The Fuse

US equity futures are down moderately again this morning trying to burn off more of an extreme overbought reading from last week. Technology and Nasdaq stocks are especially weak after Monday’s more than 1% loss, but we may see some buying here before the end of the week if interest rates faill with the job reports coming out.

Interest Rates are a bit lower this morning in a ‘flight to safety’ situation. Plenty of positioning in front of next week’s Fed meeting, where they may start signaling a pause in rate hikes (officially).

News of Moody’s cut for China credit outlook to negative on rising debt. Gold and oil are mostly unchanged after a couple of volatile sessions. European equities rose modestly, the DAX up .2% and closing in on record highs, but emerging markets were lower following the China downgrade. US jobs data this week will clear up some confusion over why the markets are moving as they are currently. Seasonality and sentiment are playing a huge role along with liquidity and easier financial conditions (rates have been dropping).

Gitlab is exploding today following a very strong earnings report and guidance. A slew of earnings out this am from HOV, GIII, NIO, SIG, AZO then latery tonight from BOX, MDB, ASAN and TOL.

It was an odd session Monday, we saw big cap tech taking on the chin while the rest of the market was flourishing. The heavy-handed Nasdaq was down sharply most of the session but pared its losses a bit. Strong gains again by the Russell 2K, more than 1% spurred some buying while other markets were in distribution.

Today was ‘supposed’ to be a down day, and the breadth figures pretty much show that to be the case. While it seemed to be a tie, quite a few big cap names were distributed Monday following the amazingly strong breadth on Friday, so we’ll call it a draw. Gobs of breadth are good for the bulls.

A day of distribution for the Nasdaq as sellers took control on that index. This means Tuesday is an important day for turnover statistics.

The bulls would like some followthrough from the small caps, and of course it’s Tuesday and we always look for a turnaround session. Volume prints were good on the Dow Industrials and Russell, notably good for a consolidation day.

One more time, say it with feeling: The 4,600 level just cannot be broken yet. As we spend more time trying to push through the ceiling it becomes increasingly harder to do. If we are stuck at the top of the range then downside is quite vulnerable. For starters, 4,500, which is about 1.7% lower would be the first stop.

The Internals

What’s it mean?

