The Fuse

Equity futures are trickling up as the low volatility remains an issue. Overnight saw futures dip lower when Europe opened but have bounced back. Remember, when buyers are seemingly finished the sellers take over, and when support falls there is little support in this recent rally to hold stocks from dropping.

Interest Rates are higher today in front of tomorrow’s employment report. It’s hard to read to much into this as rates on the long end of the curve have dropped sharply, signaling the market is expecting quite a few rate cuts coming in 2024.

Some news overnight from Japan as the thought of their central bank scrapping their negative interest rate policy may actually happen. Japan is the last economy left with ZIRP or NIRP (zero or negative interest rate policy). The yen was up on this news, traders see markets taking a breather soon after the strong recent rally.

Earnings from Chewy, Veeva Systems and GameStop were out last night and they were poor with weak guidance. This morning DG and Ciena were out out with mixed results but their stocks are higher. Later tonight we’ll hear from LULU, AVGO, RH and DOCU.

Three days down for the SPX 500 has this index ready to test lower levels. Without so much as a blink of an eye the indices have fallen about 2% or so as turnover is starting to rise. That means distribution days, which is professional selling. We need to be on watch here for more down sessions, especially with a Fed meeting to come next week.

Breadth looked as if it was going to recover, and the Russell 2K was on its way but the buyers stopped late in the day and the selling turned nasty. We saw another negative breadth day as new lows are starting to creep higher.

Volume levels were elevated as we come close to the end of the week and the labor report. Markets could certainly use a breather after the wild November, but not many are expecting too much action. Volatility remains muted but may rise sharply at anytime. Not good to remain complacent.

As we continue to monitor key levels above we cannot forget about the support levels below. It appears the 4,500 level may be the next area of interest to the downside, the 20 day moving average is right there close by. It seems a bit too ‘neat’, markets are much sloppier.

The Internals

What’s it mean?

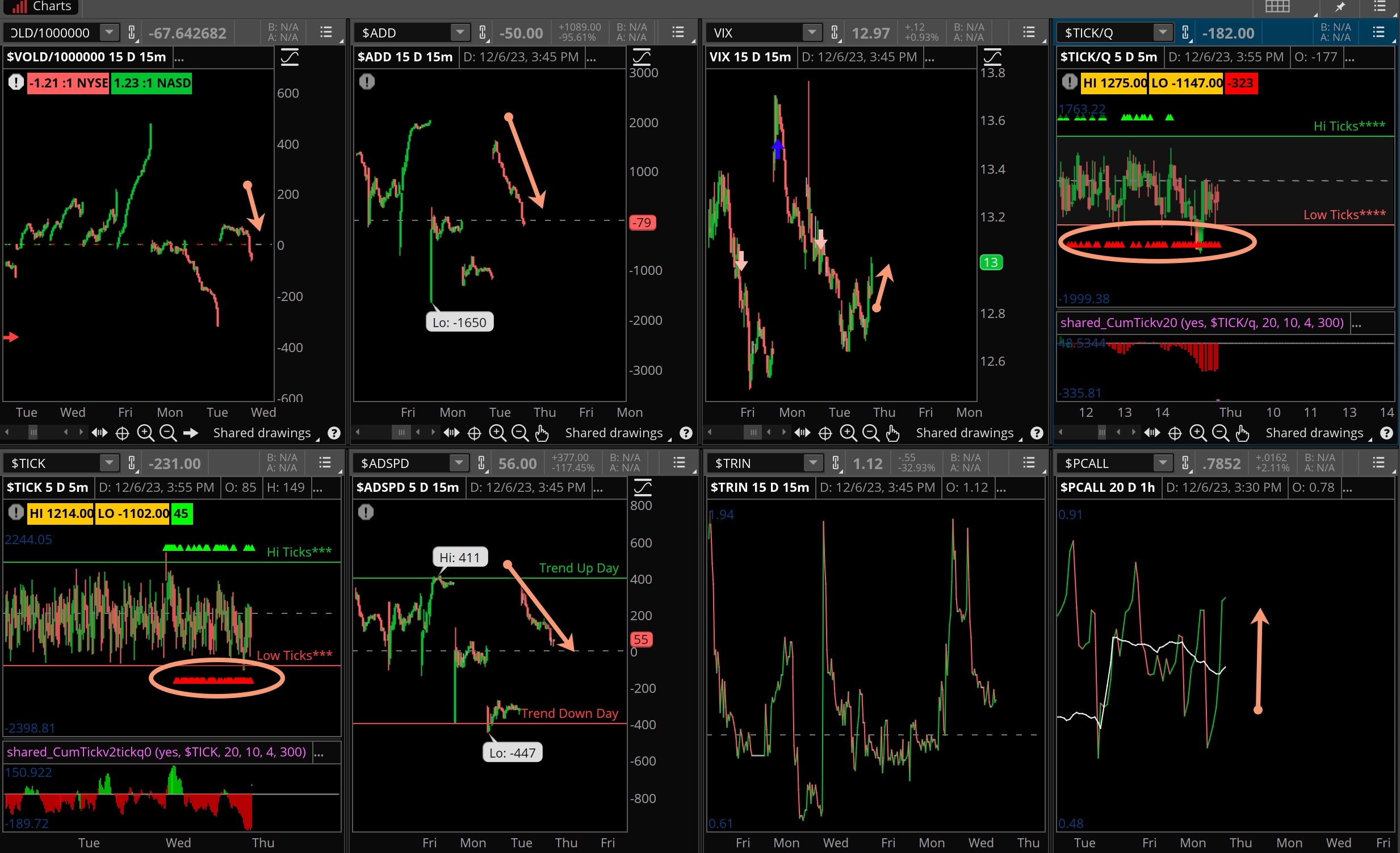

A rather dismal session for the stock market as evidenced by the internals. The VOLD was smacked around all day and the ADD was horrendous, down all session long. VIX poked its head up and closed nearly at the highs of the session, the TICKS were red most of the day as a bunch of sell programs hit from the start of trading. Not a good sign of things here if you’re bullish, but perhaps we get a respite on Friday.

The Dynamite

Economic Data:

- Thursday: Challenger job cuts, jobless claims, wholesale inventories, consumer credit

- Friday: Job report for November, Michigan sentiment index

Earnings this week:

- Thursday: CIEN, DG, GMS, AVGO, LULU, DOCU, RH, MTN

- Friday: JOUT

Fed Watch:

Chair Powell spoke a couple of times last week indicating the committee is still an inflation fighter. The market believes their work is down and it’s just about time for rate cuts. We’re not sure that’s the case yet but some fed speakers this past week indicated the hikes were probably done for now. Of course, we will watch the data as will the committee, the last meeting of the year comes in about 11 days.

Stocks to Watch

SPX 500 – We are close to breaking through big resistance at 4,600 and if that happens the SPX 500 is on its way to the old highs from 2022.

VIX – The volatility index remains low, probably too low but that doesn’t matter when traders are not buying protection and want stocks.

Eventually it’s going to matter as market players are conditioned for markets only going up. It’s time to be alert.

Employment – The November jobs report is out Friday and it could be a game changer for Fed policy if inflation trends (wages) are lower than the prior month.