The Fuse

Equity futures are modestly higher today as traders await the big CPI number due out this morning. Overnight the market has been well bid and regardless of the number the stock market could continue its rise. Traders may be seeing some opportunity to push the SPX 500 to 4,500 this week.

Interest Rates continue a gradual descent from high levels reached last week. A bit lower and we’ll have seen the double top formed on the 10 and 2 year yields. Lower rates would be a positive for tech and the Nasdaq stocks.

CPI is due out this morning and many are looking for lower numbers in the core, approaching 3%. That is still to hot for the Fed’s taste, so a July rate hike is still on the table. Plenty of more data will be released in the days ahead that will help the committee craft its policy.

Pepsi later in the week along with United Health,Delta and Cintas, then banks start reporting – Wells Fargo, JP Morgan, Citi, Blackrock, State Street.

A handful of Fed speakers out this week as they try and explain policy in the current economic environment.

Another solid day of breadth as this key indicator remains on a buy signal. Gobs of breadth is a good sign for continuation, and the Russell 2K is leading the parade.

Volume is starting to pick up once again as the bulls take the lead. Oscillators are now on buy signals and are near overbought.

Pushing back above 4,400 today was a good sign and closing above that level this Friday would have us upgrade the rally. So far, lower levels of support have held in nicely.

The Internals

What’s it mean?

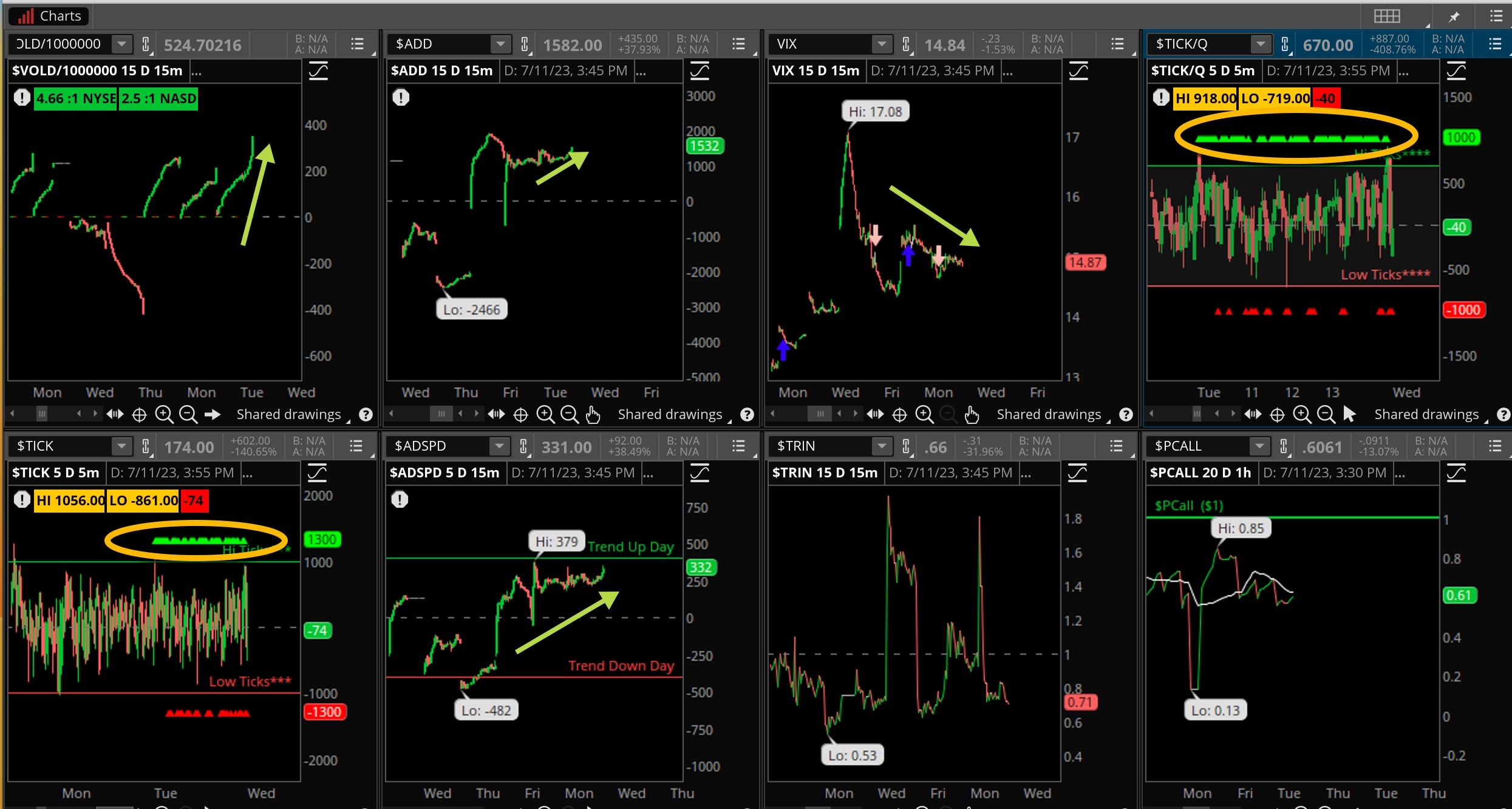

What started out slow turned out to be a very positive day. Sellers were nowhere to be found, notice another strong day of breadth with the VOLD, ADSPD and ADD showing very strong readings. The VIX headed down modestly and that could continue tomorrow with the CPI report. Notice on the graphic the strong ticks all day long, that helped drive the markets higher.

The Dynamite

Economic Data:

- Wednesday: CPI, Beige Book, Mortgage Apps

- Thursday: PPI, jobless claims

- Friday: Import/export prices, Michigan Sentiment

Earnings this week:

- Wednesday:

- Thursday:CTAS, DAL, FAST, PEP

- Friday: JPM, BLK, C, WFC, UNH, STT

Fed Watch:

More Fed speakers out today with Neal Kashkari and Loretta Mester hitting the stage. We don’t expect too much from them but certainly the latest inflation reading might be something to comment on.

Issues/Stocks to Watch This Week

Banks/Financials – This group starts reporting their Q2 earnings this week. Financials have been rather weak since last quarter, we’ll see if they can snap out of their funk.

Interest Rates – We saw a big rise in rates last week, the 2 year above 5% again. If that continues we could see equities shed some value.

For now it appears that 5% level and 4% level on the 10 year should be a peak.

Semiconductor Stocks – On Monday, Taiwan Semi stated their revenue would be down significantly in June. This smacks at recent talk of bullish trends, so we’ll have to see how this group responds.