The Fuse

Equity futures are pushing higher again, trying to followthrough on Monday’s moderate gains. News will certainly move market with inflation reports the next couple of days and big tech name Oracle releasing earnings, which might have some influence. Sentiment is pretty bullish at this time, so there is caution warranted.

Interest Rates are slightly higher this am after a nice session with lower yields on Monday. Bond buyers were active at the start of the week, we’ll see if that continues. The two year remains in a downtrend, again portraying a much more aggressive fed policy down the road. Long term rates have remained strong, also high yield spreads are tight. Fed futures seeing three cuts still in 2025 happening.

Modest gains in Europe with the STOXX rising .2% led by a .3% gain in France. The FTSE matched gains in STOXX. Gold is making its way towards 3,700 per ound, sill slightly down and crude up nearly .7%. The US dollar index fell .1%. Yields across the globe are up slightly, 1bp for bunds and 2bps for US treasuries. Stocks in Asia were mixed, Japan down .4% along with Shangai down .5%, Hong Kong up .9%.

Earnings from Casey’s General Store were pretty decent. Tonight we’ll hear from Oracle, Synopsis and Rubrik along with GameStop. Tomorrow am we’ll have Chewy.

Not a bad day for the bulls as the SPX 500 finished just under an all-time high and below 6,500. That seems to be a brick wall but with the nice broad rally that may be coming in days it is not likely to hold for too much longer. Nasdaq did tag a new high on good turnover.

Positive breadth Monday but nothing too elaborate. There was bullish action all day long but not the rout one would expect. Regardless, new highs beat new lows again, that indicator is on a buy signal while the oscillators remain bullish.

Low volume today as maybe traders don’t want to get too involved yet before the big data dump later in the week. No doubt volume will pick up later in the week as the inflation reports have some influence. A fed meeting is not far off, the committee will be reading the data carefully. As such, we may see volume pick up even next week, with a big triple witching event next Friday.

Support levels continue to rise with the markets, and that means the moving averages are rising as well. It is a good situation for the bulls as these rising support levels are a nice ‘pin’ underneath current levels. We may see bigger slides down the road, the 50 ma is about 2% lower so any drop there might be picked up by the dip buyers one more time.

