The Fuse

Stock futures are bouncing back this morning after a nasty spill late yesterday. The blame was given to options-related action and short-term style calls/puts. That weighed heavily on the indices but the bulls are trying to wrest the ball back onto their court.

Interest Rates are mostly steady but slightly higher as we continue to see inversion across the curve. The 10 year has now spent five. days below it’s 200 day moving average, which is right at 4.03%. This tells us the trend is downward in rates even if it is a slow drip. Next up appears to be 3.7% on the 10 year, but that might take some time.

Stocks took it on the chin yesterday as there was a massive downside candle formed from the days action. On the worst day since October 26, we saw big distribution day occur, many saying it was options-related. It was bearish of course, but there is a chance to rehabilitate over the next couple of days, we’ll see if the bulls have the energy before the xmas holiday break. Crude oil and gold are slightly lower this morning. GDP Q3 will be updated one more time today while the important PCE comes out tomorrow morning.

Strong earnings and guidance from Micron last night has that stock and the semi group catching a bid this morning. Carmax is up in early trading as that name showed good earnings this morning but sales declined.

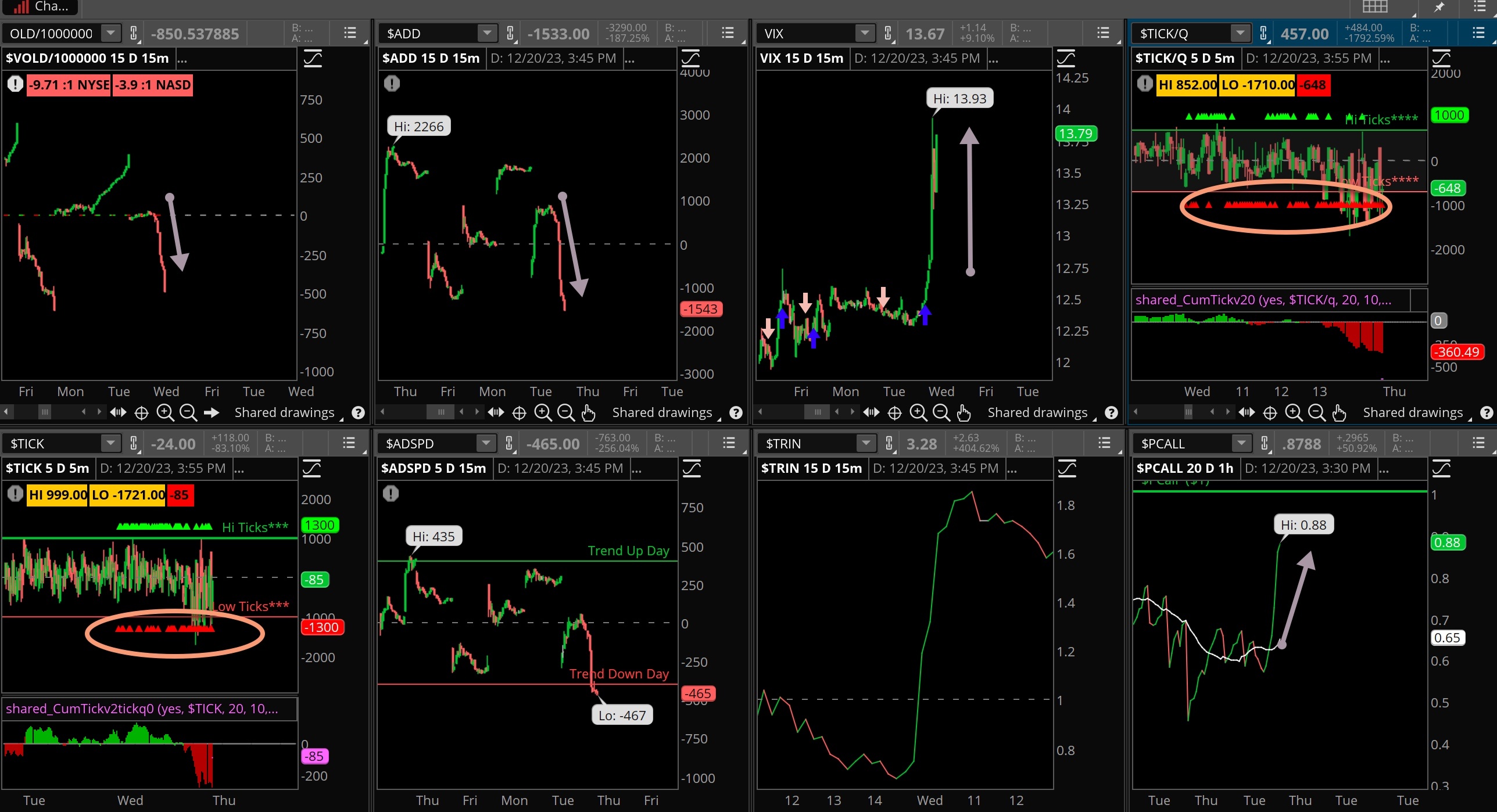

Stocks were under pressure early in the day but the heavy selling did not really begin until a slew of sell programs hit the tap consecutive after 2pm EST. It was an avalanche of sells and no buyers to be found, something we have not gotten used to over the last six weeks or so. Still, markets are up strong for the month and are still looking for some upside to finish the year strong.

Breadth was weak as could be expected all day long but really finished poorly at the end of the day. A 5-1 bearish skew was the result of this bearish action, the first real down day since the start of the month. Seasonal trends are still bullish but after such a tremendous run higher there could be more downside.

