The Fuse

Equity futures are mixed this morning as market volatility is rising a bit from the overnight session. We could see a bit of sideways action here in over the next few days before the big tech earnings are delivered.

Interest Rates are slightly lower today as a push down from last week’s inflation numbers are inspiring bond traders to add positions. The inverted yield curve continues to narrow.

China growth estimates were cut by wall street today after some poor releases of late. Yet, we always have to be aware of potential stimulus packages from China, which may be inflationary but the country will do anything to push growth.

Plenty of earnings out this week. Tomorrow am we will have BAC, SCHW, LMT, NVS and PNC among others. After the close we’ll hear from IBKR, AAR, and a few regional banks.

Stocks moved higher again this past week but the SPX may stall out here above 4,500. That was a huge milestone but not all that surprising.

Stocks have been strong for weeks and money is starting to come off the sidelines into equities.

This week was all about strong breadth. Solid number all week, save for Friday as buyers were exhausted. We are on the cusp of a new all time high for breadth/volume, so that often leads to a new high in the SPX 500.

Volume trends have been solid this week too, with good turnover on most of the up sessions. Buyers are clearly coming into the market right now, but as we push into a big earnings season there might be a ‘sell the news effect’ soon.

With the markets breaking out we still have to remember they can go down, too. We could see a level below 4,400 tested in a corrective period, 4,330 remains stickier. The Nasdaq has 15K as a strong support level.

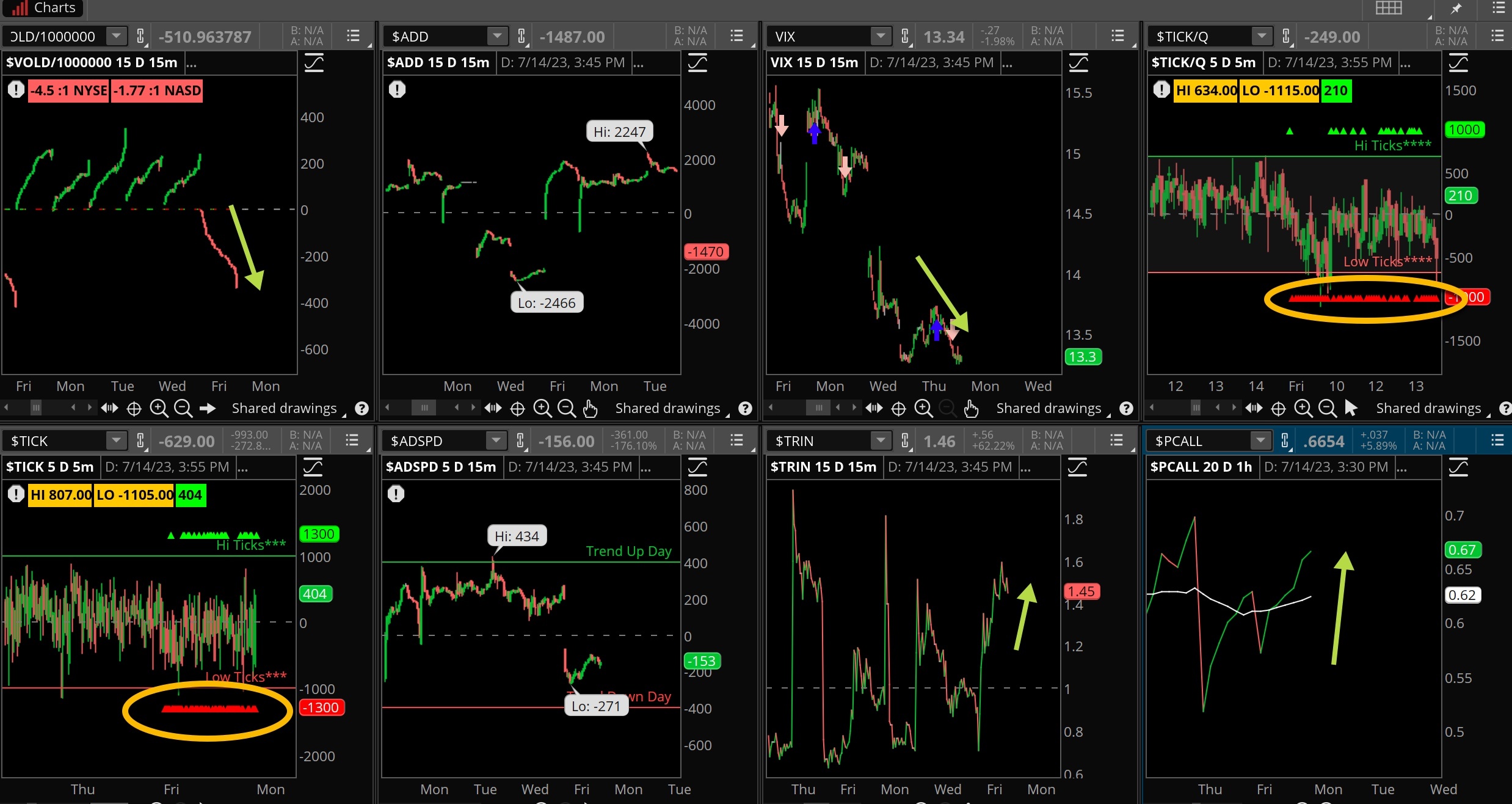

The Internals

What’s it mean?

It’s hard to keep a strong market down, but that is what happened Friday. The string of green from the VOLD ended as breadth was poor, thanks to the IWM. Ticks were concentrated in red as well, the VIX fell sharply again and remains at a critically low level. Put/calls actually rose a bit Friday as nervous investors pick up some cheap protection.

The Dynamite

Economic Data:

- Monday: Empire State Manufacturing

- Tuesday: Retail Sales, industrial production, business inventories

- Wednesday: Housing Starts, mortgage apps

- Thursday: Jobless claims, philly fed index, leading indicators, home sales

- Friday:

Earnings this week:

- Monday: ELS

- Tuesday: BAC, SCHW, LMT, BK, SYF, IBKR, JBHT

- Wednesday: ASML, ELV, GS, AA, CCI, DFS, IBM, NFLX, TSLA, UAL

- Thursday: AAL, DHI, JNJ, NOK, TSM, CSX, PPG, VMI

- Friday: AXP, AN

Fed Watch:

Fed speakers will be quiet this week in front of the next FOMC meeting. Current odds favor a rate hike at the next meeting but certainly the cooler inflation may offer the committee yet another opportunity to pause. So many hikes in the system seem to be working their magic, and if the economy holds up strong we’ll see rate cuts coming in 2024.

Stocks to Watch

Earnings – Companies will start reporting their quarter this week, a bigger list of names henceforth. We are getting a sampling of tech earnings and other groups this coming week.

Volatility – VIX remains very low and as we have preached in prior weeks, it is dangerously low. That said, until a change in character is seen there is no reason to fight the trend.

Tesla – the big EV car company reports on Wednesday evening, it is always entertaining to hear Elon Musk on the call and how well the company is doing.