The Fuse

Equity futures are modestly higher this morning as the market prepares for the Fed’s new policy meeting concluding tomorrow. Stocks are at their highest levels since March 2022 and are looking to build more momentum into the end of the year. But it will take some heavy lifting if the big FANG+ names are not involved, as they chose not to participate in yesterday’s rally.

Interest Rates are down this morning as bond traders start scooping up fixed income. The inflation reports this week will be important for bond holders, if prices are still higher we could see bonds falling sharply from recent levels and yields climbing once again.

Only 13 more days until the Christmas holiday but a short 9 days of trading before the market takes a break. Stocks have been resilient this month, very impressive following the strength we saw in November. The Federal Reserve meeting starts today, the committee may contemplate a timeline for when it is appropriate to start cutting interest rates.

Earnings from Oracle last night were a bust. The company barely beat but offered horrendous guidance. Tomorrow we hear from Adobe Systems, a big tech name with some influence.

Bonds are on the rise as the dollar fails to catch a bid as equity traders await the CPI and PPI numbers for November. The Fed starts its 2 day meeting today, the last one of 2023 and it is widely expected they will leave fed funds rate alone. European stocks were steady, some countries’ exchanges are near all time high levels. gold is up nearly .5% while crude oil is down modestly. The yen rebounded in overnight trading while bitcoin also mounted a nice rally following a very weak session Monday.

Due to the weakness of the IWM (up slightly) breadth came in weaker than expected. But still, the indices were higher on this day and in front of an important inflation report, the CPI today and the PPI tomorrow. If taken well we could see more upside, the oscillators are not overbought yet.

Chalk up another accumulation day for the Dow industrials (DIA), but strong turnover for the other indices, too. The bulls like to see good, solid volume and expanding breadth, though we had the former on Monday we could see breadth expand later in the week. Seasonal trends are bullish and moving through resistance like the indices have done recently is only going to bring in more buying volume.

The SPX 500 finally finished above the 4,600 level for the first time in months. We need some confirmation though, and that would require another day above there. For support we still see 4,450 and 4,500 as levels where the markets could travel and bounce from.

What’s it mean?

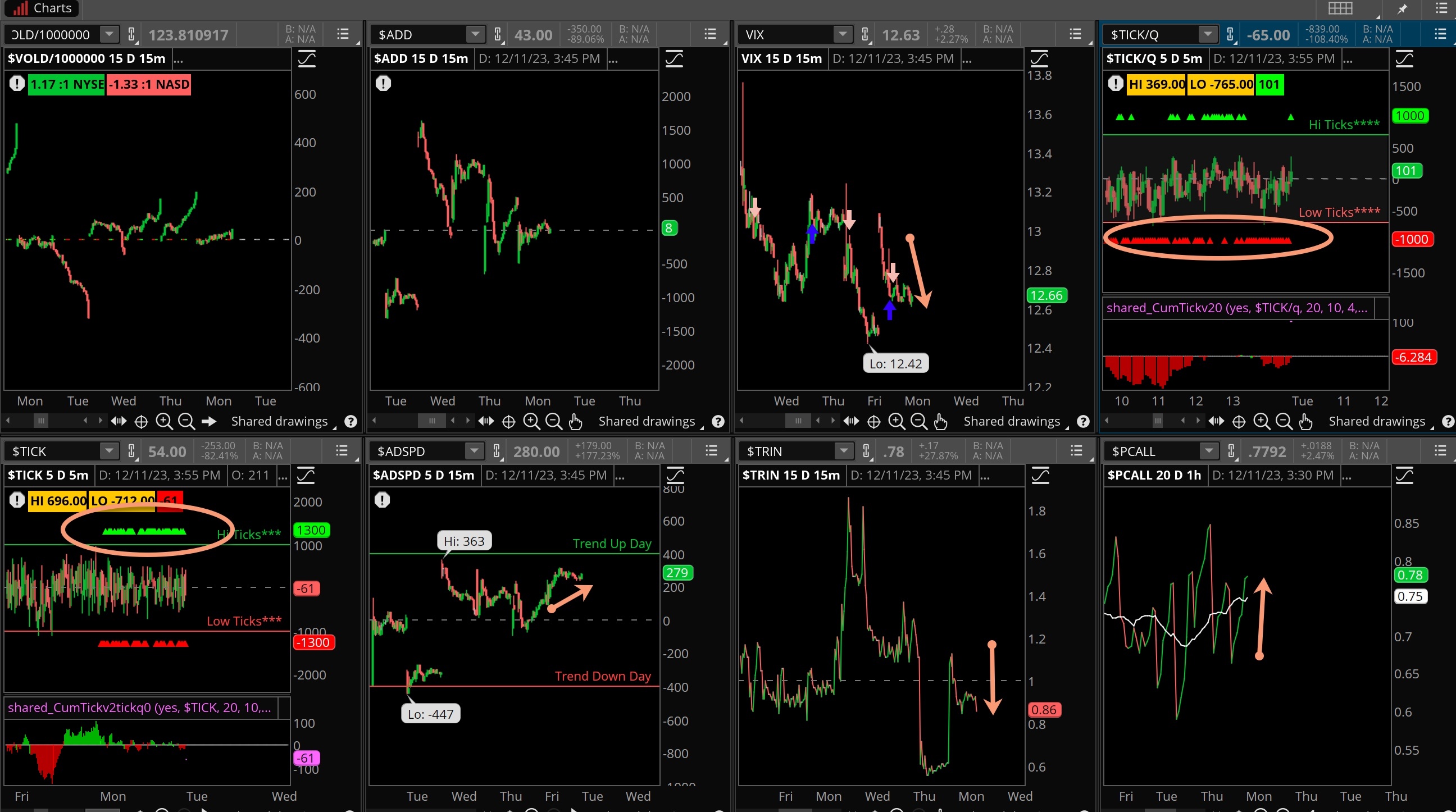

It was an odd day according to the internals. Not only did the VOLD and ADD not advance much, but the VIX barely budged on a day when the indices started to make a strong move higher. Put/calls ran up, apparently investors looking to buy some protection, the ADSPD was up but again the VOLD, which ties into this one was much higher. Ticks were mixed, NYSE TICKS strong while Nasdaq TICKS weaker most of the day. Today is an important day for the market and internals to get back on track.

The Dynamite

Economic Data:

- Tuesday: Small Business Optimism, CPI, treasury budget

- Wednesday: PPI, mortgage apps, FOMC decision/press conference

- Thursday: Jobless claims, retail sales, biz inventories, import/ex prices

- Friday: Empire Manufacturing Index, IP and cap utilization, S&P Global PMI

Earnings this week:

- Tuesday: JCI

- Wednesday: REVG, ADBE, NDSN

- Thursday: COST, LEN, REGN

- Friday: DRI

Fed Watch:

It’s the last Federal Reserve meeting of the year and markets are not expecting rates to move at all. We will have some projection materials this week from the committee along with another press conference from Chair Powell. In all likelihood the committee will be far more reserved than what the market wants, and that could be considered a disappointment. Look for quite a bit of volatility before and after the meeting.

Stocks to Watch

Federal Reserve – This is the last meeting of 2023 and the hope is the committee is more likely to end rate hikes in 2024. No hike or cut is expected this week.

Interest Rates – They say the bond market has been doing the Fed’s job. Yet, the market is now pricing in five 1/4 point rate cuts in 2024. They may be way ahead of themselves and the Chairman may throw some cold water their way.

Retailers – We are only a couple of weeks from the Christmas holiday and shoppers remain active. But as the time gets near supplies run short and stock (inventory) is hard to come by. So far it seems to be a solid shopping season.