The Fuse

Equity futures are a bit soft this morning following a massive surge to start the new month. Volume and breadth were very good Friday with prices pushing up towards important resistance. However, oscillators are pretty well overbought here so a pullback should not be a surprise.

Interest Rates on the long end of the curve are modestly lower as investors/traders ready for the last Fed meeting of the year next week.

Some investors are not doubting rate cuts are coming very soon.

Gold and bitcoin surged higher overbought with the latter pushing above 40K for the first time in months. The former hit an all time high at 2,150 per ounce overnight but has backed off, still the highest level reached was impressive. Chair Powell gave the same line Friday about being vigilant on inflation, and fed speakers were beating the same drum.

Some big earnings later in the week including RH, LULU,, AVGO, VEEV, MDB and OLLI. Retail remains in the spotlight.

Another solid day for the markets as the SPX 500 is within reach of the elusive 4,600 level. The problem here is an overbought condition that may need a corrective measure or pullback. Volatility is nowhere to be found, and following a couple of comments from Chair Powell the market is simply not believing in more rate hikes, and in fact is heavily pricing in rate cuts in 2024, at least three of them. As always, the data will matter most.

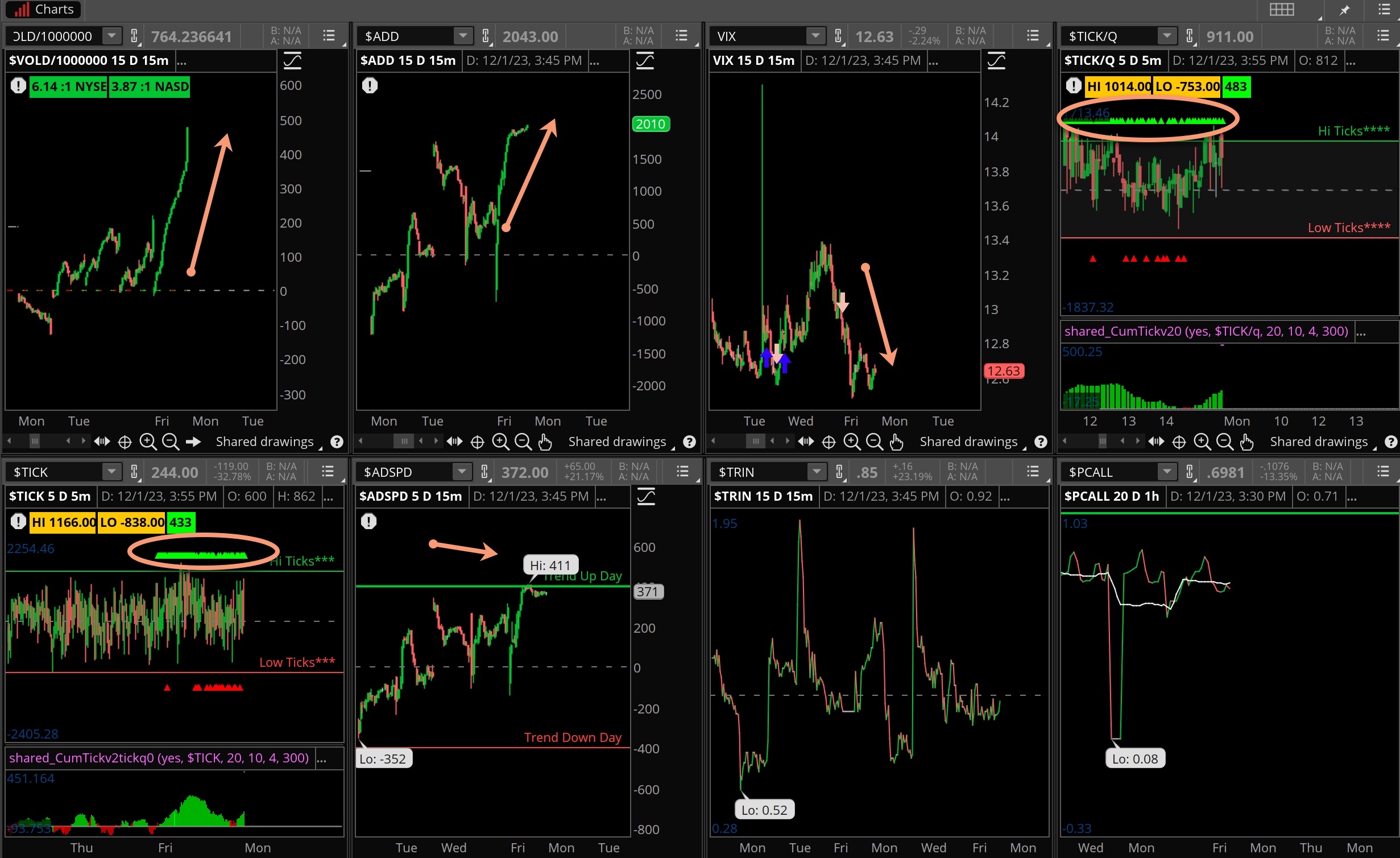

Friday was a tremendous breadth day, more than 6-1 on the positive side as the bulls regained control. It’s impressive to see this strong breadth as the markets rise up towards strong resistance, it simply means buyers are interested at these high prices. So be it! New highs are expanding on the NYSE and Nasdaq, and Friday’s Naz level was the highest since August.

SPY and DIA volume stood out but so did the Russell 2K, which broke out on a massive turnover. It was an impressive move as buyers started to finally come after small cap stocks. This was a main reason for the higher breadth noted above, which is driven by 2000 stocks rather than 500 or 30.

The 4,600 level is close to being breached, we need to watch this closely as a confirmation above will solidify the move and set the stage for higher prices for the remainder of the year. Next level of resistance would be old highs at 4,818 with support at 4,500.

The Internals

What’s it mean?

Incredibly strong day for the internals. Notice the VOLD just straight up, reflecting the strong volume and skew of good breadth. It was a trend up day for the ADSPD, volatility down while the ticks were concentrated bullish. Put/calls were not a factor. We could see some followthrough on Monday here as well but perhaps a stall later in the week.

The Dynamite

Economic Data:

- Monday: Factory Orders

- Tuesday: Global PMI final, ISM, JOLTS

- Wednesday: ADP employment change, productivity/labor costs

- Thursday: Challenger job cuts, jobless claims, wholesale inventories, consumer credit

- Friday: Job report for November, Michigan sentiment index

Earnings this week:

- Monday: SAIC, GITB

- Tuesday: SIG, AZO, BOX, PLAY, S, TOL, MDB

- Wednesday: CPB, OLLI, UNI, GME, CHWY, VEEV, NAPA

- Thursday: CIEN, DG, GMS, AVGO, LULU, DOCU, RH, MTN

- Friday: JOUT

Fed Watch:

Chair Powell spoke a couple of times last week indicating the committee is still an inflation fighter. The market believes their work is down and it’s just about time for rate cuts. We’re not sure that’s the case yet but some fed speakers this past week indicated the hikes were probably done for now. Of course, we will watch the data as will the committee, the last meeting of the year comes in about 11 days.

Stocks to Watch

SPX 500 – We are close to breaking through big resistance at 4,600 and if that happens the SPX 500 is on its way to the old highs from 2022.

VIX – The volatility index remains low, probably too low but that doesn’t matter when traders are not buying protection and want stocks.

Eventually it’s going to matter as market players are conditioned for markets only going up. It’s time to be alert.

Employment – The November jobs report is out Friday and it could be a game changer for Fed policy if inflation trends (wages) are lower than the prior month.