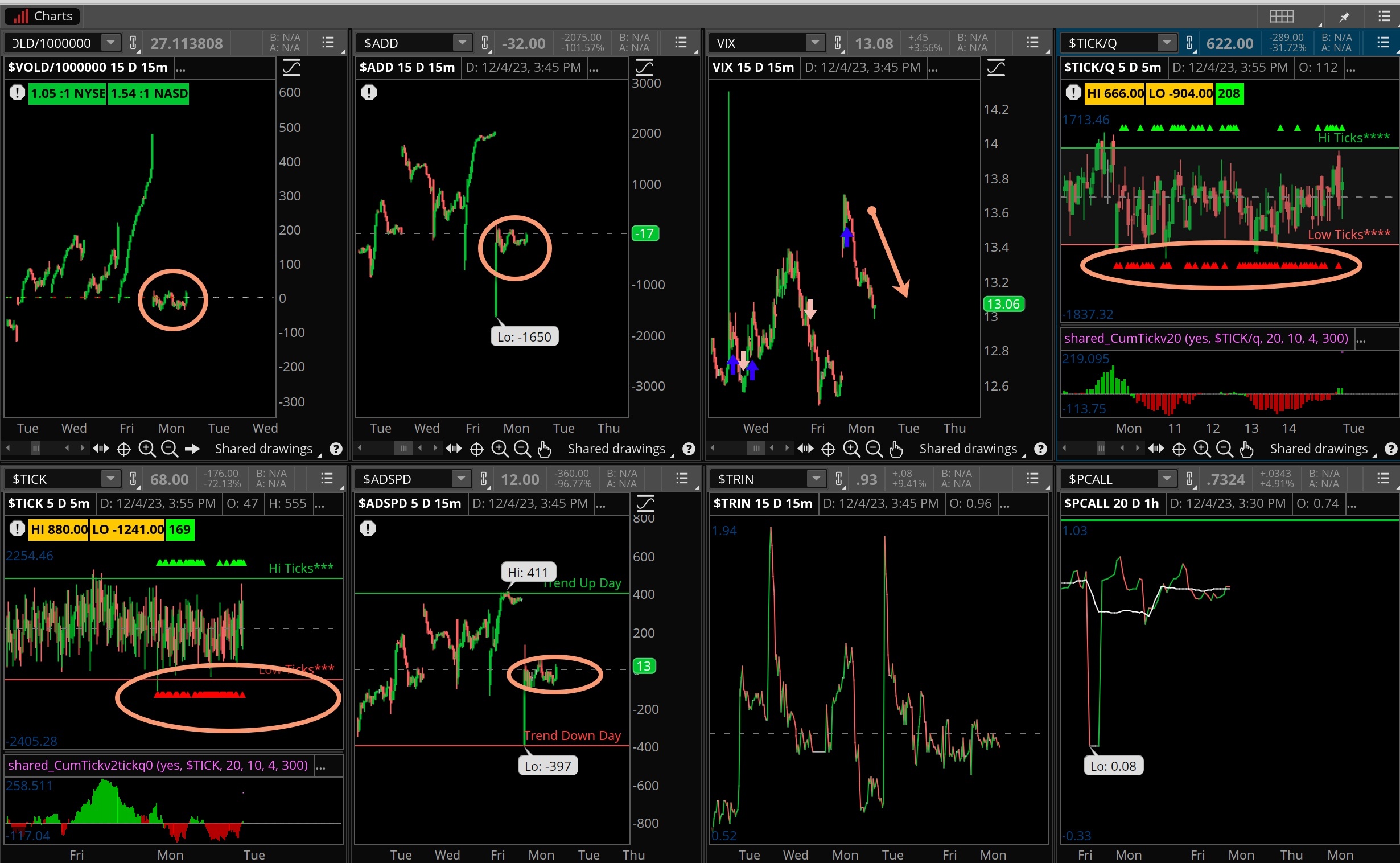

Not much movement in the VOLD on Monday, indicative of the mixed market signals. Look at the ticks, especially in the Nasdaq as the red is just the dominant color. That is plain selling, but after a couple of strong weeks we would expect it. VIX was modestly higher on the day but mostly sending a message that below 13% is not OK. ADSPD and ADD were flat as well. Maybe today will give us something better to evaluate, Monday was just a throwaway day.

The Dynamite

Economic Data:

- Tuesday: Global PMI final, ISM, JOLTS

- Wednesday: ADP employment change, productivity/labor costs

- Thursday: Challenger job cuts, jobless claims, wholesale inventories, consumer credit

- Friday: Job report for November, Michigan sentiment index

Earnings this week:

- Tuesday: SIG, AZO, BOX, PLAY, S, TOL, MDB

- Wednesday: CPB, OLLI, UNI, GME, CHWY, VEEV, NAPA

- Thursday: CIEN, DG, GMS, AVGO, LULU, DOCU, RH, MTN

- Friday: JOUT

Fed Watch:

Chair Powell spoke a couple of times last week indicating the committee is still an inflation fighter. The market believes their work is down and it’s just about time for rate cuts. We’re not sure that’s the case yet but some fed speakers this past week indicated the hikes were probably done for now. Of course, we will watch the data as will the committee, the last meeting of the year comes in about 11 days.

Stocks to Watch

SPX 500 – We are close to breaking through big resistance at 4,600 and if that happens the SPX 500 is on its way to the old highs from 2022.

VIX – The volatility index remains low, probably too low but that doesn’t matter when traders are not buying protection and want stocks.

Eventually it’s going to matter as market players are conditioned for markets only going up. It’s time to be alert.

Employment – The November jobs report is out Friday and it could be a game changer for Fed policy if inflation trends (wages) are lower than the prior month.