The Fuse

Futures are mixed to slightly lower this morning as traders digest earnings news and position themselves in front of this week’s big releases.

Interest Rates are falling a bit this morning as it appears the ECB official is signaling a rate reprieve soon. Further, many strategists are now seeing a path towards an economic soft landing.

Plenty of earnings news this week and retail sales out later this morning, along with industrial production and housing data. The CNN fear/greed index is now at extreme greed, so extreme CAUTION is warranted.

We’ll have earnings out this morning from Bank of America, Lockheed Martin, Schwab and Morgan Stanley among others. These names have not performed well of late so we’ll see if earnings manage to push these stocks higher.

A decent rally given the weak close from the prior Friday. We continue to see a broadening out of market breadth to include sectors that have lagged so far in 2023, including transports, industrials and financials (for the most part).

More strong breadth Monday as the cumulative breadth moves closer to a new all time high. Historically when that has occurred a new high inthe SPX 500 is not far off.

We saw volume taper off a bit yesterday as many traders/investors re-group and catch their breadth. As the markets are modestly overbought and sentiment is extremely bullish, it makes sense to see a pause in volume.

A second straight close above 4,500 for the SPX 500 was confirmation that this level is fairly secure. Next upside target would be 4,550 and then 4,600+. The Nasdaq is up 43% on the year and remains the index many covet.

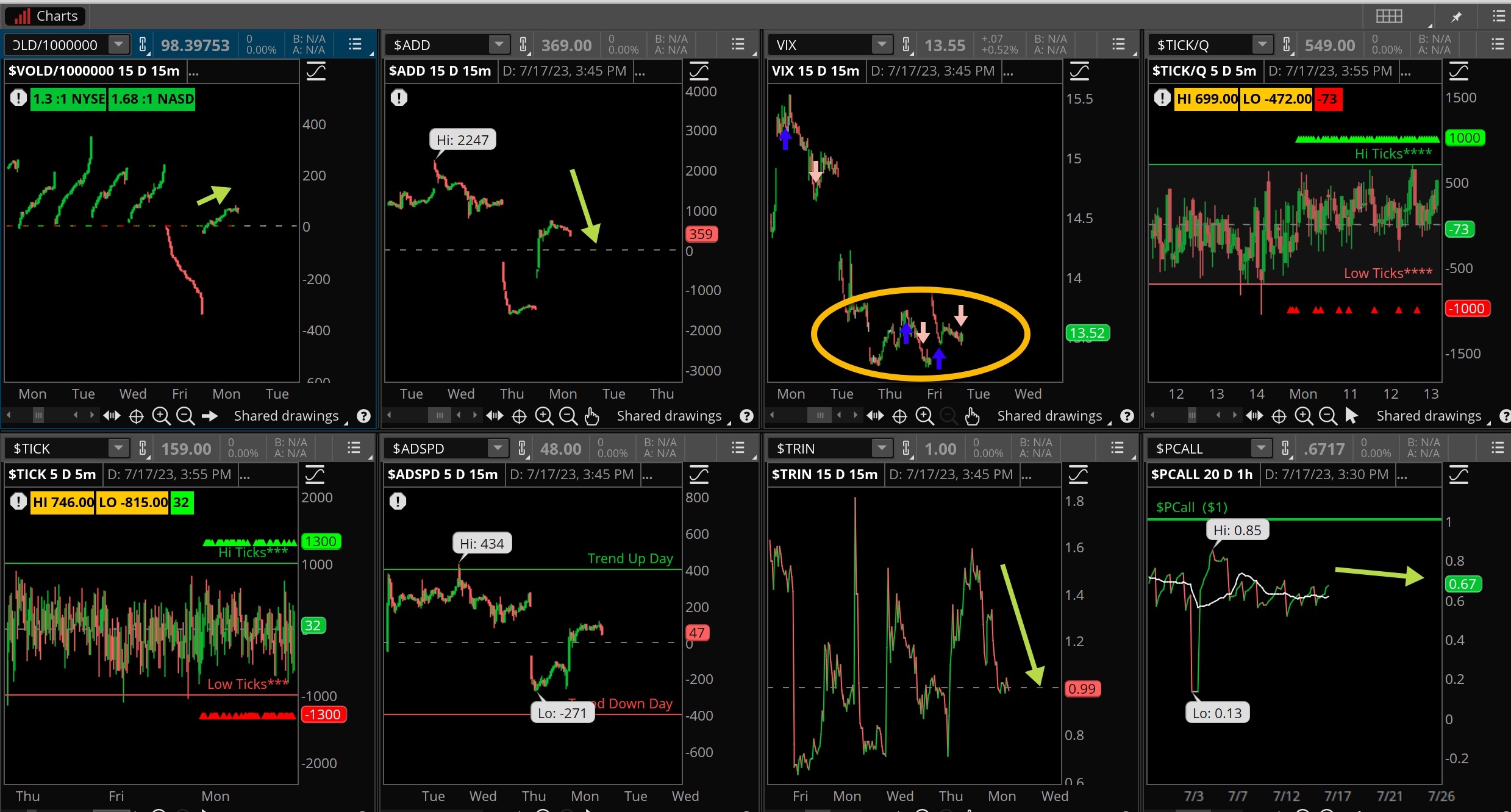

The Internals

What’s it mean?

A rather slow session Monday but constructive nonetheless. With the very strong VOLD last week it makes sense traders were going to cool off a bit. Put calls remain low as does the VIX, which is staying put below 14% for now. Ticks were moderate and breadth was positive but as we have seen lately, these pullbacks have been bought viciously.

The Dynamite

Economic Data:

- Tuesday: Retail Sales, industrial production, business inventories

- Wednesday: Housing Starts, mortgage apps

- Thursday: Jobless claims, philly fed index, leading indicators, home sales

- Friday:

Earnings this week:

- Tuesday: BAC, SCHW, LMT, BK, SYF, IBKR, JBHT

- Wednesday: ASML, ELV, GS, AA, CCI, DFS, IBM, NFLX, TSLA, UAL

- Thursday: AAL, DHI, JNJ, NOK, TSM, CSX, PPG, VMI

- Friday: AXP, AN

Fed Watch:

Fed speakers will be quiet this week in front of the next FOMC meeting. Current odds favor a rate hike at the next meeting but certainly the cooler inflation may offer the committee yet another opportunity to pause. So many hikes in the system seem to be working their magic, and if the economy holds up strong we’ll see rate cuts coming in 2024.

Stocks to Watch

Earnings – Companies will start reporting their quarter this week, a bigger list of names henceforth. We are getting a sampling of tech earnings and other groups this coming week.

Volatility – VIX remains very low and as we have preached in prior weeks, it is dangerously low. That said, until a change in character is seen there is no reason to fight the trend.

Tesla – the big EV car company reports on Wednesday evening, it is always entertaining to hear Elon Musk on the call and how well the company is doing.