The Fuse

Equity futures are soft this morning following a strong finish on Monday, where we saw the indices shoot higher in the last 10 minutes of trading. This was probably due to some window dressing action at the end of the month, funds try to show bigger positioning at the end of a period. The new month of August starts here today and after a very strong five months, we would not be surprised to see markets backing off some, perhaps starting in a week.

Interest Rates are edging higher as investors position themselves for the start of the new month and the heavy dose of jobs data to come this week. A risk off session would not be a surprise here after the bulls chased equity markets higher this past month.

Euro stocks are lower following in line PMI data, China stocks are modestly lower but in Japan equities are higher. Crude oil is slightly lower after a very strong month for the commodity, gold and silver are down more than 1% each.

Solid earnings this morning from MRK, UBER and CAT. Not just beating expectations but also raising guidance, which has become a theme this earnings season. More big releases tonight and later in the week.

Earnings this week include Apple and Amazon, and many will be watching those. But it’s all about the jobs report this week and if the economy continues to float along and test the soft landing scenario.

Markets were a bit timid out of the gate Monday but managed to finish with a respectable gain. Breadth was positive, this indicator is once again on a buy signal.

Volume trends were not too positive on this last trading day of the month, but we could see that start to change later this week. Yet, we have historical evidence that August is a month of low volume and higher volatility, so look for range expansion.

The 4600 level on the SPX 500 remains in reach, only 12 points away until we can count it. Nasdaq and Russell 2K may be the key players in determining the next direction. With the monthly MACD crossover in July, a confirmation month now would cinch a bull market has arrived.

The Internals

What’s it mean?

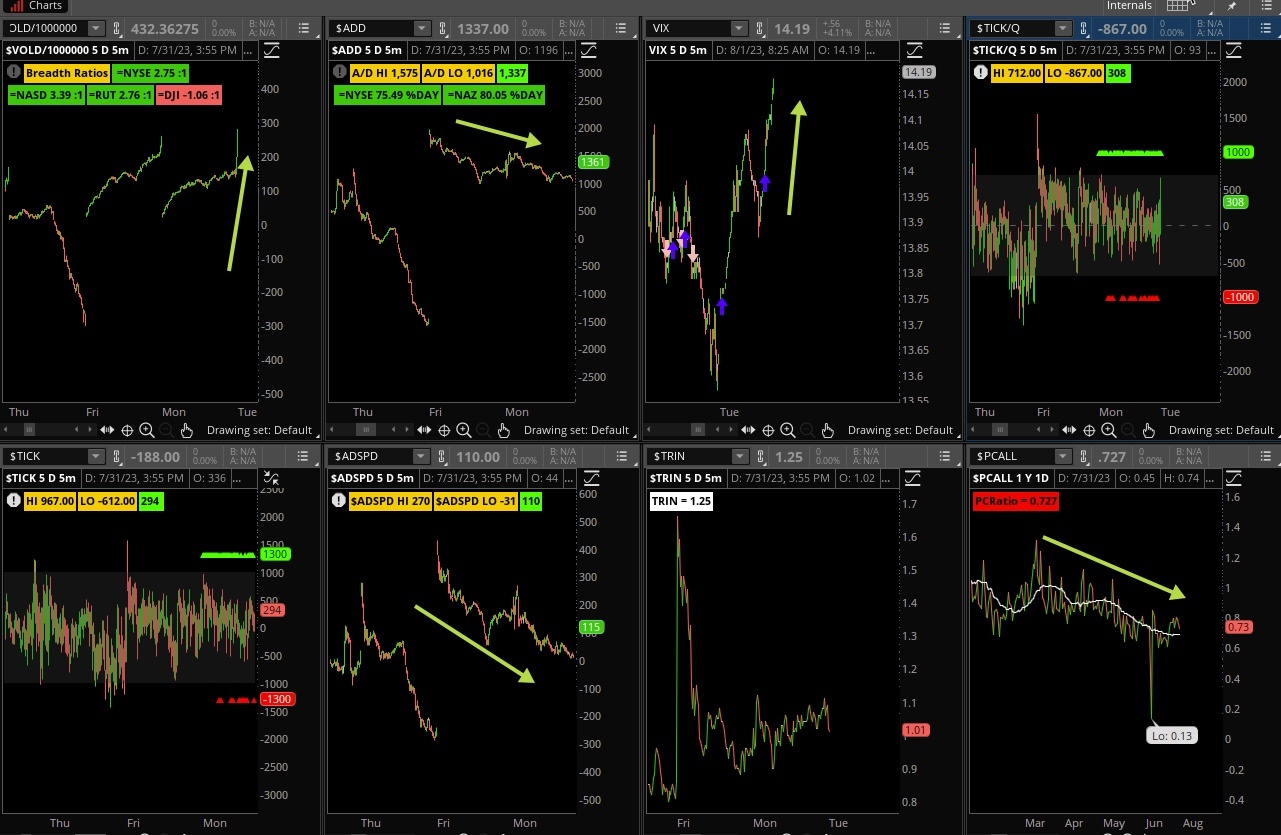

The internals took on strange behavior, it appeared a nasty close was going to occur until a big buy program hit in the last 10 minutes of the day to push indices higher. We can see a divergence between VOLD and ADD, while the VIX shot up to end the day on its highs. ADSPD was also down and the put/call pushed lower, the bears just cannot catch a break!.

The Dynamite

Economic Data:

- Tuesday: global PMI, ISM manufacturing, construction spending, JOLTS report

- Wednesday: ADP report, weekly crude report

- Thursday: Productivity and unit labor costs, global services PMI, ISM non-manufacturing, Factory orders

- Friday: non-farm payroll report

Earnings this week:

- Tuesday: MO, CAT, ETN, ITW, MAR, TAP, UBER, AMD, CZR, ELF, MOS, PINS, SBUX, VFC

- Wednesday: BLDR, YOU, CVX, DD, EMR, RACE, YUM, CF, CAKE DASH, EVGO, FSLY MGM, PYPL, QRVO, QCOM, SHOP, ZG

- Thursday: BUD, GOOS, CMI, PZZA, SHAK, VMC, AMZN, AAPL, SQ, NET, POST, DBX, FTNT, WW

- Friday:AMC, CBOE, PRLB

Fed Watch:

Last week’s Fed meeting seemed ho-hum to many but to use there was a message sent, and that was the committee was trying to pivot slowly, out loud. Of course, nobody heard it that way to feel confident about that call, but we believe the Fed may consider a pause or a hike over the next few meetings. Any hike that does come is likely to be the last one. We’ll have some speakers out this week talking about the economy. While inflation remains too high for their liking, they are still very pleased to see prices starting to come down due to their efforts.

Stocks to Watch

Apple – the largest company in the world will report earnings this week, the stock has added more than 1 trillion dollars in value this year. We don’t expect a disappointment but rather news about upcoming products and production concerns.

Jobs – Friday’s big employment report will give us a glimpse of how the economy has started off in the second half of 2023. So far so good and if productivity is strong the day before, the Fed will be very pleased with their hawkish campaign.

Interest Rates – Last week saw rates climb above 4% on the 10 year for a brief moment, enough to scare stock investors. We’ll be watching for more ‘scaring’ this week, if it materializes.