FREE WEBINAR TODAY – DON’T MISS IT, AFTER THE CLOSE AT 430PM EST, Mish Schneider joining me as we jump around different market topics. Use this link to register!

The Fuse

Futures are modestly higher this morning in a continuation from yesterday’s sharp move up from the lows. With CPI out tomorrow morning it makes sense to take some risk off the table, we should see that happen today.

The markets are still consolidating recent gains. The Russell 2K was impressive on Monday, rising up more than 1% but with lousy volume.

The price action though was positive all session long, and helped turn the other indices around.

Not much new overnight but interest rates on the short end of the curve continue to rise, sparking fear the Fed is truly seriously about raising rates further than anyone believes. Tomorrow’s CPI and Thursday’s PPI will tell us plenty about the Fed’s motivation from a market perspective. Currently, the markets believe the Fed is about finished raising short term rates and will have to cut very fast, very soon.

Carmax this morning delivered earnings that beat reduced estimates but were down sharply from a year ago. The company re-affirmed guidance for 2023.

This week starts off earning season, but we’ll be watching inflation data carefully along with the release of last month’s FOMC meeting minutes.

Breadth was good all day, thanks to the strong Russell 2K. This index can carry the markets with good or bad breadth. Today’s nearly 2-1 positive was a welcomed sign after the indices started off slow.

Volume trends are improving. Yesterday’s turnover was constructive and positive, and with some news coming out there could be some followthrough.

We see 4100 on the SPX 500 as good support once again, below there is 4090 and 4050 then 4000. For the Nasdaq, it’s 13K of course, with some levels below there if that falls (12500 and then 12K).

The Internals

What’s it mean?

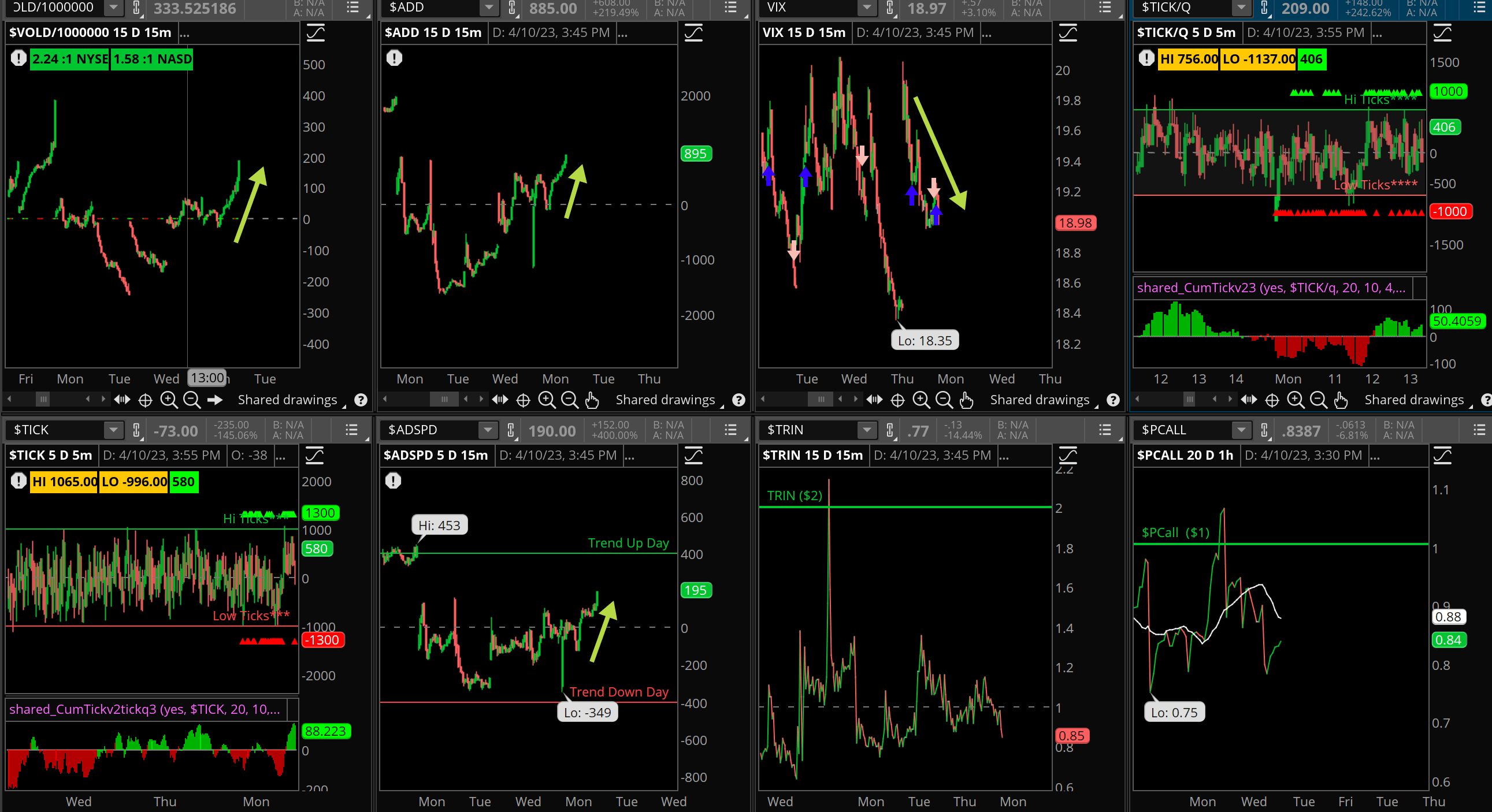

Let’s call Monday a day of improvement. Starting in the hole, we saw the VOLD and ADD spurt higher all session long. Put/calls headed lower which was bullish for the markets, while VIX started high and finished just off the lows, where volatility sellers were active. Today might bring some followthrough.

The Dynamite

Economic Data:

- Tuesday: Small Biz optimism index

- Wednesday: CPI, FOMC minutes, Atlant Fed Biz Inflation expectations

- Thursday: PPI, jobless claims

- Friday: Retail sales, industrial production, biz inventories, consumer sentiment

Earnings this week:

- Tuesday: KMX, ABS

- Wednesday: RENT, LVMH

- Thursday: DAL, FAST, INFS

- Friday: JPM, UNH, PNC, C, WFC, BLK

Fed Watch: NY Fed President Williams out saying rates need to stay higher for longer. Two other Fed speakers this week, Austan Goolsbee on Tuesday and Tom Barkin Wednesday. We don’t expect fireworks from these speakers though a response to last week’s job data is likely.

Issues/Stocks to Watch this week

Banks – JPM, C, WFC, BLK kick off the ‘real’ start of earnings.

Gold, Silver – After a strong couple weeks, seeing if key levels of support hold.

Inflation data – With CPI, PPI out midweek, will these start to materially turn down or force the Fed to hike more.