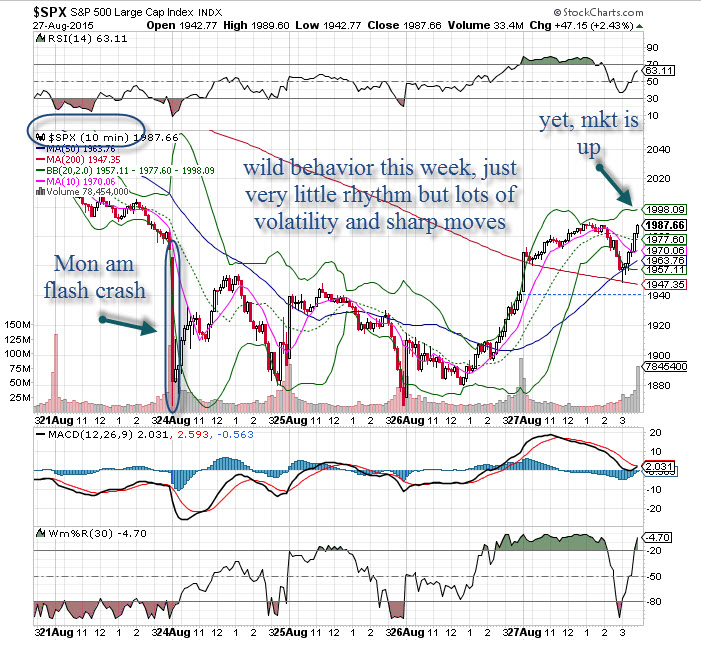

When markets opened on Monday, August 24, a slew of sell orders were already lined up, causing many computer systems to go haywire. Many brokers were locked out, and with market makers and specialists unwilling to take action, we saw enormous bid/ask spreads, stops being hit at very low levels, and frozen markets. This all occurred at the opening bell, and it was quickly fixed when some traders saw opportunity and dove right in on the buy side.

This was flash crash 2015, and it happened so quickly that nobody seemed to be concerned. In fact, no one expressed shock that it happened, which I find really surprising.

For the past five years, I’ve heard discussion about “bears” who vowed to get a piece of the next flash crash, which was inevitable. During the May 2010 flash crash, Apple shares dropped $100 in one day only to rebound sharply, and anyone who missed it vowed they wouldn’t miss another. When the flash crash happened last Monday, those waiting for it probably missed this one, too, simply because they were more shocked by (and paying attention to) the dramatic decline leading up to the open.

This flash crash was very different from the one that occurred in 2010. During the 2010 flash crash, the Dow plunged nearly 1,000 points and lasted for an hour (but it seemed like a lifetime). The flash crash on Monday passed very quickly – it lasted about 30 minutes. During that time, bid/ask spreads were wider than an 18 wheeler; one quote I saw for Skyworks Solutions (SWKS) had a bid/ask spread of 70 x 82 (the stock closed the prior day at 82).

Clearly nobody could have (or should have) traded this name, but a stock that trades several million shares a day with a huge float should not be showing this spread to a potential customer. Even Apple, the biggest and most liquid name of all, had wide spreads at the open. It’s outrageous that in 2015 a system problem such as this can even happen at all.

I don’t know who is to blame for the locked system. It could just have been overloaded – selling on futures was so voluminous and intense it got locked down just before the opening (futures were down 5% before trading was halted). This was clearly a crash fueled by selling in a totally confused, frightened and unprepared market. While the markets did recover some losses by the end of the week, the real damage was already done – to investor confidence.

Before the terrifying crash (believe me, if you were long, it was quite scary), mutual fund outflows were at 17.6 billion, the highest level since 2014. On August 25, it rose to a staggering 19 billion, the highest daily amount since 2007 (see here). While some would say this data is too late to be of any help, it is still important information to have, as money flows into funds feed liquidity and drive prices higher.

Post-crash, volatility picked up considerably. The VIX hit 53, a number not seen since the early days of the global financial crisis in 2008. I’m sure that brought back horrible memories for everyone, including the Fed. New York Fed President Dudley (a Goldman Sachs alum) even said he is less confident about a September rate hike, a comment that seemed to spur heavy buying on Wednesday that followed through to Thursday. Just a month ago, Dudley seemed ready to hike rates. Is this a sign of things to come? Perhaps, as the confidence shored up the by Fed via six years of easy money is suddenly challenged.

After the 2010 flash crash, recovery was fast but the low was tested again within three months. To a long term investor, these “mistakes” are great buying opportunities – if the chance to buy is there. On a long term chart, these drops are just a blip on the screen, but for those trading in shorter time frames, the volatility and uncertainty can easily rattle one’s nerves.