The Fuse

Futures are down slightly after a moderately down overnight session. The ES futures are still clinging to 4200 as the moving averages catchu up to price. We still find only a few names are carrying the indices (mostly Nasdaq), but perhaps some better breadth and participation is upon us.

Interest Rates are falling on the long end of the curve as we continue to see the term structure flatten out on that end of the spectrum. However, the inversion is quite steep from the Fed funds to the 2, 5, 10 and 20 year yield, which is portraying recession on the horizon.

Apple was hit with a downgrade this morning, Meta was fined 1.3 billion on the EU for data privacy violations and Micron is being banned in China as a supplier to big Chinese firms.

We’ll hear from pandemic name Zoom later tonight along with Lowes, Dick’s and BJ’s in the am. It’s part two of retailers’ earnings week.

Some big earnings coming up this week including NVDA, SNOW, COST, MRVL,LOW, DKS and ZM. All eyes/ears again this coming week on Washington and the debt ceiling discussions.

Breadth was weak on Friday but only managed to show a slight negative. We have a pre-holiday week coming up and that means some erratic price action and choppy markets. History is on the side of the bulls, this week is normally higher.

Volume trends are weakening for the moment. A recent surge in volume and price action got our attention, but no doubt some backing and filling is necessary to reset the market conditions.

Still seeing strong support below at 4100 and then 4050 on the SPX 500. For the Nasdaq 100, the clear support level is now 13.3K, which was finally exceeded and confirmed over a week ago.

The Internals

What’s it mean?

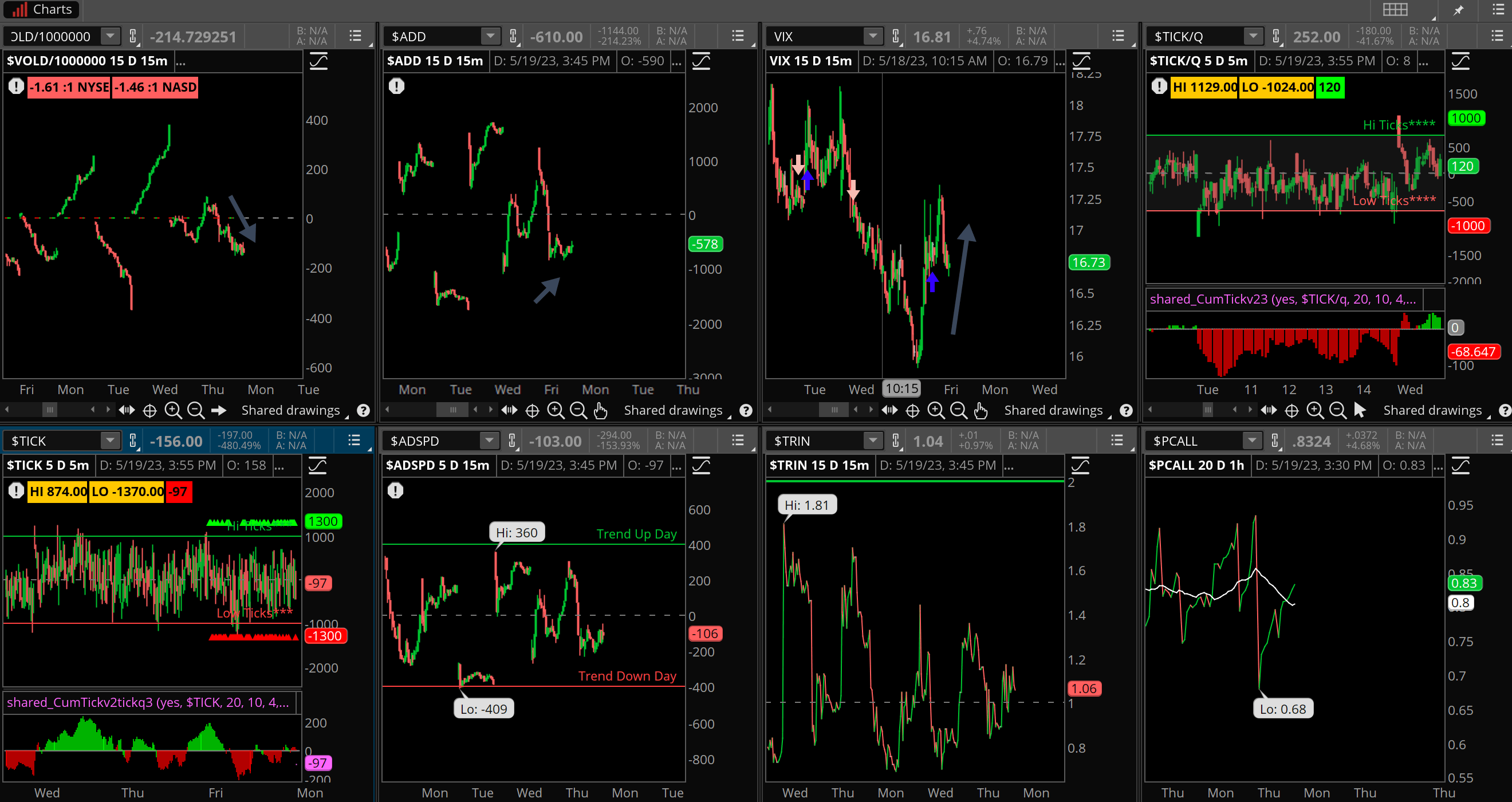

Not much to write home about. Notice the weakness in the VOLD and ADD, which tells us issues were not bullish. The VIX pushed higher into the close as being under 16% was just too tempting for the volatility bulls to pass up. Put/call remains low and may be rolling over here, which would be a bullish sign.

The Dynamite

Economic Data:

- Monday:

- Tuesday: Global Flash Manufacturing and Services PMI, New Home Sales April

- Wednesday: Mortgage applications, crude oil inventories

- Thursday: GDP second estimate, jobless claims, pending home sales

- Friday: PCE for April, Durable goods, Michigan sentiment

Earnings this week:

- Monday: NDSN, ZM

- Tuesday: AZO, BJ, DKS, LOW, WSM, A, PANW, URBN VFC

- Wednesday: ANF, ADI, DY, KSS, AEO, ELF GES, NVDA, SPLK

- Thursday: BBY, BURL, DLTR, RL, COST, DECK, GPS, ULTA, MRVL, VMW

- Friday: BIG, BAH, BKE, HIBB

Fed Watch:

Several speakers out this past week mentioned they were not done raising rates. Then on Friday, Chair Powell states that maybe we need to look at the data first before deciding what the next move is for monetary policy. A good way to shake it up.

Stocks to Watch

NVIDIA – This stock is up strong in 2023 on hype and promise with AI. They will deliver earnings on Wednesday, we’ll see if it is a sell the news event.

Washington DC – Those dreaded debt ceiling talks continue as we march toward a hard deadline.

Volatility – In front of a holiday week, we often see volatility get smashed down by the end of the week.