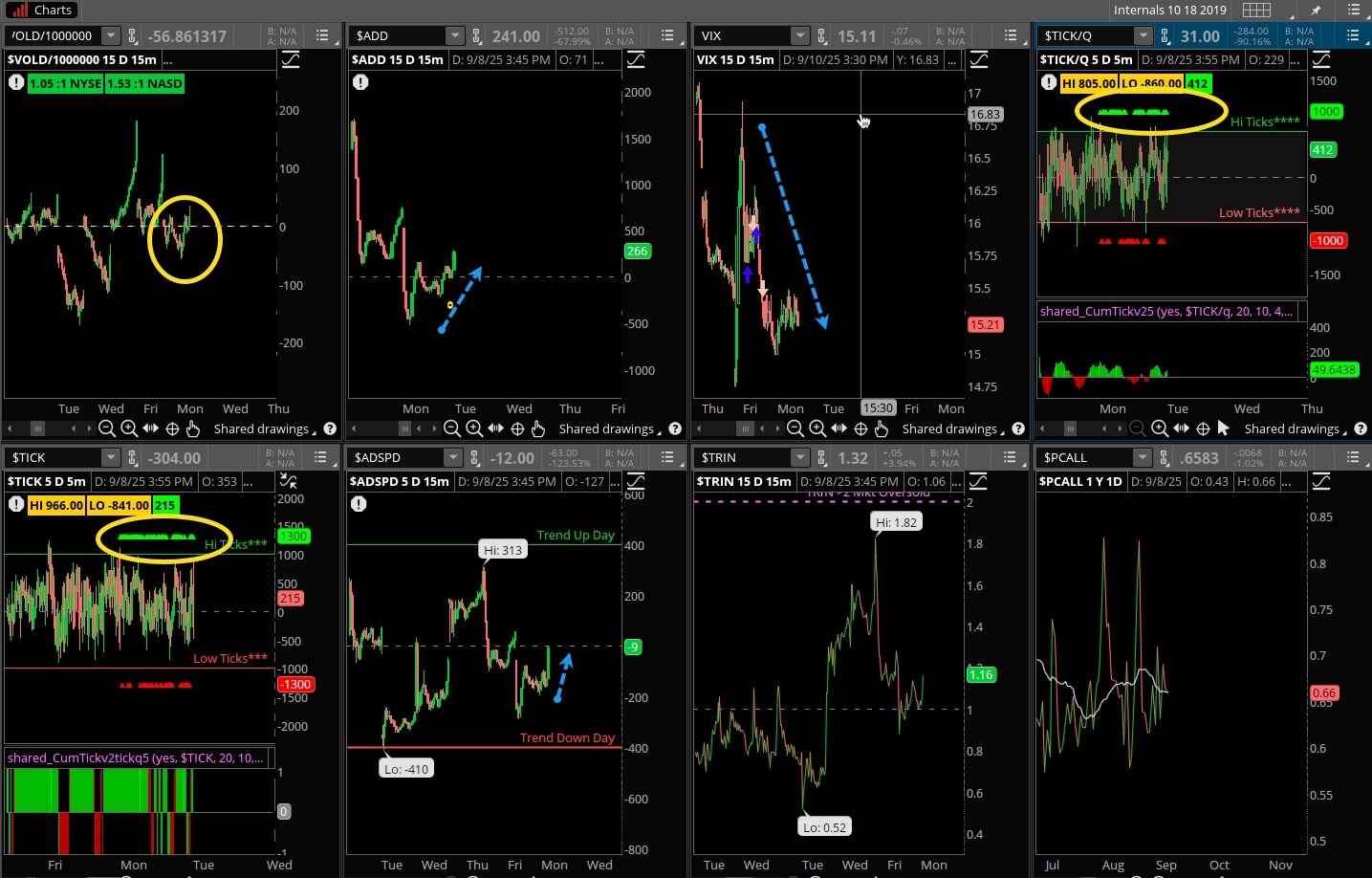

The Internals

What’s it mean?

I’m going to say modest improvement in those internals. The VOLD and ADD were not screaming out loud, and the ADSPD was decent but only finished at the zero line. Ticks were evenly distributed, VIX fell sharply again and is still hovering near 15%, put/calls remained contained. We look for better action from the internals later in the week.

The Dynamite

Economic Data:

- Tuesday:NFIB optimism index

- Wednesday:PPI, wholesale inventories

- Thursday:CPI, jobless claims, US budget

- Friday:Consumer sentiment

Earnings this week:

- Tuesday:SAIL, FCEL, DBI, SI, ORCL, GME, AVAV, SNPS, FE, RBRK, METH, LMNR

- Wednesday:CHWY, DART, ZENV, SLAR, OXM, CULP, VNCE

- Thursday:KR, LOVE, VRA, HOFT, ADBE, FARM, KMTA

- Friday:

Fed Watch:

We heard plenty from the Fed last week and will have nothing this coming week as the committee is in a ‘quiet period’ before the next meeting. That could be raucous, with both doves and hawks digging their heels in to support policy measures. Will it be one, two or no cuts?

Stocks to Watch

Bonds – Once again, we’ll be watching bonds here, especially yields and if they move sharply higher following CPI and PPI. That might only happen if a hot number comes.

Gold – Some big central banks have been buying gold hand over fist, and that has pushed the metal to all-time highs. Gold and silver are outperforming markets in a huge way this year and that may continue.

Technology Stocks – Some were hot early in the week like Google, but NVIDIA fell sharply even as Broadcom rose up to new all-time highs. Semiconductor stocks have not responded well to President Trump’s rhetoric.