The Fuse

Futures are sputtering early this morning as more big earnings are yet to drop. Overnight we saw mixed inflation news from the UK, the PPI over there was in the negative (good news).

Interest Rates on the long end are headed lower this morning as players get prepped and positioned for next week’s Fed meeting. Yes, it’s happening that early! Yields are down across the board, which might spur a bit more rally in the tech space.

Yields plunged in the UK as their economic news overnight might suggest their central bank might look to ease up on the rate hikes.

Strong earnings and raised guidance this morning from Elevance (ELV) while yesterday Interactive Brokers (IBKR) had a slight miss on the top/bottom lines. ASML beat as well but shared a cautious outlook. We’ll hear from Goldman Sachs and Halliburton a bit later this morning, with Tesla, Netflix and IBM after the close.

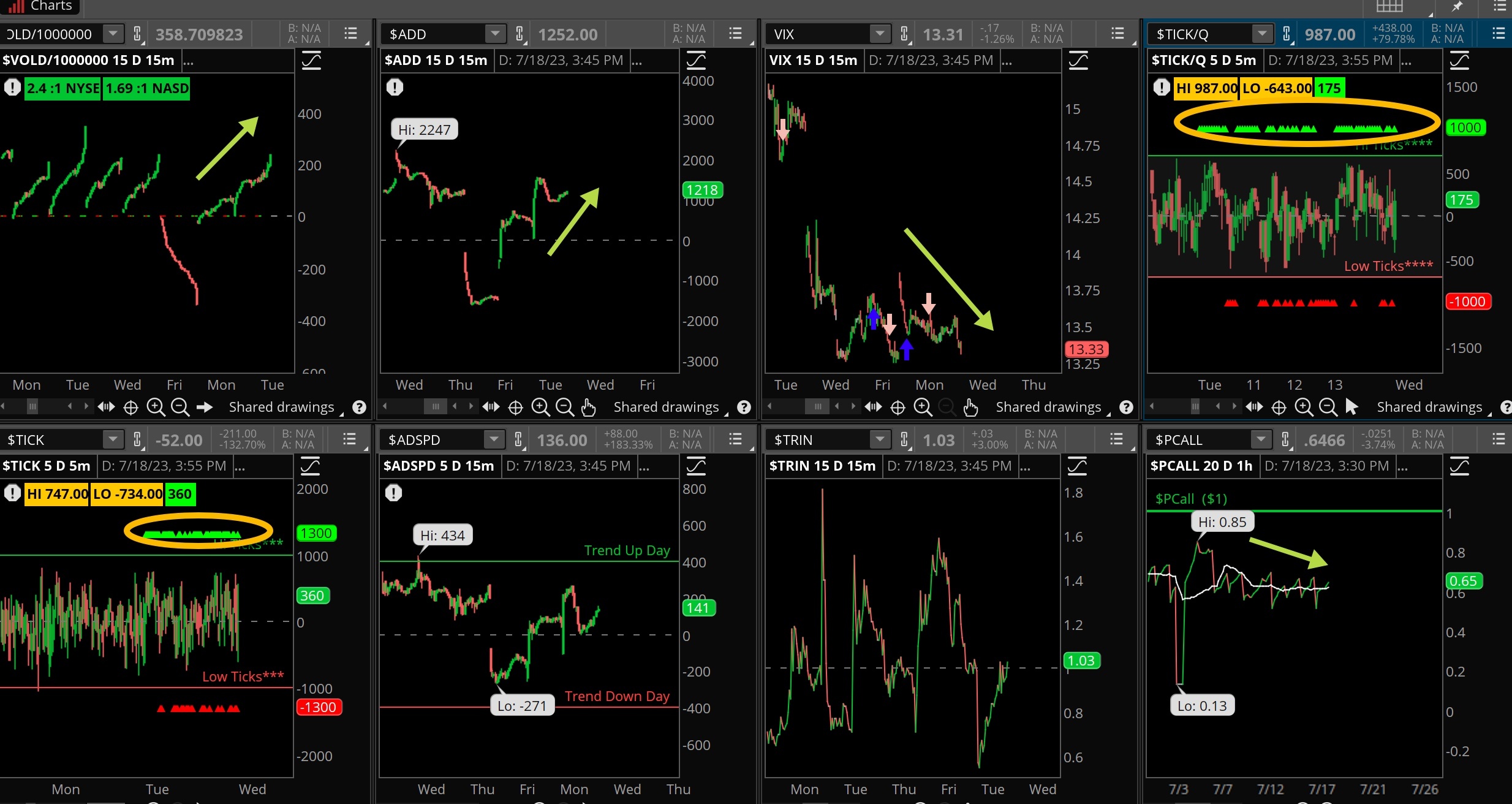

A continuation of the recent rally with very good internals and statistics. Another close above some significant resistance (4,550) was passed today, and with only about 5% left to get the SPX 500 to an all time high, we look for clues that might get us there. One of them is cumulative breadth.

As Tom McClellan likes to say, ‘gobs of breadth’ are enormously bullish. That happened again yesterday with a 2.5 to 1 ratio. The chase is on for stocks it appears, at some point that will end but for now we follow the market trend.

Volume spurted higher on Tuesday as some who were short and looking for a down move were caught off guard. Some of the laggards like financials and industrials were thrust into the spotlight, showing good price action and turnover.

So much for 4,550 as resistance. Next up is a tough nut at 4,600 but frankly the indices are cutting through resistance like a hot knife through butter. We are looking at the all time highs soon enough, supported by extreme 52 week highs vs lows, good breadth, volume and bullish sentiment.

The Internals

What’s it mean?

A solid market session as the indices ripped higher from the start and never looked back. That VOLD did not quite reach those high levels from last week but that is typical after a strong run. Notice the continued pounding away on the ticks, very bullish. As the VIX continues to flounder below 15%, at some point the low volatility is going to matter. For now, it won’t. Put/calls are also falling sharply, these are deep and reflect an overbought condition.

The Dynamite

Economic Data:

- Wednesday: Housing Starts, mortgage apps

- Thursday: Jobless claims, philly fed index, leading indicators, home sales

- Friday:

Earnings this week:

- Wednesday: ASML, ELV, GS, AA, CCI, DFS, IBM, NFLX, TSLA, UAL

- Thursday: AAL, DHI, JNJ, NOK, TSM, CSX, PPG, VMI

- Friday: AXP, AN

Fed Watch:

Fed funds futures at 99.8% probability of a hike next week as of today. Fed speakers will be quiet this week in front of the next FOMC meeting. Current odds favor a rate hike at the next meeting but certainly the cooler inflation may offer the committee yet another opportunity to pause. So many hikes in the system seem to be working their magic, and if the economy holds up strong we’ll see rate cuts coming in 2024.

Stocks to Watch

Earnings – Companies will start reporting their quarter this week, a bigger list of names henceforth. We are getting a sampling of tech earnings and other groups this coming week.

Volatility – VIX remains very low and as we have preached in prior weeks, it is dangerously low. That said, until a change in character is seen there is no reason to fight the trend.

Tesla – the big EV car company reports on Wednesday evening, it is always entertaining to hear Elon Musk on the call and how well the company is doing.