Heavy volume prints today as the markets just could not ignore the news of poor FDX earnings and potential for a slowing economy. Buying has been rampant this month but was pretty week, and remember if stocks are not going up, they are likely to go down. Chalk up one distribution day, the first one in a few weeks. Nothing to worry about until we see 2-4 more of those.

As hard as the markets tried to tag a new high it just wasn’t meant to be for the SPX 500. Stocks were leveled after 2pm EST in a concerted effort to bring prices lower. Support below at 4650 and then 4600 should hold, but volatility is starting to kick up.

The Internals

What’s it mean?

The mirror image of Tuesday’s very strong internals. Wednesday was atrocious but it really did not seem to get bad until 2pm EST when an avalanche of selling hit the markets. Breadth was horrendous as mentioned above, the VOLD straight down as was the ADD. VIX climbed as well, up about 8% but check out put/call, which was sharply higher. Clearly investors were looking for protection in cheap puts, and they found it. TICKS were especially red, too.

The Dynamite

Economic Data:

- Thursday: Jobless claims, GDP 3rd Q Estimate, Philly Fed, Leading Indicators

- Friday: PCE, Durable Goods, Michigan Sentiment, New Home Sales

Earnings this week:

- Thursday: NKE, KMX, CTAS, PAYX, AVO, AAR, CCL

- Friday: N/A

Fed Watch:

Some Fed talk on Friday caused many to take money off the table but the Chairman’s words Wednesday were pretty definitive. The committee kept rates in check and stated there was ‘talk’ of a time line for rate cuts. That spurred a slew of buying in stocks and yields fell sharply, the 10 year is now below 4% for the first time since August and its lowest levels since July. Truly amazing move lower but we may be at the far end of the move now. The inversion of the curve is extreme.

Stocks to Watch

Volatility – The VIX remains low, hovering near 12% and could even break LOWER this week by Friday (holiday coming up, volatility sellers are active).

Small Caps – The Russell 2K has been on fire lately, with yields falling sharply that means small cap names are getting heavy money flows. If rates don’t rise then the Russell 2K may finish the year strong.

Retail Sales – Last week’s report was pretty good but this is the last full week for shoppers to get ahead of Santa. Can the consumer pull it off once more?