Volume expanded Friday and with the down session this counts as a distribution day. However, we have not had many of those lately so we’ll just consider this a ‘normal’ session of selling, not indicative of further downside yet. We could see that expansion of volume come alive later in the week.

It seems some short term levels of support were tested successfully on Friday, though we remain skeptical. There is little evidence yet to say if a bigger selloff will hold, but the 20 day moving average does provide a level of good support in case some heavy hitters decide to step aside.

The Internals

What’s it mean?

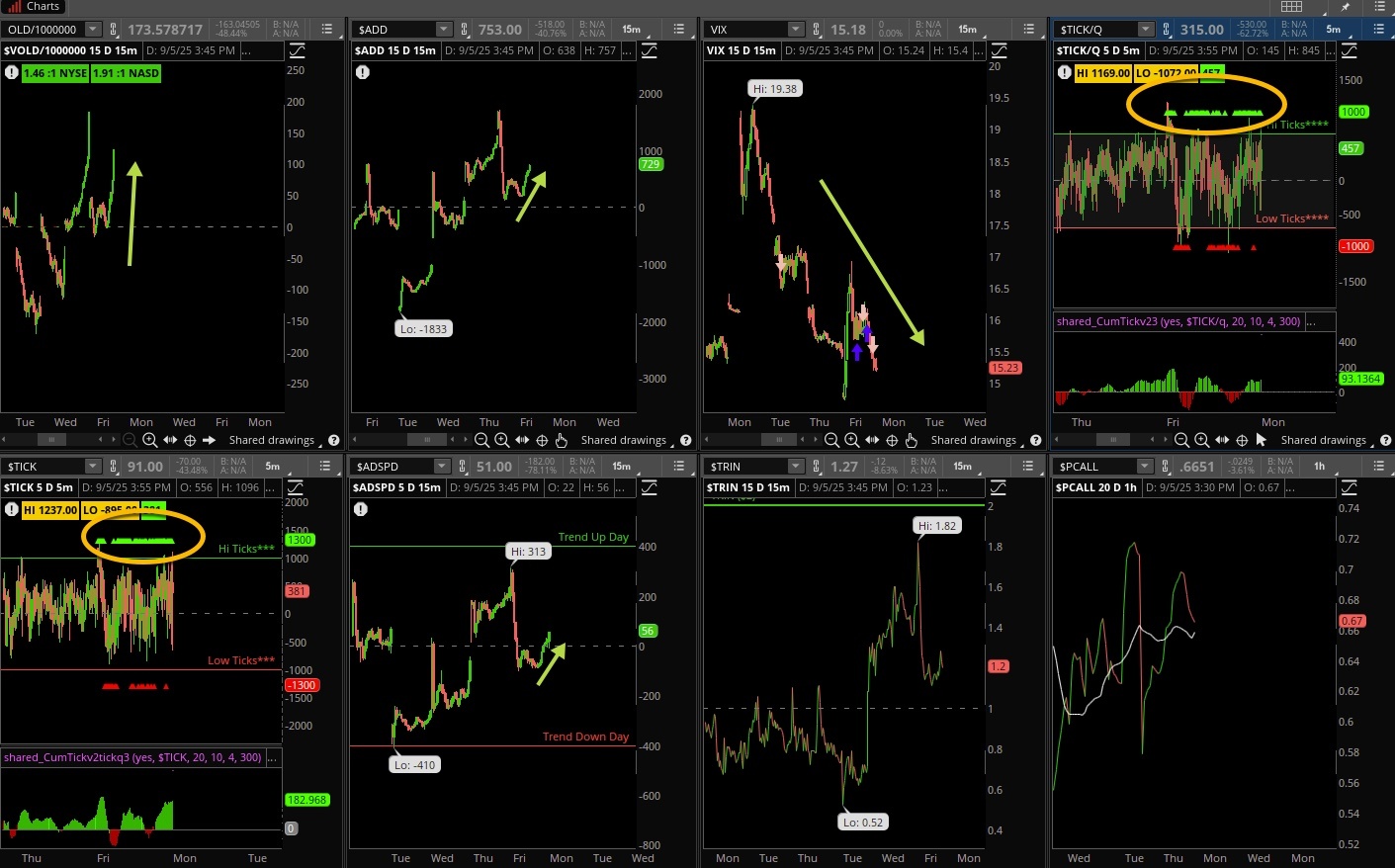

The stock market did not initially like the August jobs report, though it did not really start selling off until after the open. Notice though the underlying strength of the internals, where the VOLD was up and finished at the highs of the day, so did the ADD and ADSPD. There was buying underneath. TICKS were green most of the day, some heavy buy programs. VIX did its thing, rallying and then selling off after the news.

The Dynamite

Economic Data:

- Monday:Consumer Credit

- Tuesday:NFIB optimism index

- Wednesday:PPI, wholesale inventories

- Thursday:CPI, jobless claims, US budget

- Friday:Consumer sentiment

Earnings this week:

- Monday:PI, CASY, MAMA

- Tuesday:SAIL, FCEL, DBI, SI, ORCL, GME, AVAV, SNPS, FE, RBRK, METH, LMNR

- Wednesday:CHWY, DART, ZENV, SLAR, OXM, CULP, VNCE

- Thursday:KR, LOVE, VRA, HOFT, ADBE, FARM, KMTA

- Friday:

Fed Watch:

We heard plenty from the Fed last week and will have nothing this coming week as the committee is in a ‘quiet period’ before the next meeting. That could be raucous, with both doves and hawks digging their heels in to support policy measures. Will it be one, two or no cuts?

Stocks to Watch

Bonds – Once again, we’ll be watching bonds here, especially yields and if they move sharply higher following CPI and PPI. That might only happen if a hot number comes.

Gold – Some big central banks have been buying gold hand over fist, and that has pushed the metal to all-time highs. Gold and silver are outperforming markets in a huge way this year and that may continue.

Technology Stocks – Some were hot early in the week like Google, but NVIDIA fell sharply even as Broadcom rose up to new all-time highs. Semiconductor stocks have not responded well to President Trump’s rhetoric.